Report: Bad Banks, Support for Workers Aid Financial Cleanup

Serge Bulaev

Recent studies suggest that it may be possible to clean up bank balance sheets without causing mass layoffs if governments phase in loss recognition and support workers. Moving bad loans to a special bank appears to help lending more than just recapitalizing banks. Conditional support for banks, like tying new funds to restructuring goals, may improve results and reduce risks. Helping workers with training and moving costs might ease the impact of firm closures. Overall, transparency and careful timing seem important so that financial cleanup and worker support can work together.

A new report on financial cleanup finds that using bad banks combined with support for workers helps resolve non-performing assets without mass layoffs. This evidence-based approach allows governments to manage zombie firms and protect the financial system while mitigating social upheaval through phased loss recognition and targeted labor policies. This analysis synthesizes credible financial and labor market tools from recent cross-country studies, focusing on the effectiveness of bad banks, conditional recapitalization, and active labor market policies.

Segregating impaired assets

Recent evidence shows that segregating non-performing loans into a 'bad bank' and pairing financial sector cleanup with active support for workers is a viable strategy. This dual approach allows for orderly balance sheet resolution while mitigating unemployment impacts through targeted reskilling and mobility assistance programs.

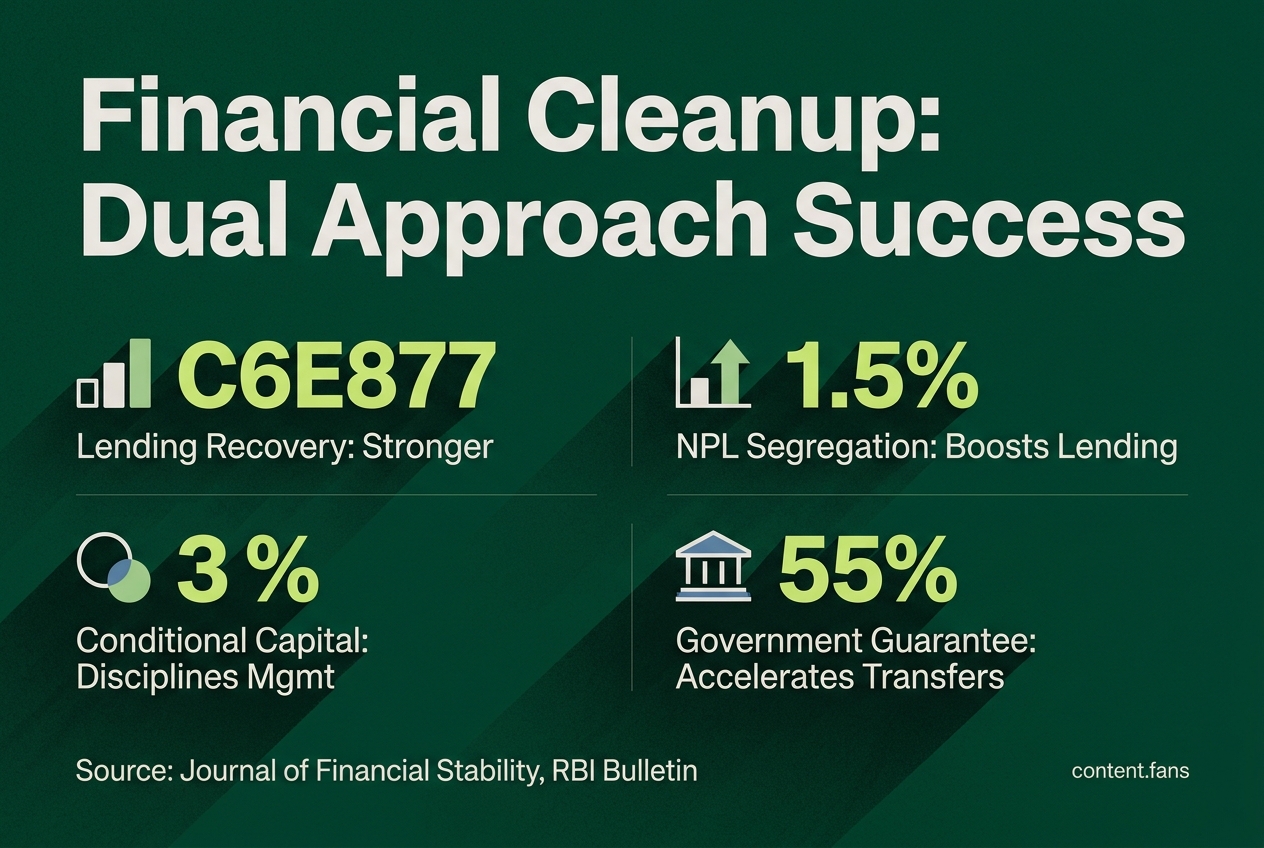

A key finding from a 2023 study in the Journal of Financial Stability is that transferring non-performing loans (NPLs) to a bad bank boosts subsequent lending, a contrast to simply recapitalizing banks which often led to shrinking credit portfolios (study on Europe's bad banks). While both strategies lowered funding costs, the lending recovery was significantly stronger when impaired assets were segregated. Similarly, India's central bank notes its National Asset Reconstruction Company Ltd. (NARCL) benefits from a government guarantee that accelerates transfers and reduces coordination issues, highlighting the importance of legal backing and swift capitalization (RBI Bulletin).

The timing of loss recognition is also critical. Experts advocate for announcing a multi-year schedule for booking losses, which gives banks time to raise private capital and reduces the immediate need for public funds. For instance, during past financial clean-ups where China announced significant capital injections into state lenders, linking fund tranches to specific restructuring milestones could have enhanced the process.

Conditional recapitalization

Conditionality is key to successful recapitalization. Model-based research on state-owned banks shows that linking capital transfers to performance disciplines management more effectively than unconditional grants, which can weaken restructuring incentives and increase welfare losses. In practice, India now ties new capital for public sector banks to tripartite agreements requiring austerity and non-performing asset (NPA) reduction targets. The provided source supports the general idea of government-backed cleanup mechanisms and linked support, with industry reports suggesting notable improvements in various risk metrics following implementation.

Nigeria provides a recent parallel. According to industry reports, the Central Bank's recapitalization framework requires affected banks to meet higher capital thresholds by choosing one of several options including capital injection, mergers/acquisitions, or license adjustment. Recognizing that this consolidation could lead to job losses, regulators have integrated support for displaced staff into the recapitalization packages.

Worker transition support

Because industrial regions bear the brunt of firm closures, effective worker transition support is crucial. The International Labour Organization (ILO) emphasizes that active labor market policies (ALMPs) work best when combining demand-driven training with mobility assistance. For example, case studies from European coal regions demonstrate higher re-employment rates when programs offered short, modular courses linked directly to employer vacancies. Industry reports note that transportation and housing stipends are vital for overcoming geographic barriers to re-employment.

Key Policy Recommendations from Research:

- Establish a legally-backed bad bank to transfer legacy NPLs within a fixed timeframe.

- Phase capital injections, linking each tranche to pre-defined restructuring benchmarks.

- Ensure transparency by publishing asset transfer prices and recovery progress to mitigate moral hazard.

- Implement demand-driven reskilling programs managed by local employment services.

- Provide practical mobility support, including subsidies for childcare, transport, and housing.

Transparency is the cornerstone of this integrated approach. Research on governance highlights that full disclosure - of asset transfer prices, bad bank governance, and labor re-entry outcomes - is essential for building public trust and maintaining social stability. Ultimately, financial cleanup and worker support are mutually reinforcing when implemented with clear timelines and explicit conditions.

What is a "bad bank" and why is it recommended for financial cleanup?

A national bad bank is a state-backed entity created to isolate and manage impaired assets from commercial lenders. Recent cross-country evidence shows that when bad banks are centrally coordinated, legally backed, and coupled with recapitalization, they restore credit growth faster than direct recapitalization alone. For example, studies covering European banking systems found that banks using bad banks showed stronger lending recovery compared to those only recapitalized. India's NARCL illustrates the model: NARCL was set up as a government-backed asset reconstruction company with a ₹30,600 crore guarantee to help resolve stressed assets and improve coordination in stressed-asset resolution.

How does conditional recapitalization differ from unconditional bail-outs?

Conditional recapitalization ties public capital injections to specific restructuring outcomes - such as NPA reduction targets, productivity benchmarks, or merger plans - whereas unconditional bail-outs provide funds with no strings attached. Recent recapitalization efforts in India and Nigeria show the difference in practice. In India, PSBs signed tri-partite MoUs that require austerity and NPA metrics before receiving any funds; in Nigeria, banks that miss the new capital thresholds must choose from several options including mergers or acquisitions. Early data suggests improvements in NPAs and higher provision coverage ratios under the conditional model.

Do active labor-market policies really help displaced workers?

Yes - but only when ALMPs are targeted, skills-oriented, and employer-linked. The most recent global stock-take finds that short, modular reskilling, transport-childcare-housing supports, and individual placement services outperform broad hiring subsidies. In Europe, post-crisis programs that embedded training in regional development strategies saw higher re-employment rates, while schemes relying mainly on wage subsidies showed weaker long-run effects. For future restructuring efforts, the best-performing packages combine employer partnerships with skill demand mapping to avoid costly mismatches.

What institutional safeguards reduce moral hazard in state-directed lending?

Research across emerging economies points to three pillars:

1. Transparent asset-transfer rules that publish the valuation criteria used when bad banks take over NPLs.

2. Governance reforms in state-owned banks, including independent boards and performance-linked management contracts, as seen in India's recent tri-partite MoUs.

3. Realistic resolution timelines backed by legal powers - e.g., India's NARCL can invoke Sarfaesi or IBC provisions to speed up recoveries, preventing the "evergreening" that plagued earlier cycles.

How large could the fiscal outlay be, and what safeguards ensure value-for-money?

According to industry reports, significant capital injections have been required in major banking cleanups; a similar order of magnitude could apply elsewhere. To protect public funds, the emerging playbook recommends:

- Phased recognition of NPLs tied to hard restructuring milestones.

- Sunset clauses for bad banks (usually 5-7 years) combined with recovery-linked remuneration.

- Public dashboards tracking both financial outcomes and job-placement rates from linked ALMPs, ensuring accountability to taxpayers and workers alike.