Cognition AI Raises $1B+ at $26B Valuation, Nears $500M Revenue

Serge Bulaev

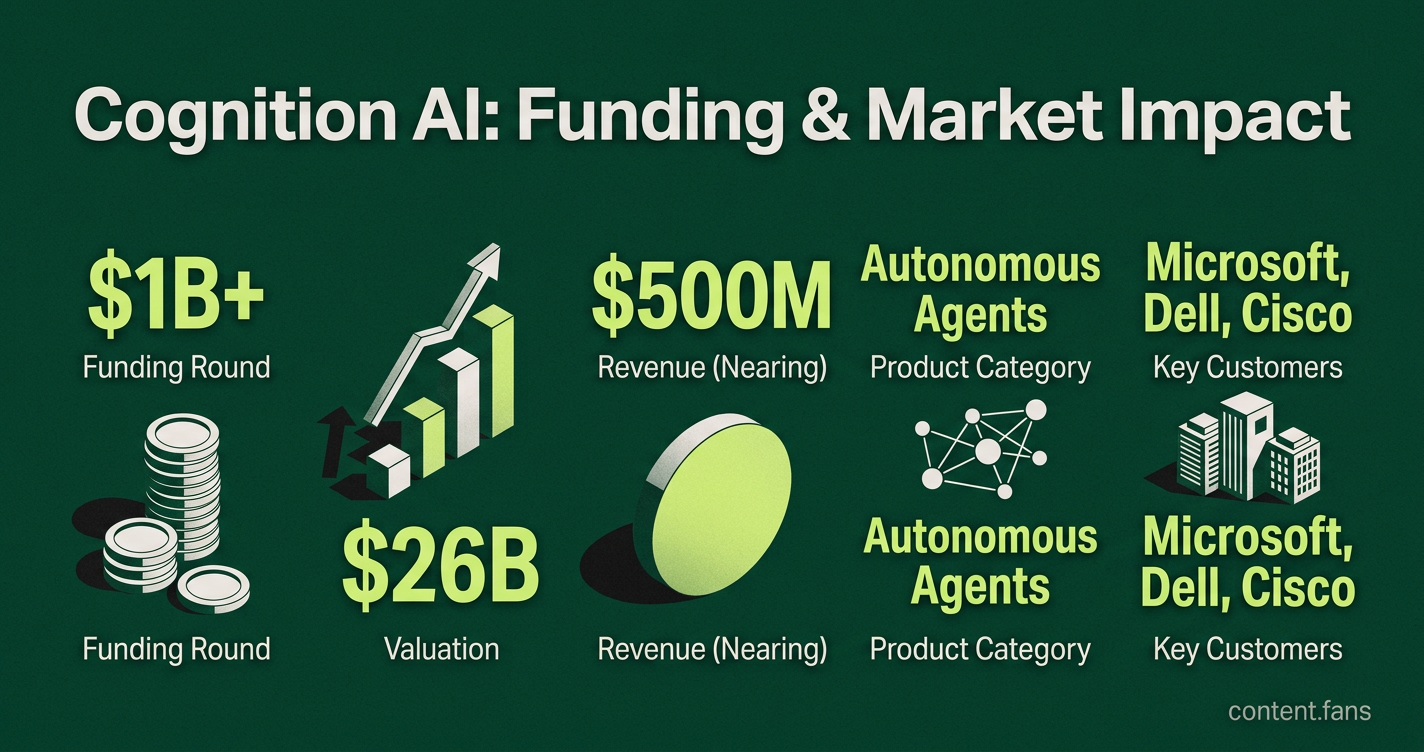

Cognition AI has raised over $1 billion at a $26 billion valuation, and its revenue run rate grew from about $37 million in May 2025 to $492 million by early 2026. The company sells an autonomous coding agent called Devin that can do multi-step tasks with little human help, but how widely Devin is used is not clear. Cognition faces competition from code assistants and AI-powered IDEs, and its future profit may depend on controlling costs and keeping users. Many AI firms, including Cognition, appear to be spending heavily, so profitability may be years away. It is also uncertain if Devin's current momentum will turn into a large and stable customer base.

Cognition AI, maker of the autonomous coding agent Devin, has secured a significant new financing round according to industry reports. According to Yahoo Finance, the company has shown substantial revenue growth over recent months. This explosive growth places Cognition in the elite tier of AI startups but also sharpens focus on its long-term strategy for market share, cost control, and profitability.

What Cognition Actually Sells

Cognition AI markets Devin as an autonomous software agent designed to execute complex, multi-step engineering tasks with minimal human oversight. Unlike AI assistants that only suggest code, Devin can independently plan, write, and debug entire software features, positioning it as a next-generation development tool.

The company's product is described as the "third layer" of the AI coding stack. While most tools offer simple code completion, Devin aims to perform complete tasks, from deploying a backend service to refactoring a legacy codebase, defining it as a fully autonomous agent.

Competitive Field in 2026

The AI coding market is segmented into three distinct areas, according to analysis from Contrary Research:

- Code Completion Assistants: Tools like GitHub Copilot and AWS Q that offer line-by-line suggestions.

- AI-Native IDEs: Platforms such as Cursor, which has reportedly gained significant user adoption by deeply integrating AI into the development environment.

- Fully Autonomous Agents: The emerging category where Devin competes alongside Anthropic's Claude Code, Magic AI, and Poolside AI.

While established players benefit from massive distribution by bundling assistants into existing platforms, the rapid adoption of AI-native IDEs highlights their potential as a major competitive threat. Cognition's strategy relies on proving the value of its deeper autonomy, though concrete adoption metrics for Devin are still scarce beyond revenue figures.

Investors Are Paying for Velocity

Cognition's valuation reflects intense investor demand for developer tools with proven recurring revenue. This trend is sector-wide: according to industry reports, AI startups command significant valuation premiums over non-AI companies, with AI firms raising substantially larger funding rounds on average. Cognition's valuation is further amplified by its position as a rare autonomous agent showing significant enterprise traction. Its reported customer list includes major players like Microsoft, Dell Technologies, and Cisco Systems, although specific deployment sizes remain undisclosed.

Can That Growth Translate into Profit?

As investor focus shifts toward sustainable margins, the key question becomes profitability. For AI coding companies like Cognition, achieving this depends on mastering three critical factors:

- Cost Control: Managing high inference costs through techniques like model distillation and efficient caching.

- Smart Pricing: Implementing recurring or usage-based models that outpace cloud expenditures.

- User Retention: Ensuring high retention by deeply embedding the tool into core developer workflows, including build, test, and deployment.

Many top-tier AI companies operate with high burn rates, and profitability may be years away. This challenge almost certainly applies to Cognition, as its rapid scaling of revenue has been matched by significant investment in hiring and compute resources.

What to Watch Next

Moving forward, analysts will monitor if Cognition can convert its significant momentum into a broad and stable installed user base. Key challenges include addressing enterprise concerns around security and compliance for autonomous agents. In a fragmented market, the company's long-term success and profitability will likely depend on its ability to continuously improve model efficiency and defend its unique edge in coding autonomy.

What drove Cognition AI's recent valuation increase?

The company raised substantial funding after its revenue growth showed significant acceleration - an increase that signals explosive enterprise demand for autonomous coding agents.

How does Cognition AI position itself against rivals like GitHub Copilot or Cursor?

Cognition targets the third layer of the AI coding market: fully autonomous agents that can plan, execute, and validate multi-step development tasks inside a single workflow, rather than simple code-completion or AI-native IDEs.

Is the 2025 investor appetite for developer-focused AI tools sustainable?

Industry reports show AI startups command significant valuation premiums over non-AI peers, with AI funding rounds substantially larger than non-AI counterparts - but investors now also demand clear recurring revenue and cost-efficient scaling before writing mega-rounds.

What unit-economics metrics underpin strong revenue growth?

Founders and investors watch inference cost per task, workflow integration depth, and high-LTV customer concentration; successful startups blend SaaS subscriptions, usage-based fees, and outcome-based pricing to keep gross margins healthy while burn rates stay elevated across the sector.

Could Cognition AI continue its growth trajectory?

According to industry reports, the company is targeting continued strong revenue growth, but reaching that scale will depend on sustained enterprise adoption, competitive pressure from well-funded incumbents, and the company's ability to reduce per-task compute costs as usage scales.