US officials discuss government taking equity stakes in AI companies

Serge Bulaev

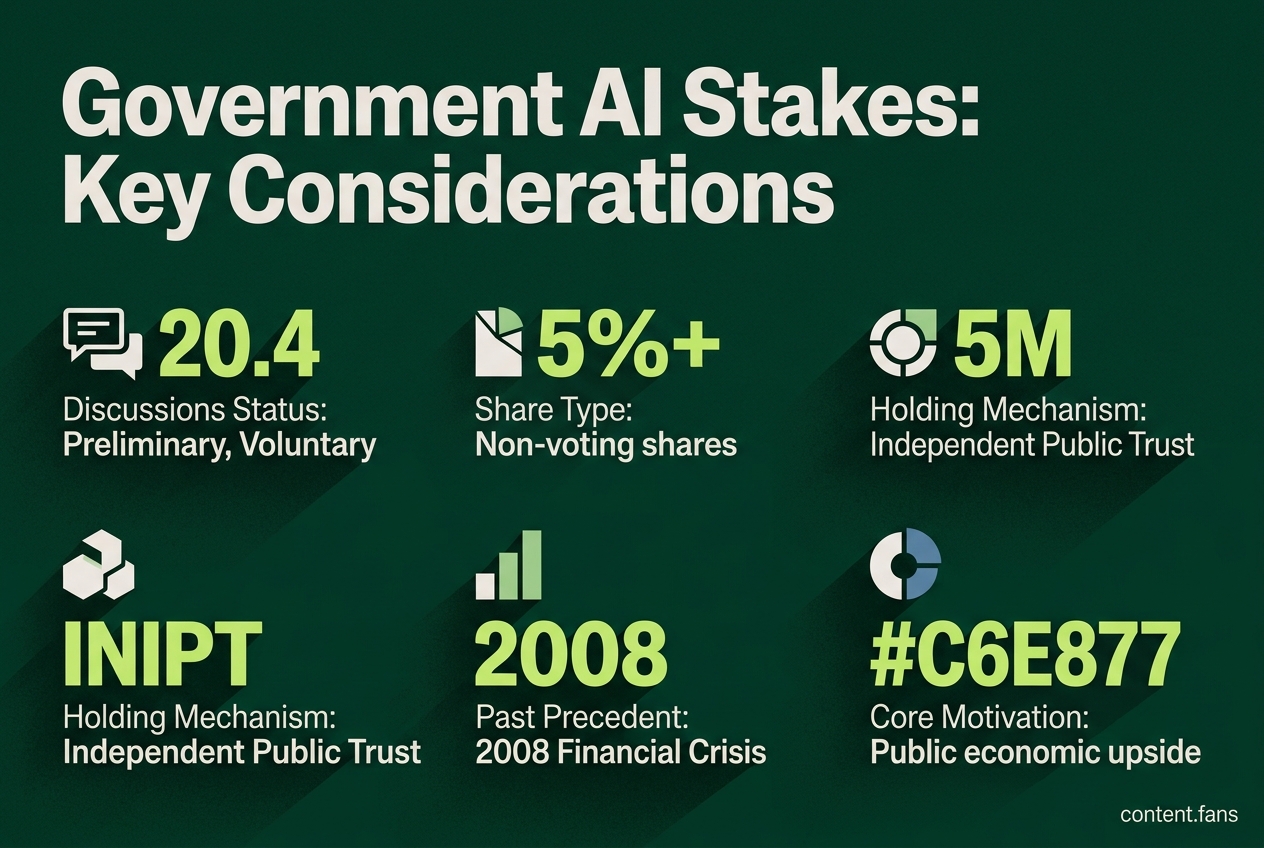

US officials have had early discussions with some AI companies about the government possibly buying shares in them, but any involvement would be voluntary for now. There is no law or set plan, and officials seem interested in making sure the public gets some benefits from the growth of important AI firms, without harming competition or national security. Past examples, like the government's temporary stakes in banks and car companies, suggest this approach might be legal if companies agree and Congress approves. Experts are suggesting ways to reduce conflicts, such as having an independent trust hold the shares and making all holdings public. Other ideas, like special taxes or voluntary payments, are also being considered, and it is not yet clear which, if any, option will move forward.

In Washington, US officials are discussing government taking equity stakes in AI companies as a novel way to ensure the public benefits from the technology's rapid growth. This article examines the facts behind these preliminary talks, exploring the potential for public ownership to fund household dividends without harming competition or national security.

Where the idea stands today

Senior officials have held initial, voluntary discussions with AI developers about the government acquiring shares. While no legislation exists, the talks are motivated by a desire for the public to share in the economic upside of frontier AI models, potentially through a dividend funded by the government's stake.

According to industry reports, these preliminary discussions would involve a voluntary transfer of shares; no legislation or official timetable has been announced (Reuters). OpenAI was reportedly among the companies involved, with a public dividend being one of several ideas for distributing potential returns (The Next Web). The conversations are driven by three core concerns: that advanced AI firms will generate immense economic value, that traditional taxes may not effectively capture this wealth, and that a voluntary equity stake could provide public upside without new immediate taxation. The backdrop is a bipartisan consensus that frontier AI is both a strategic asset and a potential source of economic inequality.

Lessons from earlier equity moves

The U.S. has a limited but relevant history of federal equity holdings, typically driven by crisis or specific industrial policy rather than routine investment. Past examples include the temporary Treasury control of banks and auto companies during the 2008 financial crisis and a government stake in Intel using CHIPS Act funds. A Lawfare analysis noted that such stakes are most legally sound with company consent and explicit congressional authorization, but they still raise concerns about political influence and market distortion.

Governance safeguards under debate

To mitigate potential conflicts of interest, policy experts are proposing several governance safeguards. These measures, often modeled on past crisis-response programs, include:

- Holding shares in an independent public trust to separate ownership from regulation.

- Using non-voting shares to prevent government interference in corporate strategy.

- Establishing firewalls that bar officials from dealing with firms in the government's portfolio.

- Mandating full public disclosure of all holdings, their size, and voting status.

- Defining clear entry and exit criteria to limit political discretion and favoritism.

Alternative tools on the table

Given the political sensitivity of direct ownership, officials are also evaluating simpler alternatives. These include revenue-sharing agreements, new corporate taxes targeting excess profits from AI, or creating a public AI dividend fund through voluntary corporate contributions. Each option presents a different balance: taxes offer revenue certainty but may deter investment, while voluntary schemes depend on corporate goodwill. Direct equity captures potential gains but also exposes taxpayers to market risks.

For now, the concept of public equity in AI firms is purely exploratory. Government agencies are assessing legal frameworks, companies are considering the governance challenges, and lawmakers are gauging public sentiment. While historical precedent and proposed safeguards suggest a path exists, its feasibility depends on creating a structure that both insulates the market from political influence and persuades AI companies that a shared stake is preferable to future taxes.

What exactly is being discussed right now?

According to industry reports, senior U.S. officials have held preliminary, non-binding talks with major AI companies about the possibility of the federal government acquiring voluntary equity stakes. No legislation has been drafted, no price has been set, and no timeline has been agreed upon. The most concrete proposal floated in these conversations is that any eventual returns could fund a "public dividend" to American households, but even that remains one idea among several. In short, this is still at the "what-if" stage, not a done deal.

Why would the government want shares instead of just taxing the companies later?

Taking an equity slice ties public reward directly to private success: if an AI firm's valuation soars, the Treasury's dividend grows at the same rate, before any lobbying or accounting maneuvers shrink the taxable base. Treasury used equity-style interventions in the 2008 crisis, but the approach was not limited to crisis-only use; the 2025 Intel stake is a later non-crisis example. The 2025 Intel transaction was a government stake tied to CHIPS Act-related support, giving taxpayers both upside without forcing a distressed sale. For AI, officials argue ownership could also accelerate safety standards, since regulators would share in long-term value rather than face accusations of stifling innovation.

What are the biggest legal and economic risks?

- Market distortion: Government ownership could bias procurement, grant decisions, and even antitrust enforcement toward portfolio firms, chilling competition.

- Conflict of interest: The same agencies writing AI safety rules would literally profit when the models they oversee succeed, raising revolving-door and lobbying questions.

- Taxpayer downside: Equity stakes absorb full downside risk; if valuations crash, public pensions or emergency funds might be on the hook.

Legal scholars note the CHIPS Act did not explicitly authorize equity for pure industrial-strategy purposes, so any AI deal would need new statutory language or creative use of existing emergency powers, both certain to face court challenges.

Are there proven guardrails that could make this work?

Yes. Policy experts have proposed an independent investment trust framework, drawing from various historical models.

| Guardrail | Purpose |

|---|---|

| Non-voting shares held by an independent board appointed for fixed terms | Reduces political meddling in product decisions |

| Firewalls: regulators involved in procurement, antitrust, or AI safety must recuse from decisions involving portfolio companies | Keeps referee and player separate |

| Mandatory public disclosure of position size, valuation, and dividend flows | Lowers information asymmetry for other investors |

| Objective exit rules (e.g., automatic divestiture once a firm reaches significant market share or sunset provisions) | Prevents permanent state champions |

These measures address concerns that without such walls the program could create an uneven playing field more corrosive than any tax break.

What are the realistic alternatives?

Revenue-sharing or AI dividend funds could avoid direct ownership. Several states are piloting gross-receipts taxes on frontier-model compute, ring-fenced for universal basic dividend checks. Voluntary cloud-access credits are another path: firms that pledge compute hours to public-interest projects (disaster-response simulations, scientific research) receive priority in federal procurement. Each mechanism preserves competitive neutrality while still letting society capture part of the AI windfall.