Sanders Proposes $7 Trillion AI Fund with 50% Stock Tax

Serge Bulaev

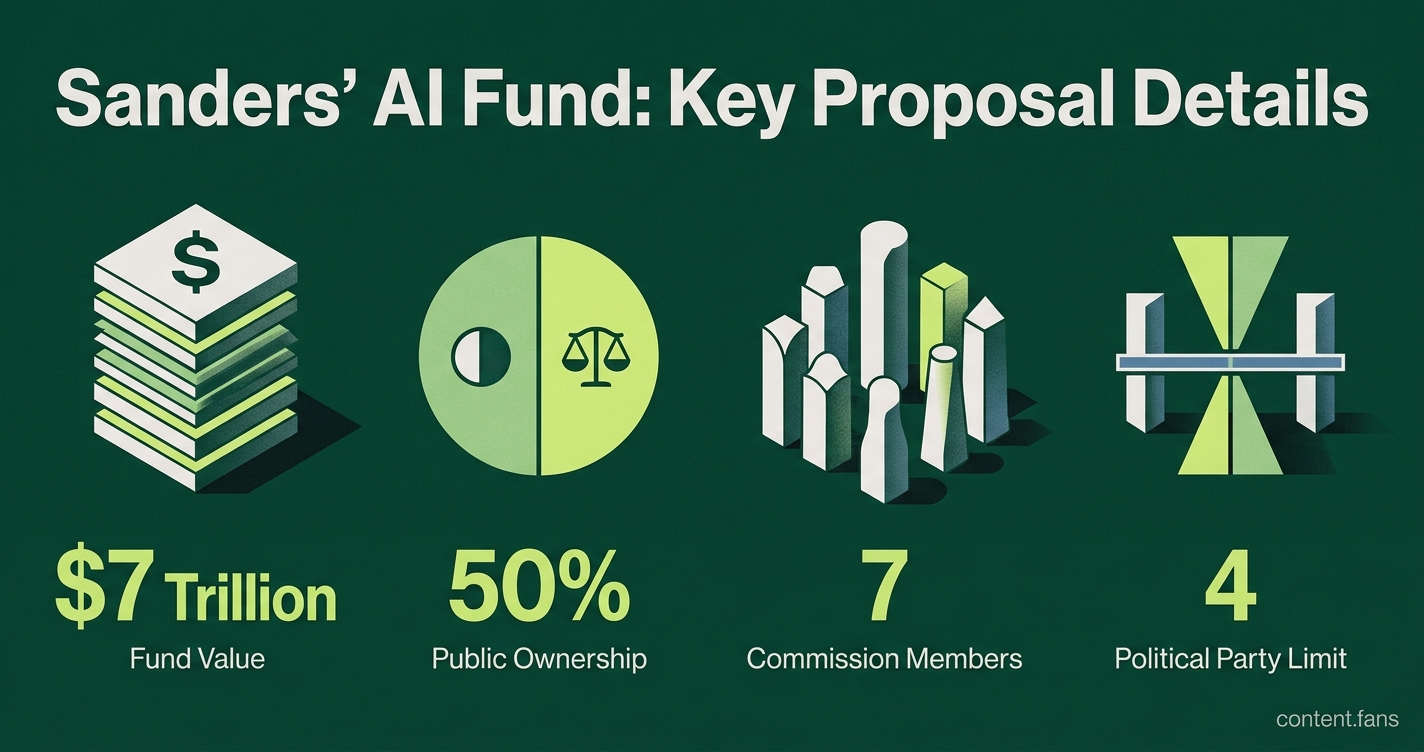

Senator Sanders has proposed creating a $7 trillion fund to give the public a 50% ownership stake in major AI companies by having them issue new shares to the government. An independent commission would manage the fund, focusing on worker rights, safety, fair competition, and environmental goals. The proposal might raise about $350 billion per year, possibly paying over $1,000 per person, but experts say actual payouts could be small at first since many AI companies are not yet profitable. The plan appears to face strong political opposition and legal questions, and some industry leaders suggest smaller alternatives. Early returns from the fund may depend more on long-term growth than immediate profits.

Senator Sanders has unveiled a landmark proposal for a $7 trillion AI fund, a plan seeking to give the public a 50% ownership stake in major artificial intelligence companies through a stock-based tax. The ambitious measure aims to redistribute the immense wealth generated by AI, though it faces significant political, legal, and economic challenges.

How the 50 percent stock tax would work

The proposal mandates that major AI companies subject to the tax transfer 50% of their equity (via a one‑time stock tax) into a sovereign wealth fund. This would transfer 50% of the equity of leading AI companies to a federal sovereign wealth fund, with the public receiving dividends from that fund, rather than direct ownership via new shares issued to the U.S. Treasury.

To satisfy the tax, companies would issue new shares rather than paying in cash. The bill also requires diversified technology conglomerates, such as Alphabet or Microsoft, to spin off their AI divisions into stand-alone companies before the equity transfer occurs, preventing them from shielding assets. The government could potentially levy additional equity taxes according to industry reports.

Independent Commission for Democratic AI

Management of the public's AI portfolio would fall to a new seven-member Independent Commission for Democratic AI, established within the Treasury Department. No more than four commissioners could belong to the same political party, and members would require expertise in fields including labor, national security, privacy, and sovereign fund management. This body would exercise all voting rights for the public's shares and could appoint directors to company boards.

Government‑appointed commissioners would manage the fund and use voting shares to block harmful decisions and push for policies that help the public, though the specific mandates and focus areas would be determined through the legislative process.

Dividends and public payments

The fund is projected to generate significant annual returns. According to Sanders, this revenue stream could finance substantial payments to the public. However, analysts caution that since many leading AI companies are not yet profitable, near-term cash dividends may be modest. The bill also allows surplus funds to support public programs in health care, housing, and education.

Political roadblocks

The proposal faces steep odds in the Republican-controlled Senate, where lawmakers have described the plan as partial nationalization that could deter private investment. Conservative commentators have also raised constitutional questions, suggesting a seizure of this magnitude could constitute an unlawful taking of private property. While former President Donald Trump has expressed some sympathy for public stakes in AI, he has not endorsed a 50% threshold. OpenAI CEO Sam Altman has also rejected the half-ownership concept, signaling openness only to smaller public-benefit mechanisms.

Economic context

The immediate financial returns of the fund would depend on the profitability of an industry still in its growth phase. Many AI companies face substantial costs due to massive research and infrastructure investments. For example, OpenAI generated about $2.1 billion in revenue by early 2026 and faces high costs, but available sources do not consistently confirm that it was definitively unprofitable at that point. Many companies in the sector are projected to require significant additional investment before achieving profitability. This economic reality suggests that early returns from the fund would rely more on long-term capital gains than on immediate cash payouts from dividends.