OpenAI, Anthropic Pivot to Enterprise; B2B Nears 40% Revenue

Serge Bulaev

OpenAI, Anthropic, and Google are focusing more on selling AI to businesses, which may soon bring in as much revenue as their consumer products. Analysts say this shift makes sense because companies can spend more and sign long-term contracts. OpenAI says over 40 percent of its revenue now comes from businesses, and Anthropic seems to be growing even faster in this area. To attract companies, these labs are adding more security, compliance, and special features that big organizations want. The market may keep changing as businesses try different AI providers and as labs form new partnerships with other tech companies.

The OpenAI, Anthropic pivot to enterprise is reshaping the AI industry, as major labs like Google also steer their roadmaps toward corporate buyers. This move toward B2B monetization focuses on securing high-value, long-term contracts and building defensible features, transforming everything from hiring to product compliance.

Why the enterprise buyer matters

Leading AI labs are prioritizing enterprise clients due to their significant spending power, ability to sign multi-year contracts, and demand for specialized features. This B2B focus provides a more stable and scalable revenue stream compared to consumer markets, justifying the investment in enterprise-grade security and compliance.

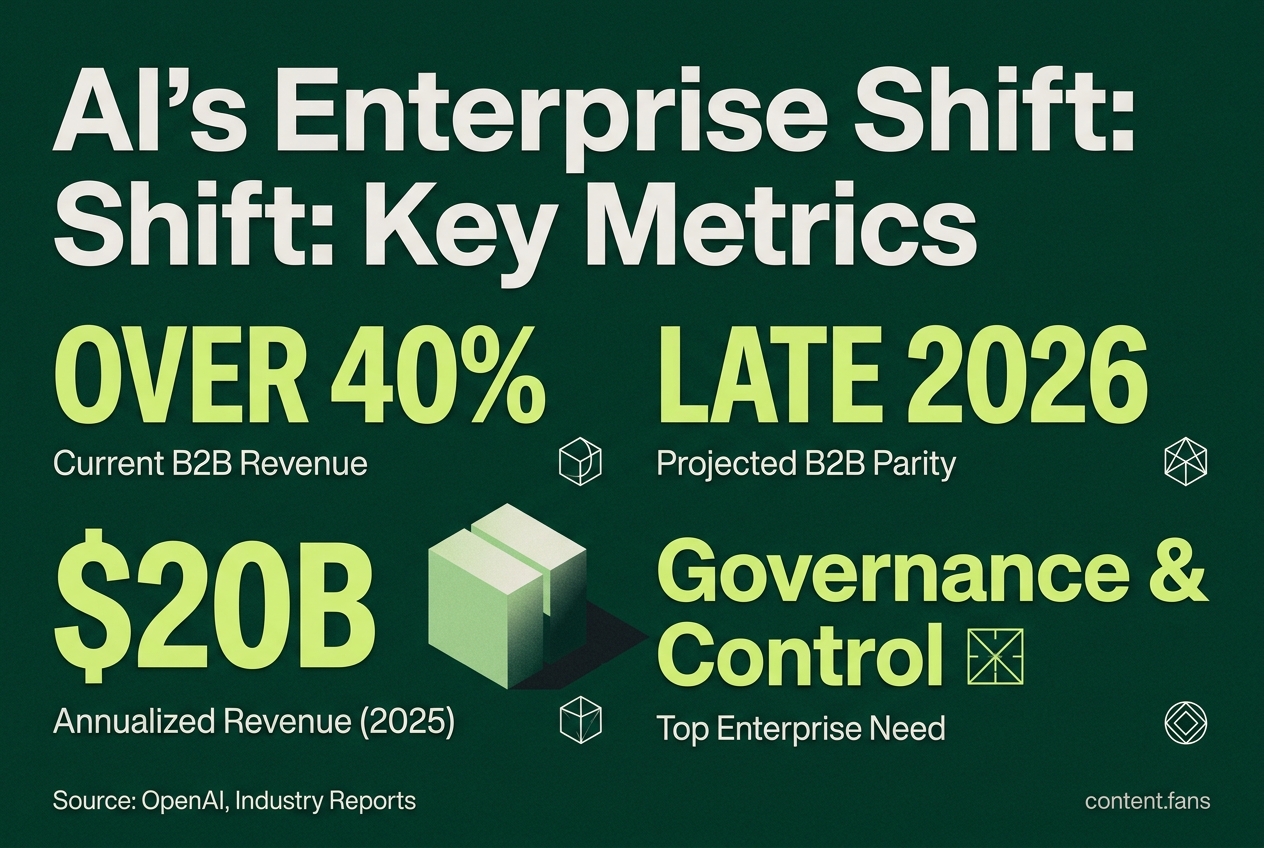

Enterprise clients already deliver over 40% of revenue, and that share is projected to reach parity with consumer lines by late 2026, according to an update on the OpenAI site. This B2B focus is a key growth engine, with annualized revenue reportedly crossing $20 billion in 2025. Anthropic is also gaining ground rapidly, with industry reports suggesting growing enterprise adoption across multiple AI providers.

Monetization stacks now in play

Major AI labs have converged on a multi-tiered monetization strategy to serve everyone from developers to large enterprises. These revenue schemes typically include:

- Metered API usage for developers

- Seat-based SaaS tiers such as ChatGPT Team or Gemini Business

- Custom enterprise agreements that bundle security reviews, data residency, and uptime SLAs

- Professional services or co-innovation pilots

Industry reports suggest OpenAI has secured a significant number of paying business users, with a substantial portion of enterprise customers representing high-value accounts.

Features enterprises insist on

According to industry analysis from firms like StackAI, governance and control are now the primary factors in enterprise adoption, surpassing raw model quality. Businesses now require features like detailed audit trails, permission-aware data retrieval, human approval checkpoints for automated tasks, and sovereign data controls. This emphasis on security, also highlighted by IBM as a top challenge, is shaping product development. OpenAI now markets ChatGPT Enterprise with SOC 2 certification, while Google integrates Gemini with existing Google Cloud security policies. This focus is also evident in hiring, with a surge in roles for solution architects and governance specialists.

Competitive dynamics through 2026

While market-share reports vary, the competitive landscape is clearly shifting. An a16z analysis indicates that while a majority of CIOs use OpenAI in production, competitors like Anthropic and Gemini are gaining wallet share. Infrastructure providers such as Microsoft, AWS, and IBM remain pivotal, offering the compute, data platforms, and sales channels that AI labs need to reach enterprise customers. This reality suggests future monetization will heavily rely on partnerships. Firms like Databricks and Salesforce are already reselling or embedding frontier models, giving labs access to corporate budgets through established vendors. For businesses, this means more choice; for AI labs, it confirms the enterprise buyer is their new priority.

What share of OpenAI's revenue now comes from enterprise customers?

More than 40% of OpenAI's revenue now originates from enterprise deals,up from a small minority just two years ago,with the company stating it is "on track to reach parity with consumer revenue by the end of 2026."

Sources: OpenAI official announcement and Sacra revenue breakdown.

How is OpenAI monetizing B2B clients?

OpenAI has built a multi-tier stack that blends subscription, usage, and services revenue:

- ChatGPT Enterprise - custom-priced deployments for large firms

- ChatGPT Team / Business - per-seat plans for smaller organizations

- API usage - token-based billing for developers embedding GPT models

- Premium consumer tiers (e.g., ChatGPT Pro) that expand ARR without diluting the core enterprise push

This layered approach has helped land a significant number of paying business users and enterprise customers, with many high-value accounts spending substantial amounts annually.

Sources: Sacra revenue model and LinkedIn summary of OpenAI Enterprise traction.

Which enterprise-grade features are moving to the top of product roadmaps?

Enterprise buyers are shifting vendor priorities toward governance, compliance, and control:

- Auditability - logs that answer "who changed what, when, and why"

- Sovereign data controls - region-locked storage and cross-border risk mitigation

- Scoped permissions - retrieval and tools that respect least-privilege access

- Human-in-the-loop gates for higher-risk agentic workflows

These requirements now outweigh raw model performance in procurement decisions.

Sources: Industry analysis from StackAI and IBM research on AI adoption barriers.

Who leads the enterprise AI usage market today?

Industry reports suggest competitive dynamics are shifting, with Anthropic gaining significant ground in enterprise adoption alongside OpenAI and Google.

In parallel, an a16z survey of CIOs still places OpenAI as the "clear enterprise leader today" in production deployments, while noting that Anthropic and Google are rapidly gaining wallet share.

Sources: Industry reports and a16z enterprise AI analysis.

What common hurdles still slow enterprise AI rollouts?

Despite vendor investment, buyers report five consistent blockers:

1. Data quality and fragmentation - Original sources support 52% for data quality and availability as the biggest AI adoption challenge, and 57% for data fragmentation as a digital-transformation barrier

2. Legacy system integration - Integration of AI with existing systems and data silos remains a common barrier

3. Skills gaps across product, risk, and platform roles

4. Workflow redesign failure - AI is bolted on rather than transforming processes

5. ROI justification - proving financial return before company-wide scale

A significant gap remains between pilot success and regulated production scale, with many organizations lacking mature governance frameworks for AI agents.

Sources: Industry research on AI adoption statistics and enterprise best-practices guides.