OpenAI expects to burn $100B before 2030 free cash flow

Serge Bulaev

OpenAI expects to spend over $100 billion before it might start making more money than it spends around 2030. The company's own models suggest it will have negative free cash flow until then, and this forecast has been revised upward from earlier estimates. Most of the costs appear to be for powerful computer chips, including a deal for over $20 billion with Cerebras. Analysts warn that more years of losing money could lead to more investors owning pieces of OpenAI, which may create risks. There is still uncertainty if OpenAI's possible large profits in 2030 will be enough to balance out years of high spending.

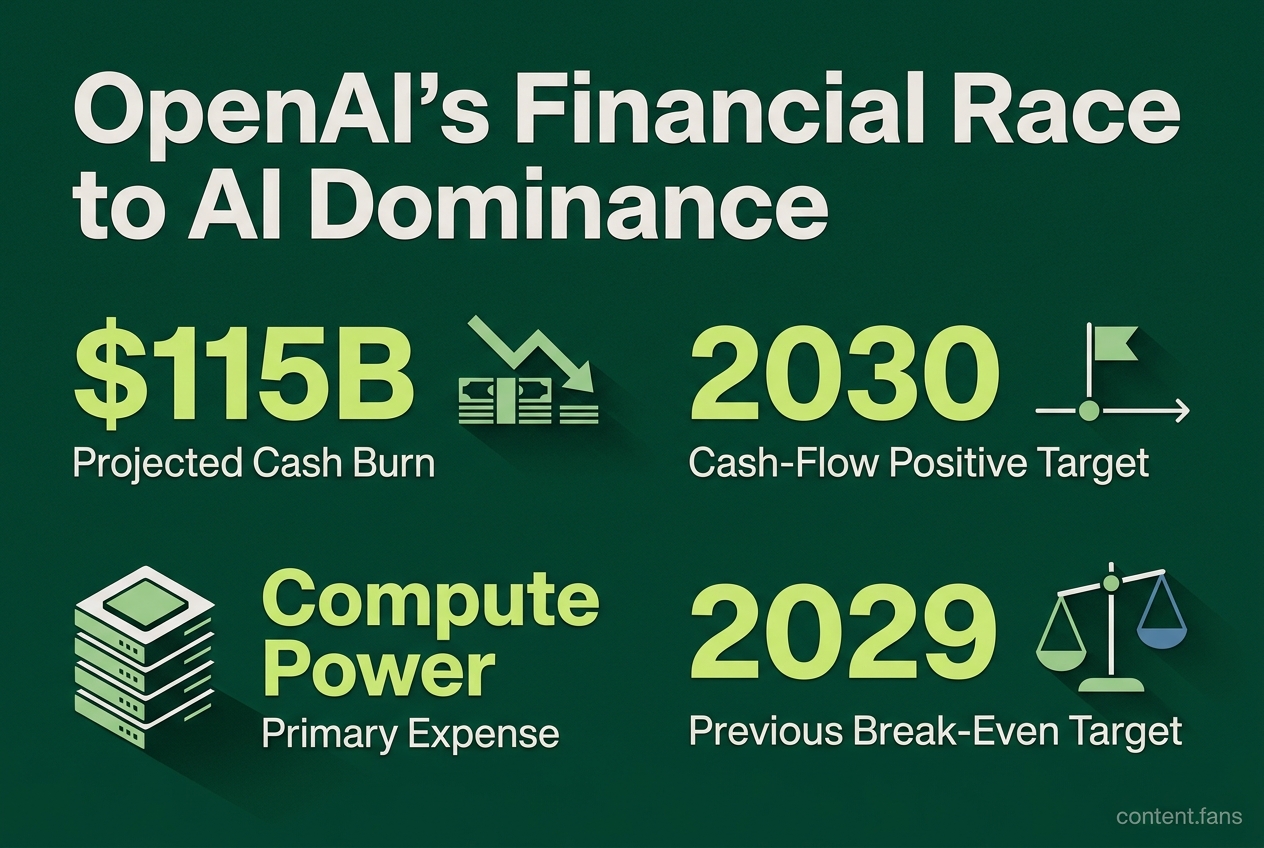

OpenAI was reported to expect roughly $115 billion in cash burn before becoming cash-flow positive in 2030. This substantial capital expenditure, which includes significant chip deals according to industry reports, underscores the immense financial hurdles in the AI race and is already a central topic in pre-IPO investor discussions.

Internal financial models project negative free cash flow until 2030. This date represents a slip from earlier forecasts, which had targeted 2029 for break-even (Reuters). Leaked slides summarized by MLQ.ai indicate that this revised timeline involves substantial additional cash burn compared to previous estimates, placing further pressure on the company's valuation (MLQ.ai).

Cost trajectory through 2030

OpenAI is forecast to spend substantial amounts in a sustained period of negative cash flow until approximately 2030. The primary driver of this massive expenditure is the acquisition of computational resources, including custom AI processors, necessary for developing and operating frontier artificial intelligence models.

The company's primary expense is compute power. According to industry reports, significant deals with Cerebras for custom AI chips signal a strategy to control hardware capacity directly, viewing it as a more cost-effective long-term solution than renting cloud GPUs. While talks with other vendors like Broadcom and Nvidia are reported, details remain unconfirmed.

Financial analysts warn that extending the period of negative cash flow increases the risk of shareholder dilution, as funding will likely require issuing more equity or accepting structured investments from partners like Microsoft. A delayed break-even point directly impacts valuation, lowering discounted cash flow models unless offset by higher projected revenue.

Competitive backdrop

OpenAI's spending occurs within a fiercely competitive landscape. Its rivals also face massive capital requirements, but often within larger corporate structures. According to industry reports, major tech firms are planning substantial infrastructure investments, with companies like Alphabet dedicating significant portions of their capex to AI initiatives. While competitor Anthropic is reportedly generating substantial revenue, it remains a high-burn entity. OpenAI's standalone nature makes its financial path more transparent than that of divisions like Google DeepMind, but its spending is not an outlier in the industry.

What investors are watching

Key metrics and events that will signal OpenAI's financial trajectory include:

- Future Compute Deals: The scale and timing of new contracts for AI hardware.

- Profitability Timeline: Any further delays to the projected free cash flow targets.

- Revenue Growth: The company's ability to meet or exceed its projected revenue targets.

- Partner Investment: The willingness of capital partners like Microsoft to provide further funding without demanding additional governance controls.

While OpenAI's leadership justifies the enormous spending as a necessary investment to build frontier AI models, the key question for investors remains. They must weigh a decade of unprecedented cash burn against the potential for substantial profits post-2030, with projections suggesting significant positive cash flow once profitability is achieved.

How much cash does OpenAI expect to burn before becoming free-cash-flow positive?

According to industry reports, OpenAI's latest internal projections show the company will burn substantial amounts in cumulative free cash flow before it turns positive, with the first year of positive cash flow now expected around 2030. Earlier reporting had suggested different timelines, but updated forecasts suggest the break-even point has been pushed out. The same forecasts estimate significant positive cash flow once breakeven is reached, implying a sharp swing in financial performance.

What does a single chip deal look like at this scale?

According to industry reports, OpenAI has significant chip agreements with Cerebras worth substantial amounts. Beyond that, the company is described as lining up multi-billion-dollar supply arrangements with Broadcom, Nvidia, AMD, Intel, TSMC and Microsoft, although most of those terms remain unconfirmed in primary filings. Taken together, the hardware commitments underscore that training and inference costs for frontier models now require substantial capital budgets.

How does OpenAI's projected burn compare with competitors?

According to industry reports, major U.S. cloud and AI infrastructure providers plan to spend substantial amounts on data-center build-outs, chips and power. OpenAI's revenue projections are estimated to be significant, while Anthropic is reportedly generating substantial revenue and Google DeepMind's spending is shielded inside Alphabet's major capex plans. In short: pure-play labs are chasing a revenue base that is still smaller than the combined infrastructure bill, making profitability timelines highly sensitive to any delay in model monetization.

What happens to IPO valuation if free-cash-flow breakeven slips?

Using a simple discounted-cash-flow lens, pushing the positive-cash-flow date further out lowers intrinsic value because investors must fund additional years of heavy burn. Moreover, revised projections add substantial extra cumulative burn compared with earlier forecasts, which increases the risk of greater dilution from follow-on funding rounds or convertibles. Unless revenue expectations and long-term margins rise in tandem, the slippage alone can impact present equity value under typical discount-rate assumptions.

Why is hardware development a critical focus?

According to industry reports, OpenAI is exploring consumer hardware development, reportedly including voice-first products developed with industry partners. Manufacturing partnerships are reportedly being explored with traditional supply-chain vendors, and development timelines are being established for potential retail availability. If these efforts progress, investors will get concrete cost and unit-economics data, turning an abstract capex story into a tangible hardware business model ahead of any prospective IPO.