SpaceX expands AI cloud, targets $26.5 trillion market

Serge Bulaev

SpaceX is spending billions on AI infrastructure, building large GPU data centers and renting out extra computing power to other companies. This strategy has led to short-term losses but may create steady income as more customers sign up. The company believes the AI cloud market could reach $26.5 trillion, and it has already signed a big contract with Anthropic. However, profits might change from quarter to quarter, and the success of this plan seems to depend on how much demand there is from outside customers. SpaceX's approach could protect its profits if it owns the hardware, but there are risks if the market slows down.

SpaceX is aggressively expanding its AI cloud capabilities, a strategic pivot reshaping its financial profile by investing billions in GPU-dense data centers. By renting surplus computing power to other firms, SpaceX is creating a significant new revenue stream, despite initial losses. This analysis examines the scale of this investment, its early successes, and the competitive landscape.

How much has SpaceX spent on AI infrastructure?

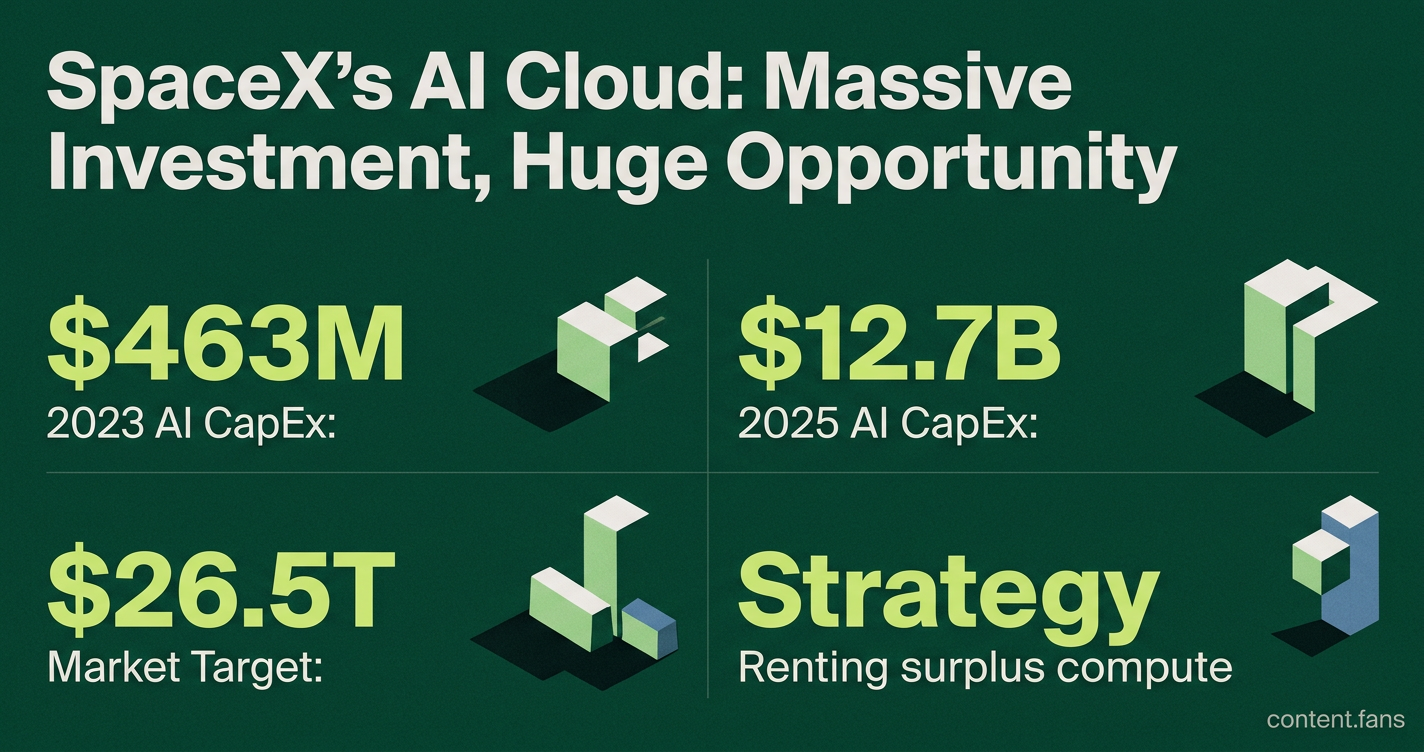

SpaceX has committed billions to its AI infrastructure, with capital expenditures reportedly rising from $463 million in 2023 to over $12.7 billion by 2025. This massive investment supports the construction of GPU-dense data centers, positioning the company as a major player in the AI compute market.

AI capital expenditures were approximately $5.6 billion in 2024. SpaceX spent $12.7 billion on AI in 2025 (per S-1 filing). While this build-out led to substantial operating losses, the xAI/AI segment reported massive capital expenditures with no confirmed profit and likely operating losses. However, analysts note that profitability remains volatile, tied directly to hardware acquisition cycles.

SpaceX's AI and Data Strategy: Massive Infrastructure Spend, Selling Compute, and an Emerging AI Cloud

SpaceX management is targeting a substantial market opportunity, focusing on enterprise AI services. The strategy involves using its proprietary data centers to train xAI's models and leasing the excess capacity. Industry reports suggest significant deals with major AI companies, and ongoing talks with other customers suggest a move toward a recurring subscription model.

Key features of the "neo-cloud" approach:

- Subsidizing data center capex with cash flow from Starlink.

- Leveraging vertical integration across launch, satellite bandwidth, and compute.

- Offering usage-based pricing tailored for AI training workloads.

- Planning for orbital compute modules according to industry reports.

Industry context and competitive pressure

Big Tech (Amazon, Alphabet, Microsoft, Meta) is projected to invest substantial amounts in AI infrastructure in 2026. SpaceX is an aerospace company focused on launch services and satellite internet (Starlink), not a competitor in the AI infrastructure market. AI funding in 2024 was substantial, with the demand for compute remaining high, but a growing GPU supply could trigger price wars and compress margins. SpaceX's strategy relies on owning its physical infrastructure to protect profits from falling API rates. While large-scale clusters create a powerful feedback loop - attracting major clients who fund further expansion - the high fixed costs pose a significant risk if external demand falters. Currently, major contracts provide a crucial buffer, covering a large share of depreciation expenses and suggesting a viable path to profitability.

What pushed SpaceX to increase AI infrastructure spending?

SpaceX's capital expenditures are not reported as a specific 'AI capex' line item increasing from $463M to $12.7B. The company's total capex is significantly higher and focused on aerospace and Starlink, not exclusively AI. Starlink is profitable, but specific operating cash figures require verification. This represents an aggressive reinvestment strategy, with a significant portion of Starlink EBITDA being channeled into AI hardware.

How does an aerospace firm suddenly become a cloud vendor?

The company's transition to a cloud vendor follows a "build-for-yourself, sell-the-excess" model. After building sufficient capacity for its own xAI models, SpaceX leases surplus infrastructure. Industry reports suggest significant deals with major AI companies. With pricing comparable to AWS spot rates and the unique benefit of ultra-low latency via Starlink, SpaceX has reportedly leased a substantial portion of its capacity, generating significant annualized revenue.

Is SpaceX chasing the same hyperscalers or a different niche?

SpaceX is carving out a niche as a "neo-cloud" provider, positioned between chipmakers and AI labs rather than competing directly with general-purpose hyperscalers. The company is targeting a substantial market for specialized vertical workloads like defense, orbital computing, and remote industrial applications where its low-latency satellite backhaul offers a key advantage. According to industry reports, there is significant demand for new compute capacity, and SpaceX aims to capture a meaningful portion of this demand.

Could this scale end in a price war?

A price war is a significant risk. With GPU supply potentially outpacing demand from a venture-funded market, spot prices are already falling. Industry reports suggest that lease rates have slipped, and if the combined substantial capex from Big Tech and SpaceX materializes, GPU-hour costs could drop significantly. Such a decline would threaten the profit margins SpaceX currently achieves on its leased hardware.

When do orbital data-centres enter the mix?

Orbital data centers are on the horizon according to industry reports. Utilizing Starship for launches, these solar-powered clusters could theoretically achieve very low break-even costs by eliminating real estate and cooling expenses. However, this futuristic model faces major hurdles: no customers have yet committed, and prohibitive insurance costs must be overcome.