Anthropic CEO Amodei Frames AI as New Economic Factor

Serge Bulaev

Anthropic CEO Dario Amodei suggests that artificial intelligence may become a new main factor in the economy, like land, labor, and capital. He says AI is improving quickly and could lead to fast economic growth but might also replace many entry-level office jobs. Experts estimate nearly $7 trillion could be needed for more data centers by 2030, and spending is compared to the large investments of the railroad era. Some analysts warn that if revenues do not meet expectations, companies could face serious financial problems. Historians note this high spending may lead to both increased productivity and the risk of too much capacity, as happened in the past.

The concept of AI as a new economic factor, championed by Anthropic CEO Dario Amodei, is rapidly moving from theory to reality. Tech executives now discuss compute power with the same gravity as 19th-century industrialists discussing railroad steel, and their massive budgets reflect this paradigm shift. This analysis explores Amodei's economic framework, the colossal scale of current AI infrastructure spending, and its parallels with transformative historical investments.

Amodei posits that artificial intelligence's cognitive capability is improving on a Moore's Law-like curve. He told Bloomberg this could spur "very fast GDP growth" but also threaten a significant portion of entry-level office jobs. This growth is already tangible; his own company has reported substantial revenue growth that strained its data center capacity.

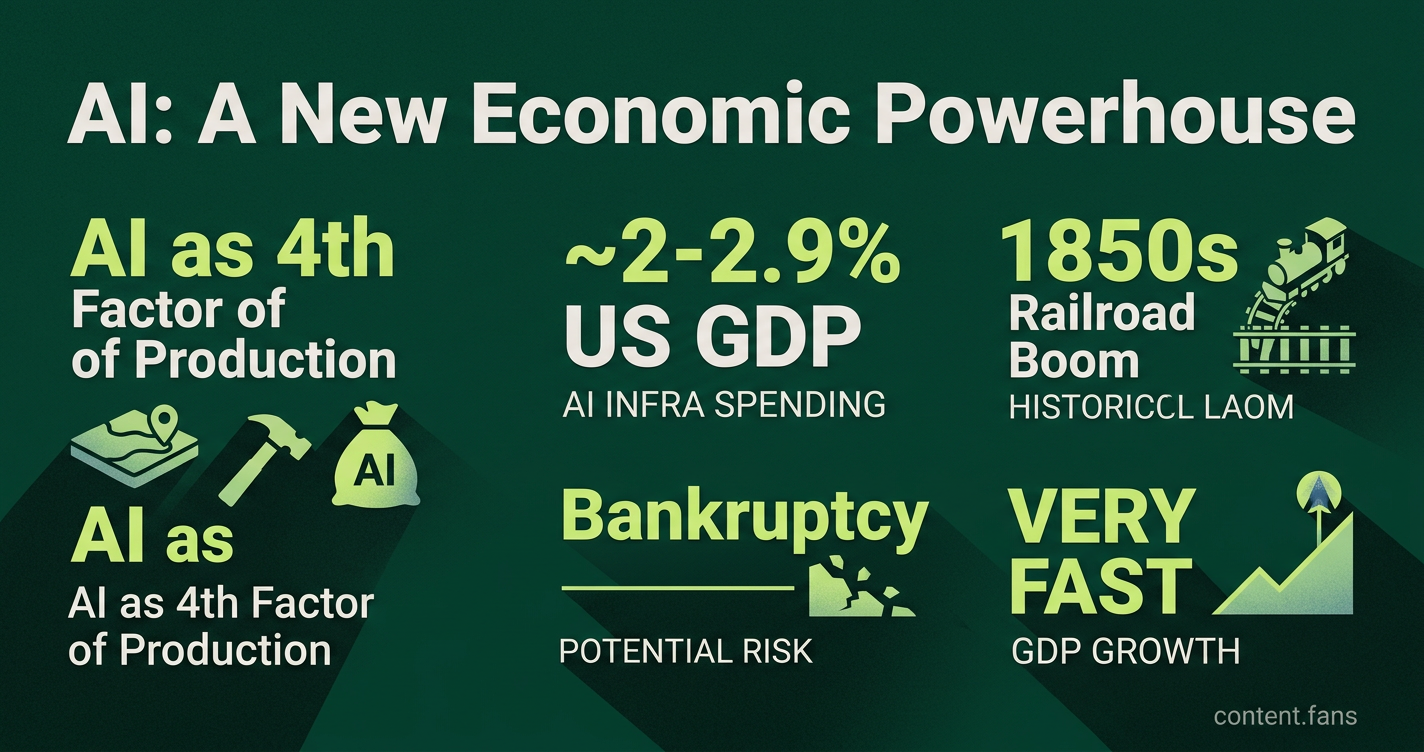

His core argument positions AI-driven intelligence as a fourth factor of production, joining land, labor, and capital. Economists now treat this as a practical budgeting principle: if intelligence scales exponentially, then the servers and electricity fueling it must scale accordingly. However, Amodei also warned Fortune of the inherent risks, noting that if revenue fails to meet capital expenditure forecasts, firms could face bankruptcy.

Infrastructure Math: The Cost of a New Economic Factor

The push to establish AI as an economic factor requires a historic investment in infrastructure. Industry reports suggest massive spending needs for new data centers, with AI workloads consuming a significant portion of new capacity and driving global electricity demand to unprecedented levels.

Leading consultants quantify the staggering scale of this buildout. Industry analysts project substantial investment needs for new data centers globally, with a significant portion dedicated specifically to AI facilities. This spending rate is comparable to the mid-19th century railroad construction boom.

Forward-looking studies highlight the physical demands of such budgets:

- Industry reports suggest global data center power needs could reach unprecedented levels by 2030.

- AI-specific tasks are expected to drive a substantial portion of this new capacity.

- In the U.S. alone, industry estimates suggest data center power consumption could reach significant levels by 2035.

Historical Echoes and Financial Risks

This unprecedented capital expenditure draws historical parallels to the railroad boom of the 1850s. Research indicates that capital spending on rail lines at that time averaged 2 to 2.9 percent of U.S. GDP, a range consistent with big tech's projected AI capex today. As with past infrastructure cycles, observers anticipate a dual outcome: immense productivity gains alongside the significant risk of overcapacity. This tension is precisely what Amodei's bankruptcy warnings reflect.

What does it mean to treat intelligence as a new factor of production?

Dario Amodei places AI-generated intelligence on the same shelf as land, labor and capital.

- Intelligence is now "a smooth exponential curve" - he likens it to Moore's Law for CPUs, except this time the resource being doubled is general cognitive work.

- Once you can rent "a country of geniuses in the data center," marginal cost of knowledge work collapses, pushing every downstream price and process to re-price around that new floor.

How much compute and electricity will this new factor really need?

Industry outlook reports give a feel for the scale:

- A substantial portion of data-center build-out through 2030 is earmarked strictly for AI workloads.

- That translates into significant extra AI capacity in the next five years - roughly equivalent to a major nation's entire current power consumption.

In short, intelligence stops being scarce, electricity becomes the scarce input.

Why is today's AI spending not widely viewed as a bubble?

Markets fear a repeat of the dot-com crash, yet three signs point to infrastructure rather than speculation:

1. Capex intensity: U.S. Big-Tech AI spending represents a significant portion of GDP, matching historical infrastructure booms that physically transformed the economy.

2. Revenue is already following - Anthropic itself has seen substantial growth before new chips were even online.

3. Lead times: Data centers take 18-24 months to finish, so today's cranes are answering demand already baked into order books, not hype cycles.

What could go wrong if revenue lags the infrastructure build-out?

Amodei warns the mismatch can flip from virtuous to vicious within a single budget cycle.

- If a firm builds for substantial AI revenue expectations and final demand falls short, "there is no force on Earth that will stop me from going bankrupt."

- Entire regions risk stranded power and half-built chip cities if adoption curves hiccup for even a year.

How should business leaders position for intelligence-as-infrastructure?

- Treat AI capacity like logistics capacity - secure long-term power and cloud contracts now; prices will move upward as silicon and substations become the new bottlenecks.

- Re-engineer processes assuming near-zero marginal intelligence cost; otherwise a competitor will.

- Track policy: The vast majority of AI capex is private, but permitting, grid upgrades and trade restrictions sit in public hands - relationships with regulators and utilities may become as strategic as the tech stack itself.