OpenAI reports $3.7B cash burn on $5.7B revenue in Q1 2026

Serge Bulaev

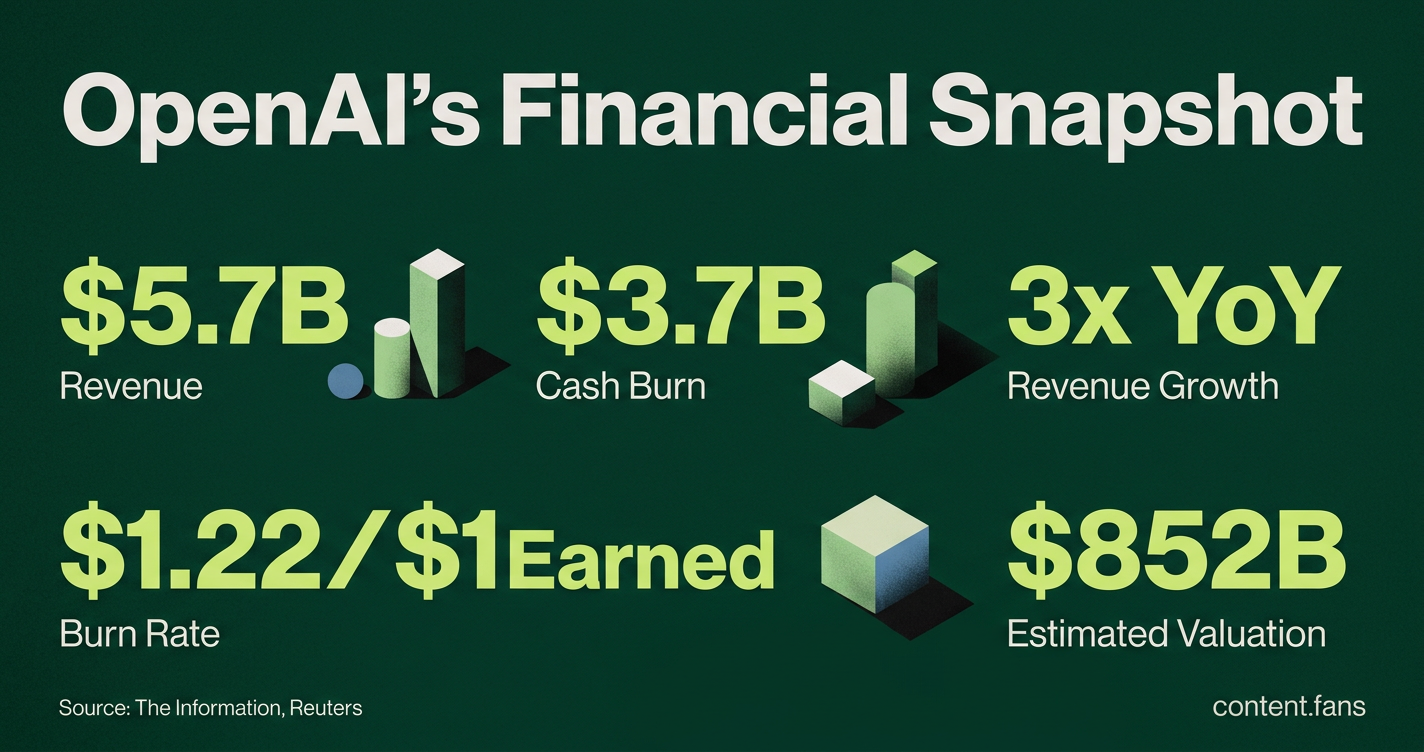

OpenAI reported $3.7 billion in cash burn and $5.7 billion in revenue for the first quarter of 2026, which may raise concerns for investors about an upcoming IPO. Despite rapid revenue growth, the company still operates at a large loss and does not expect to be profitable before 2030. Experts suggest that high spending on computing and infrastructure appears to drive these losses, even as some costs per task fall. Investors might want more information on contracts, costs, and future spending before making decisions. The situation suggests that while OpenAI is growing fast, its high costs remain a challenge.

OpenAI reports a $3.7 billion cash burn against $5.7 billion in revenue for Q1 2026, figures that heighten investor scrutiny over the financial viability of a potential IPO. These metrics, first detailed by The Information and confirmed by Reuters, underscore the immense capital required to develop frontier AI models, even as the company achieves explosive top-line growth.

Key Q1 2026 Financials

OpenAI's Q1 2026 results highlight a company in hyper-growth facing massive operational costs. While revenue tripled year-over-year to $5.7 billion, the firm simultaneously burned through $3.7 billion, driven primarily by the immense compute power and infrastructure required for its advanced AI models.

- Revenue: $5.7 billion, a threefold increase year-over-year

- Cash Burn: $3.7 billion, or $1.22 spent for every $1.00 earned

- Adjusted Operating Margin: - 122%, an estimated loss of $6.95 billion

- Cash Reserves: Significant funding following recent capital raises

While a Softonic summary notes that gross margin improved to 39%, the company does not forecast profitability before 2030. Operating costs continue to rise in lockstep with revenue, reinforcing the high-cost nature of its business.

IPO Prospects and Valuation Scrutiny

Sources indicate a March 2026 funding round valued OpenAI at approximately $852 billion, with an annualized revenue run rate exceeding $22 billion. OpenAI faces a market that now prizes capital efficiency over pure scale. For comparison, Anthropic's valuation/ARR ratio is unverified and likely higher than 13x, though secondary markets have pushed that multiple higher. Analysts argue that OpenAI's burn rate could temper appetite for a trillion-dollar IPO unless the company can present a clear path to cost control alongside its growth narrative.

The Economics of Compute-Driven Cash Burn

The reported losses are directly tied to escalating compute and infrastructure spending. While the cost for older models has plummeted significantly since 2022, frontier models remain expensive. According to industry reports, output tokens for models like GPT-4.5 can cost between $8 and $75 per million tokens.

Even with hardware improvements like NVIDIA's Blackwell GPUs offering efficiency gains of approximately 10-12x (still in beta testing), OpenAI has told shareholders it expects to spend "tens of billions in a single year" on compute. This indicates that the sheer scale of its operations, rather than per-unit cost, is the primary driver of its current cash burn.

What Investors Will Demand Ahead of an IPO

To justify its premium valuation in a public offering, OpenAI will need to provide exceptional transparency in its S-1 filing. Industry reports suggest AI platforms typically trade at elevated multiples, with premiums for those meeting the "Rule of 40" (growth rate + profit margin ≥ 40%). OpenAI's negative margin currently disqualifies it.

Investors will therefore demand detailed disclosure on:

1. Contract durability and enterprise customer retention.

2. Long-term GPU purchasing commitments and obligations.

3. Cost-per-inference trends broken down by model tier.

4. Governance structure and organizational changes.

Clarity on these points is essential to reconcile OpenAI's high private multiple with public market expectations for sustainable cash flow.

What drove OpenAI's reported cash burn in Q1 2026?

According to reports, OpenAI spent $1.22 in cash for every $1.00 of revenue, with the largest share going to compute, research, and infrastructure. The company told investors it will spend "tens of billions in a single year" on these items and does not expect to turn profitable until the end of the decade.

How does the cash burn affect OpenAI's IPO narrative?

Public-market investors now prioritize capital efficiency over pure growth. Market analysis suggests that companies with better capital efficiency ratios are favored, meaning OpenAI's current metrics could delay or depress its public debut unless it can show a clear path to positive unit economics.

What metrics should investors watch beyond revenue?

Watch gross margin per model, cost per inference, and compute-spend ratio. While inference costs have decreased significantly due to hardware improvements, output tokens typically cost 2 - 4× more than input tokens. These ratios will determine how fast OpenAI can close its -122% non-GAAP operating margin.

How much cash runway does OpenAI have?

OpenAI's exact cash position is not publicly disclosed, but the company has raised significant capital through multiple funding rounds, including substantial investments from Microsoft and other partners. This provides considerable runway for continued operations and development.

What valuation multiple is realistic for an AI company with high burn?

AI valuations in 2026 remain elevated, though specific multiples vary by company and market conditions. OpenAI's recent private funding rounds suggest premium valuations that require Rule-of-40 compliance (growth + profit ≥ 40%) to sustain in public markets. Until OpenAI improves its capital efficiency metrics, expect secondary-market scrutiny and S-1 focus on long-term compute contracts.