Q1 2026 VC funding: AI raises $240 billion, eclipsing other sectors

Serge Bulaev

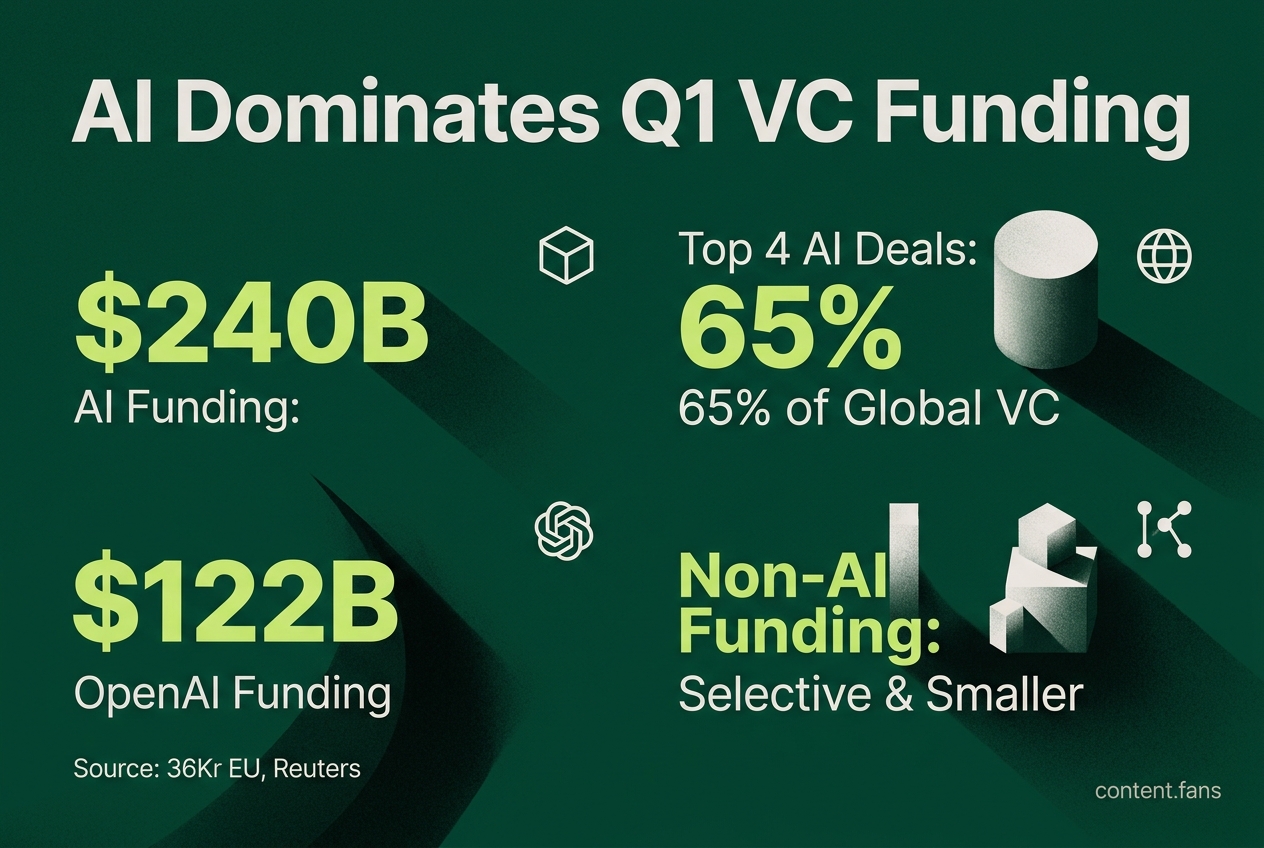

In Q1 2026, AI companies may have taken about 81% of all global venture funding, raising more than $240 billion, with just a few big deals making up most of it. Other sectors like fintech, biotech, and industrial tech got much less funding and only saw large investments when connected to AI. This focus on AI suggests that while overall funding looks high, most other areas may face tighter conditions. The biggest five deals appeared to take up almost three-quarters of all the money, showing that investors might be very cautious except for top AI companies. Outside of AI, investors seem to still support areas like defense tech and cybersecurity that help or use AI.

The Q1 2026 VC funding landscape was dramatically reshaped by Artificial Intelligence, which captured an estimated $240 billion - representing a significant majority of all global venture capital. This intense concentration in a few mega-deals masks tighter funding conditions for most other industries and signals a significant strategic shift for investors and founders alike.

AI's Dominant Share of Venture Funding

According to industry reports, Artificial Intelligence attracted this unprecedented share of capital due to investor belief in AI's massive, power-law return potential. The immense cost of training frontier models necessitates large checks, and a powerful "fear of missing out" (FOMO) cycle has turned top AI companies into must-own assets.

According to industry reports, AI companies secured over $240 billion in Q1 2026, representing a substantial portion of total venture investment 36Kr EU. The funding was heavily concentrated at the top, with four massive rounds by OpenAI ($122B), Anthropic ($30B), xAI ($20B), and Waymo ($16B) accounting for about 65% of global VC activity. This scale left little capital for even established sectors like fintech and biotech.

Funding Landscape for Non-AI Sectors

Outside of the AI frenzy, funding was selective and significantly smaller in scale. Key non-AI sectors demonstrated the following trends:

- Fintech: While still attracting capital, mega-deals were scarce. According to industry reports, banking platforms for startups saw significant funding rounds, though at more modest valuations than in previous years (Reuters repost).

- Industrial & Defense Tech: Companies with a strategic or "physical AI" angle found success. According to industry reports, defense supply chain companies secured substantial Series B rounds, with many achieving unicorn status.

- Biotech: The sector remained active, particularly with European growth funds like JEITO Capital, but saw fewer of the blockbuster rounds that characterized previous years.

- Enterprise SaaS: Traditional software struggled to attract growth-stage funding as investor focus pivoted to AI-native applications and infrastructure.

Implications of a "Barbell" Funding Market

This extreme concentration has created a "barbell market," as described by the NVCA - PitchBook Venture Monitor. Investment is flowing into massive, late-stage rounds for perceived AI leaders on one end, and smaller, cautious seed and Series A bets on the other. This dynamic has critical implications:

- For Limited Partners (LPs): Diversification analysis must now separate AI mega-rounds from underlying early-stage market health.

- For Founders Outside AI: The bar for securing funding has risen. Founders need to demonstrate strong revenue, clear competitive moats, and a path to profitability.

- For Fund Managers: Those not focused on AI face increased scrutiny and may need stronger proof of traction to pass higher diligence standards.

Sector Funding Snapshot: Q1 2026

| Sector | Approximate trend | Primary source phrase |

|---|---|---|

| AI | Dominant share of global VC; four deals represent substantial majority of value | "AI companies attracted significant portion of the funds" - 36Kr |

| Fintech | Selective recovery; limited mega deals | PwC cites limited mega deals outside AI |

| Industrial/Robotics | Funded when tied to autonomy | KPMG notes investor interest in autonomous vehicles and robotics |

| Biotech | Meaningful yet secondary | KPMG lists biotech among active themes |

| Enterprise SaaS | Weak at growth stage; shifting to AI-native tools | 36Kr reports classic software nearly absent |

The Bottom Line: While Q1 2026 posted substantial venture capital totals, the market has become narrower and more challenging than ever. Capital is abundant for foundational AI models and their direct supply chain, including semiconductors and energy infrastructure. For all other companies, the path to funding now requires exceptional traction, demonstrable efficiency, and a clear strategic fit in a world increasingly defined by AI.