OpenAI, Anthropic, Google Pivot to Enterprise AI for Revenue Growth

Serge Bulaev

OpenAI, Anthropic, and Google seem to be focusing more on enterprise AI to grow their revenue, instead of just selling to consumers. Their new products and services are aimed at business needs like compliance, data security, and easier cloud deployment. OpenAI reportedly made a lot of money from business contracts, while Anthropic stands out for its data governance, and Google has combined its AI tools into a new platform for building AI agents. How companies charge for these services may include usage fees, seat licenses, and platform subscriptions. It appears the next big changes in AI will be shaped by what businesses need, especially around data rules and managing many AI agents.

The strategic pivot to enterprise AI by OpenAI, Anthropic, and Google signals a revenue-first era for the industry. This shift away from pure consumer subscriptions is reshaping product lines and revenue models around developer APIs, SaaS seats, and partner services, prioritizing business buyers. This pattern indicates future AI innovation will focus on enterprise needs like compliance, agent governance, and multi-cloud deployment, not just novelty chatbots.

OpenAI: usage-based cash engine

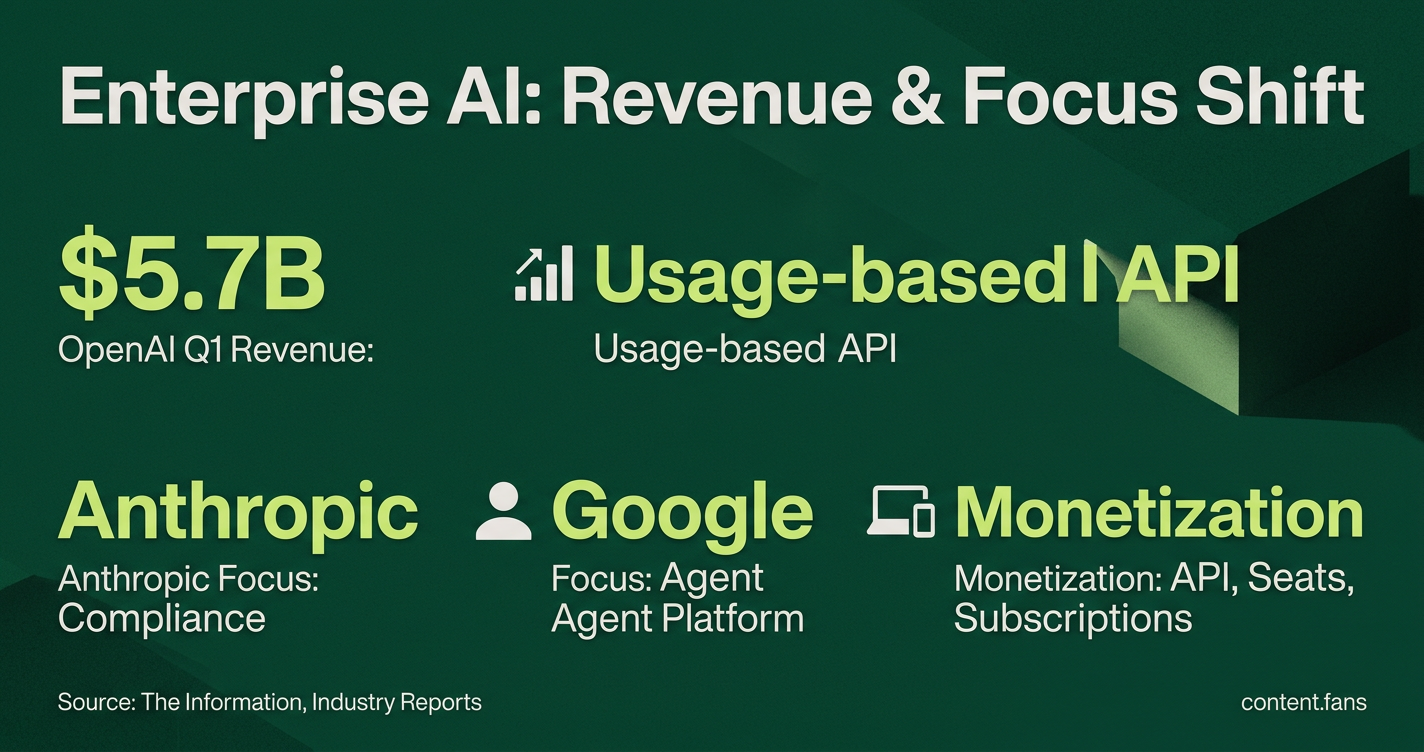

OpenAI's Q1 2026 revenue was $5.7 billion (The Information), though enterprise contracts' exact contribution remains unclear from verified sources. This revenue stems from ChatGPT Enterprise seats, developer tools, and its widely adopted pay-as-you-go API. To reduce sales friction, OpenAI is reportedly collaborating with consultancies to scale proofs of concept into full deployments.

These companies are targeting enterprise customers for the size and stability of revenue they represent. Predictable, contract-based B2B income provides a reliable path to cover massive compute costs and satisfy investors, contrasting with the more volatile consumer market and demonstrating a clearer path to profitability.

Anthropic: compliance as product

Anthropic targets regulated industries by productizing compliance. According to industry reports, the company offers zero data retention policies and focuses on ensuring customer data is not used for training. Features like access controls and analytics appeal to finance and healthcare buyers who require strict audit trails. Industry observers note Anthropic's emphasis on data governance compared to competitors.

Google Cloud: the agent platform pivot

According to industry reports, Google has been consolidating its AI efforts, with significant developments in its enterprise AI platform offerings. This unified approach combines development tools for both no-code users and engineers. Google's pitch focuses on application building, offering buyers features like improved performance and access to multiple models without needing to manage underlying infrastructure.

How the money is captured

- Usage-based API calls remain the default for model access.

- Seat-based licenses drive enterprise revenue across platforms.

- Platform subscriptions wrap orchestration, retrieval, and governance into predictable spend.

- Services partners collect integration fees when enterprises need data prep or prompt design.

This hybrid monetization model gives vendors upside from workload spikes while offering procurement teams the comfort of forecastable budgets.

Competitive signals

- Regulation-Driven Roadmaps: Features are increasingly dictated by regulated industry needs, including HIPAA compliance and EU data residency.

- Advanced Agent Management: As use cases mature beyond simple chat, sophisticated agent management is becoming a key competitive differentiator.

- Trust vs. Scale: While hyperscalers use their cloud footprint for distribution, specialized providers often win on trust, especially in sectors with sensitive data.

Margin profiles remain a key question. OpenAI burned $3.7 billion in Q1 2026 with a 122% non-GAAP operating loss margin, highlighting massive GPU and inference spending. Google's in-house TPU pipeline could provide a cost advantage, while Anthropic's partnership with Google Cloud TPUs suggests a blended economic model.

What is clear is that enterprise demand is fundamentally reshaping the AI stack, prioritizing governance, multi-agent orchestration, and hybrid-cloud controls. While consumer chatbots built brand awareness, the future of AI is being defined by contracts negotiated in enterprise procurement.

Why are OpenAI, Anthropic, and Google pivoting so aggressively toward enterprise customers?

The short answer is size and stability of revenue. OpenAI's Q1 2026 revenue reached $5.7 billion, with enterprise accounts representing a significant and growing portion of that total. OpenAI burned $3.7 billion in Q1 2026 with a 122% non-GAAP operating loss margin. Predictable, contract-based B2B income represents an important revenue stream as companies work to cover compute costs and satisfy investors.

What monetization models are emerging inside large organizations?

Industry reports suggest companies are focusing on multiple revenue streams:

- Usage-based APIs - pay-per-token for model access

- Seat-based SaaS - per-user licenses for chat or copilot products

- Platform subscriptions - annual bundles covering orchestration and governance

- Professional services - implementation and consulting work

The fastest-growing segment appears to be consumption plus committed spend: enterprises lock in predictable budgets while vendors keep upside from heavier usage.

Which enterprise-grade features are becoming important in recent deals?

According to industry reports, buyers increasingly prioritize governance, location control, and data protection alongside model accuracy.

| Vendor | Key enterprise features |

|---|---|

| Anthropic | Zero data retention - inputs and outputs are not stored after API calls |

| Google Cloud | Data residency controls and governance tools for enterprise deployment |

| OpenAI | Enterprise compliance features and access controls for business users |

These controls are becoming increasingly important as security requirements drive vendor selection decisions.

How do the three companies differentiate when selling to the same CIO?

Think of different market segments:

-

Regulated industries (finance, healthcare, government)

Anthropic focuses on this space with its safety-first approach and data protection promises. -

Cloud-native enterprises

Google Cloud leverages its existing cloud relationships and enterprise platform capabilities. -

Developer-first companies

OpenAI leads with its API ecosystem that many companies have already integrated.

What does this shift mean for buyers planning enterprise AI budgets?

Industry analysts expect vendor consolidation as organizations move from experimental pilots to production deployments. Many CIOs report managing multiple AI initiatives across different vendors. The trend appears to favor selecting one primary platform partner and one foundation-model provider under committed-spend agreements. Contracts are evolving from small pilots to larger, multi-year platform deals that bundle compute, models, and professional services.

Bottom line: Enterprise AI is moving from experimentation to production deployment, and vendors that cannot satisfy audit, compliance, and predictability requirements may struggle to win the largest enterprise contracts.