SpaceX Files IPO with $1.75 Trillion Valuation, Starlink Leads Revenue

Serge Bulaev

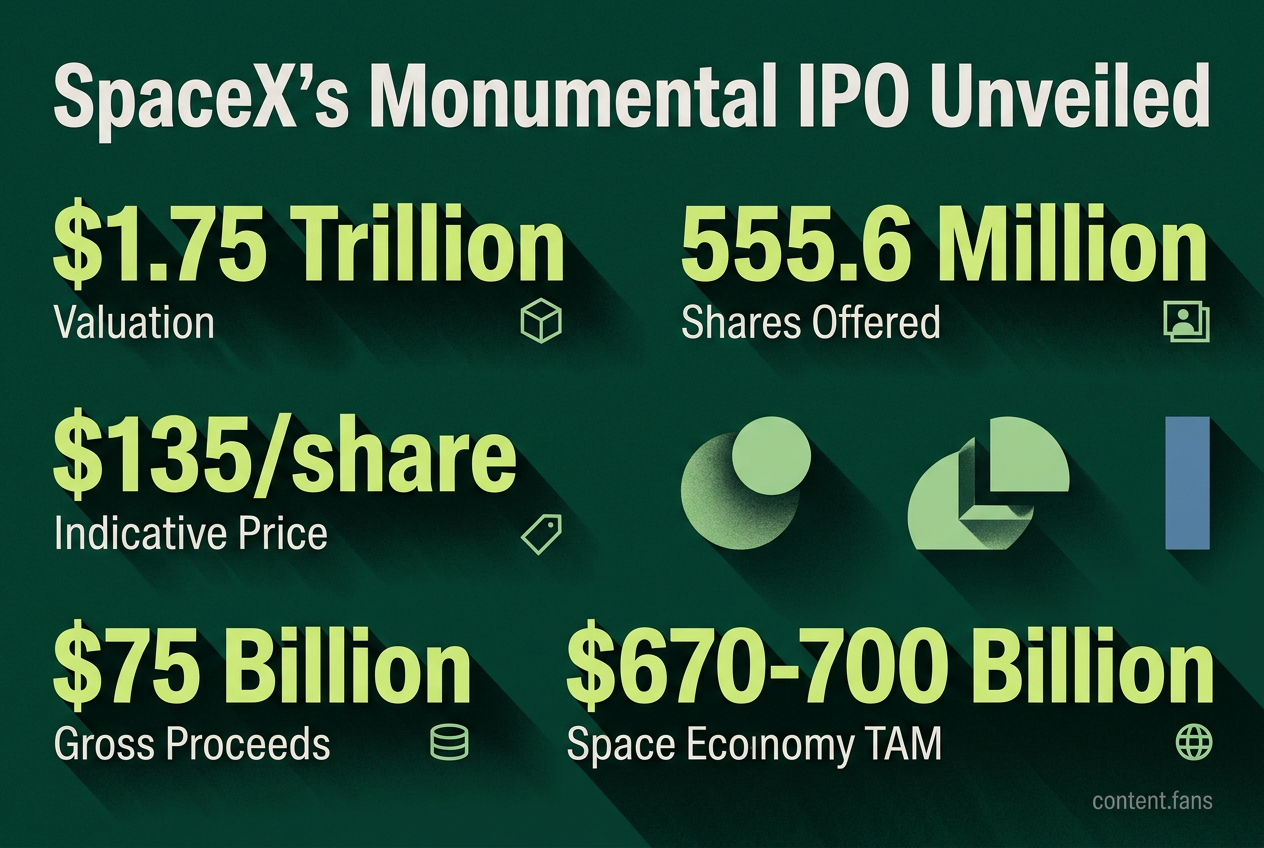

SpaceX has filed for an IPO with a reported $1.75 trillion valuation, making it one of the largest ever in U.S. markets. Starlink appears to be the main source of revenue, providing $11.4 billion out of SpaceX's $18.7 billion in sales for 2025. The company claims that its potential market is $28.5 trillion, mostly from AI, but some experts say this number may be too high and give lower estimates. SpaceX's filing also suggests it may issue more shares in the future, and a big deal with Google for xAI compute capacity might add nearly $30 billion in revenue, though the benefit to xAI itself is not yet clear. Whether the high valuation is justified may depend on how future events and reviews unfold.

In a landmark event for U.S. financial markets, the official SpaceX IPO filing reveals a monumental $1.75 trillion valuation, with its Starlink satellite internet service positioned as the lead revenue driver. The company's S-1 prospectus offers the first detailed look at the financial performance powering one of history's largest public offerings, prompting investors to scrutinize its blend of satellite broadband, launch services, and AI compute revenues.

Deconstructing SpaceX's Revenue Mix

According to industry reports, SpaceX generated significant revenue in 2025. The primary revenue source was its Starlink satellite broadband service, followed by traditional launch services. The reported revenue was associated with an emerging AI sector linked to X and Grok, not a SpaceX xAI division.

These figures, detailed in the S-1 and reported by Al Jazeera, underscore the company's strategic shift from its foundational rocket launch business toward building a recurring revenue model based on global connectivity.

IPO Structure and Share Sale Details

The initial prospectus outlines an offering of approximately 555.6 million shares at an indicative price of $135, which would generate roughly $75 billion in gross proceeds. According to industry reports, an amended filing introduced a clause that SpaceX "may issue a significant amount of equity in connection with future transactions." It also set aside a portion of the offering for select employees to sell immediately. Analysts suggest this flexibility could enable strategic acquisitions or integrations involving other Musk-led companies, though the filing offers no direct confirmation.

The Significant TAM: Justifying the Valuation

To support its massive valuation, SpaceX presents what it terms a substantial Total Addressable Market (TAM) spanning space, connectivity, and AI. Critics, including renowned valuation expert Aswath Damodaran, argue this estimate is aspirational, placing SpaceX's actual equity value at a lower figure. Available sources describe the global space economy around $670 billion to $700 billion in 2026, with some forecasts citing a $1.8 trillion opportunity by 2035; they do not substantiate the claimed three-part split. Analysts describe the AI share as speculative given limited monetization history.

Inside the Google Compute Agreement

A significant factor bolstering future revenue is a major contract with Google. According to industry reports, Google has agreed to pay SpaceX substantial monthly amounts for access to GPU compute capacity in AI-affiliated data centers. This deal could inject significant cumulative revenue. However, because the payments are directed to SpaceX and not the AI division, the direct financial benefit to the AI division remains unclear pending further disclosures.

Investor Outlook and Key Considerations

As SpaceX proceeds toward its IPO, investors are left to weigh the company's multi-segment narrative against its astronomical valuation. The company's prospectus positions it as a powerhouse across rockets, satellites, and AI infrastructure. However, the viability of its substantial market claim and the justification for its $1.75 trillion price will ultimately be tested during investor roadshows and by the SEC's feedback on its filings.

What does SpaceX's S-1 filing reveal about its valuation and revenue?

According to industry reports, the filing puts the headline valuation at $1.75 trillion and shows significant revenue. Starlink dominates the top line, followed by Launch services and AI-related income. Analyst Aswath Damodaran, however, pegs the equity value at a lower figure, implying a substantial narrative premium that investors must accept to buy into the IPO.

Why is SpaceX emphasizing a large total addressable market?

The prospectus claims a substantial TAM to frame SpaceX as more than a rocket company. Available sources describe the global space economy around $670 billion to $700 billion in 2026, with some forecasts citing a $1.8 trillion opportunity by 2035; they do not substantiate the claimed three-part split. Critics point out that the AI slice alone would dwarf annual U.S. GDP, calling the estimate more aspirational than actionable. Media coverage notes S-1 documents are "notoriously optimistic," while economists label such claims as questionable.

How will the Google GPU agreement affect SpaceX's future cash flows?

According to industry reports, Google will pay SpaceX substantial monthly amounts for access to GPU hardware and supporting infrastructure. At full run-rate this represents significant annual revenue over the multi-year contract. The revenue is captured by SpaceX, not necessarily the AI division, so while the deal dramatically lifts near-term cash flow, it does not automatically translate into incremental AI revenue unless detailed inter-company agreements emerge.

What are the main risks investors face at this valuation?

Investors must weigh three core risks:

1. TAM credibility - a significant portion of the claimed TAM rests on still-nascent AI segments.

2. Governance - according to industry reports, amended filings reserve a portion of IPO shares without lockup for insiders, creating potential post-listing supply pressure.

3. Future equity dilution - the same amendment warns that SpaceX "may issue a significant amount of equity for future transactions," signaling possible dilution or tie-ins with other Musk ventures.

Which revenue stream is expected to grow fastest post-listing?

AI-linked services have the highest implied growth ceiling because even a fractional capture of the claimed substantial AI TAM would outsize current revenues. However, xAI has faced reported layoffs and departures, but the near-term figure is not verified by the provided original sources. Starlink remains the most predictable growth engine, while Launch is more cyclical and capped by global payload demand.