Oracle's Q4 FY26 Results: AI Ambitions Drive $23.7B Negative Cash Flow

Serge Bulaev

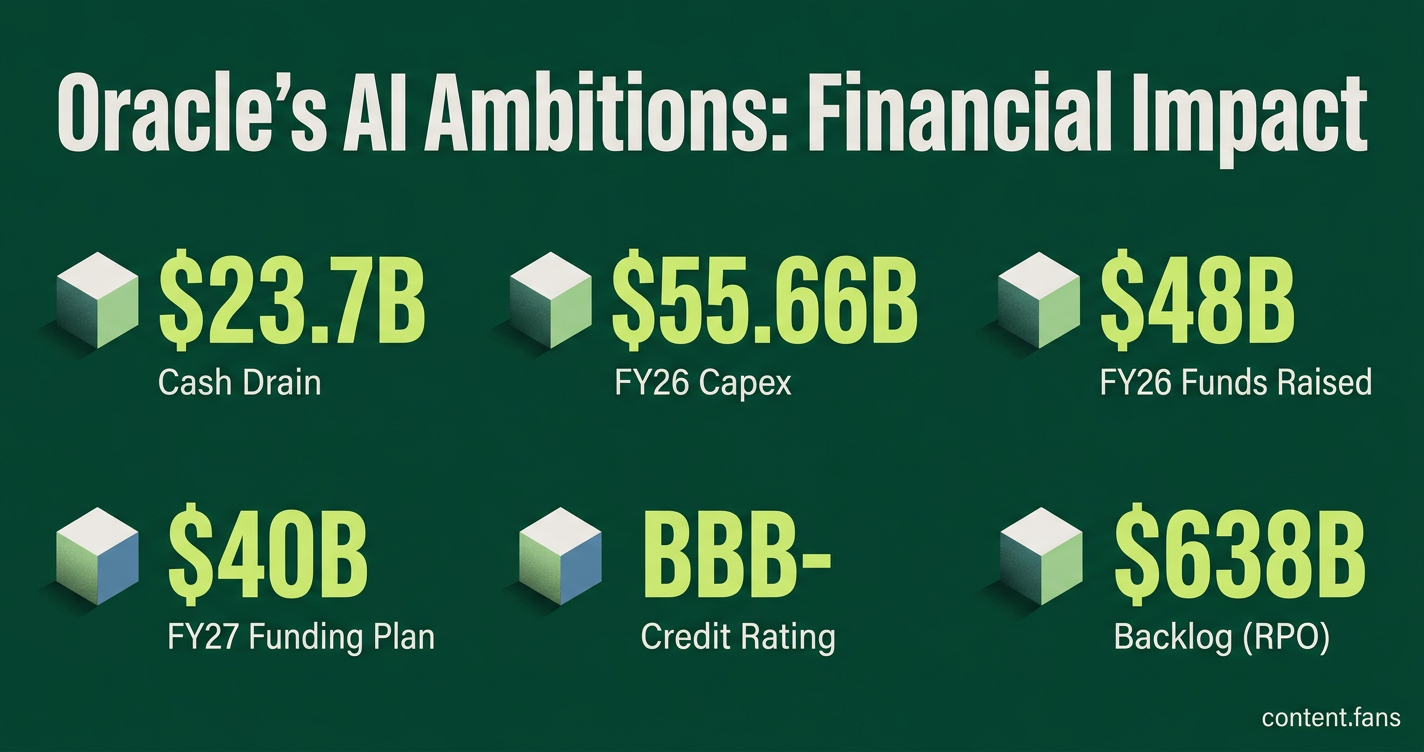

Oracle's Q4 FY26 results show strong cloud growth and a $638 billion backlog, but the company reported a negative free cash flow of $23.7 billion due to heavy spending on AI infrastructure. Management says this spending is a long-term investment, but credit markets appear worried about Oracle's large funding gap and increasing debt. S&P downgraded Oracle's credit rating, noting risks like high capital spending, continued negative cash flow, and reliance on big contracts, especially with OpenAI. While Oracle's shares went up as equity investors focused on revenue growth, bond investors asked for higher yields because of the company's financial risks.

Oracle's recent financial results reveal a pivotal moment for the tech giant, with a staggering $638 billion backlog clashing against significant cash flow challenges. This financial strain, driven by an aggressive AI infrastructure buildout, has prompted credit markets to re-evaluate the risks. While management presents the massive capital spending as a strategic long-term investment in AI, bond investors are increasingly concerned about the immediate funding gap and mounting debt needed to sustain this breakneck growth.

Cloud demand meets capital reality

Oracle's negative cash flow is a direct result of its enormous investment in AI infrastructure. The company is spending billions more on data centers and computing power than it generates from operations to capture future AI market share, creating a significant near-term funding deficit.

Surging demand for AI workloads is straining Oracle's capital resources. According to industry reports, Oracle Cloud Infrastructure (OCI) AI revenue experienced substantial year-over-year growth, with the company selling out its GPU capacity. To meet this demand, Oracle spent about $55.66 billion in FY26, above its $50 billion target. The company has provided guidance for significant additional capital expenditures, with industry reports suggesting gross capex could reach substantial levels when including customer prepayments, as noted in the company's Oracle Investor Relations filing. This spending pattern has created substantial cash flow challenges, with the company experiencing a $23.7 billion cash drain despite strong operational performance. To bridge the gap, Oracle raised $48 billion in FY26 ($43 billion debt, $5 billion equity) and plans another $40 billion raise in FY27, including a major equity program.

Credit markets push back

Credit markets are signaling significant concern over Oracle's financial strategy. According to industry reports, investors have steadily repriced the company's risk, with credit default swap spreads widening substantially. This sentiment culminated on July 9, 2026, when S&P Global Ratings downgraded Oracle's long-term issuer rating to BBB-, just one step above speculative grade. S&P cited the projected $42 billion free operating cash flow deficit for FY27 and leverage expected to hit the mid-4x range. The downgrade, which also included a lower short-term rating of A-3, makes future borrowing more expensive and raises the stakes for Oracle's planned FY27 financing.

Why backlog alone does not calm bondholders

While Oracle touts its $638 billion in remaining performance obligations (RPO), this massive backlog has failed to soothe bondholders' nerves. The primary concern is concentration risk: according to industry reports, a significant portion of the RPO is linked to large AI compute deals, including major contracts with companies like OpenAI. As S&P warned, a single major customer's failure or strategic shift could leave Oracle with costly, under-utilized data centers. Rating agencies and credit strategists have pinpointed several key risks:

- Capital intensity of AI chips and power provisioning

- Negative free cash flow projected through at least FY27

- Leverage exceeding 4x debt to EBITDA under S&P methodology

- Dependency on major customers for a substantial portion of backlog

- Potential margin squeeze if energy or financing costs rise faster than pricing power

Equity view diverges from debt view

The market's reaction to Oracle's financial position reveals a stark divergence between equity and debt investors. Oracle shares actually climbed 2.7% on the day of the S&P downgrade, as equity markets prioritized the strong growth in cloud infrastructure revenue and strong forward guidance. In stark contrast, bond investors immediately demanded higher yields, reflecting their focus on creditworthiness. This split highlights the central debate: Can Oracle convert its massive backlog into cash flow fast enough to outpace rising borrowing costs and justify its capital burn? While industry reports suggest the company is using customer prepayments to fund a significant portion of its secured power for new data centers, its deep reliance on external financing puts it in a more precarious position than hyperscale competitors that fund expansion from their vast internal cash flows.