VCs Fund AI Infrastructure for Reliability; ChatSee.ai, Jedify Raise $30M

Serge Bulaev

Venture capital firms are putting more money into AI infrastructure startups that may make AI systems more reliable. Companies like ChatSee.ai and Jedify have recently raised new funding to help trace errors and improve debugging in AI. Reports suggest most VC investment in early 2026 is going into AI, especially tools that help find and fix problems. Some experts say this could mean steady demand for tools that help with observability and failure detection. Spending on AI infrastructure may keep growing, and the market might see more mergers as companies try to offer more complete solutions.

Venture capital is increasingly funding AI infrastructure to ensure production-grade reliability, steering significant investment into startups that diagnose failures and provide real-time observability. This focus is highlighted by recent funding activity in companies developing agent error tracing and topology-aware debugging tools.

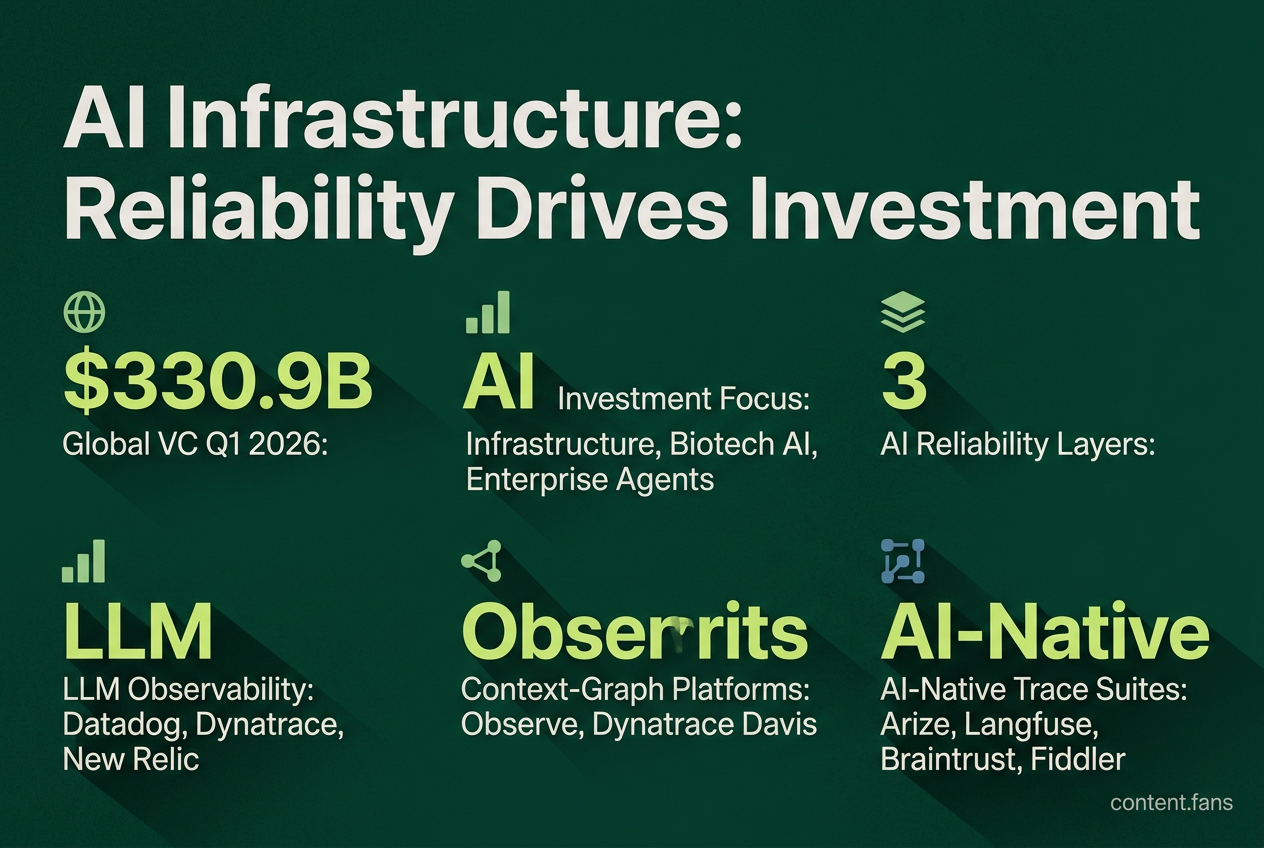

This investment is part of a broader capital flow into AI. KPMG reported global VC investment of $330.9 billion in Q1 2026, fueled by a small number of large megadeals and concentration in AI-related companies. According to industry reports, AI infrastructure, biotech-linked AI, and enterprise agents are dominating the 2026 investment landscape.

Deal momentum and concentration

Investors are betting that as AI systems move from pilots to production, reliability and debugging will become more critical than developing new models. They are funding startups that offer 'failure intelligence' and 'context graphs' to help engineers diagnose and repair complex AI failures, ensuring stable enterprise operations.

Industry reports indicate that a significant portion of global venture capital has concentrated on AI, with many investments directed toward late-stage labs. This focus creates a trickle-down effect, benefiting early-stage 'picks-and-shovels' startups that provide essential debugging, evaluation, and cost-control tools. S&P Global notes that generative AI firms are becoming "asset-heavy, operating more like infrastructure than typical SaaS players," reinforcing the durable demand for observability and failure intelligence tooling.

Mapping the ecosystem

According to industry analysis, the 2026 vendor ecosystem for AI reliability is structured in three overlapping layers:

- Full-stack observability incumbents adding LLM modules: Datadog, Dynatrace, New Relic

- Context-graph centric platforms: Observe and Dynatrace's Davis engine

- AI-native trace and evaluation suites: Arize Phoenix, Langfuse, Braintrust, Fiddler

Industry reports indicate that Datadog's LLM Observability provides interactive decision-path graphs and loop detection. Observe combines a streaming data lake with a context graph to link signals for guided remediation, while Arize Phoenix focuses on prompt clustering and drift detection to improve agent performance.

Funding patterns by subcategory

Startups focused on failure intelligence are attracting capital because localizing outages in multi-component LLM stacks is a significant challenge. Investors are backing solutions that can pinpoint root causes across prompts, models, and orchestration layers. Similarly, context-graph platforms appeal to enterprises needing robust lineage and compliance reporting, while comprehensive observability tools that correlate metrics, logs, and traces are in demand to manage rising cloud costs from AI workloads.

Recent funding rounds in the AI observability space show growing investor interest across seed and Series A stages, with companies focusing on agent failure tracing, context-graph debugging, and LLM evaluation tools receiving significant backing from venture capital firms.

Near-term consolidation outlook

Industry analysis points toward significant market consolidation by 2027. Enterprises are looking to "increase AI budgets while concentrating spending among fewer providers," according to Synvestable. With substantial AI infrastructure spending expected in 2026, the market scale advantages large vendors with established distribution. Furthermore, Castle Rock Digital highlights high growth in networking, storage, and cooling, suggesting hyperscalers will likely acquire or bundle adjacent tooling. This trend puts pressure on specialized observability and vector-database companies, making platform integrations and M&A activity more probable through 2027.