NVIDIA Reports $81.6B Quarterly Revenue, Data Center Sales Hit $75.2B

Serge Bulaev

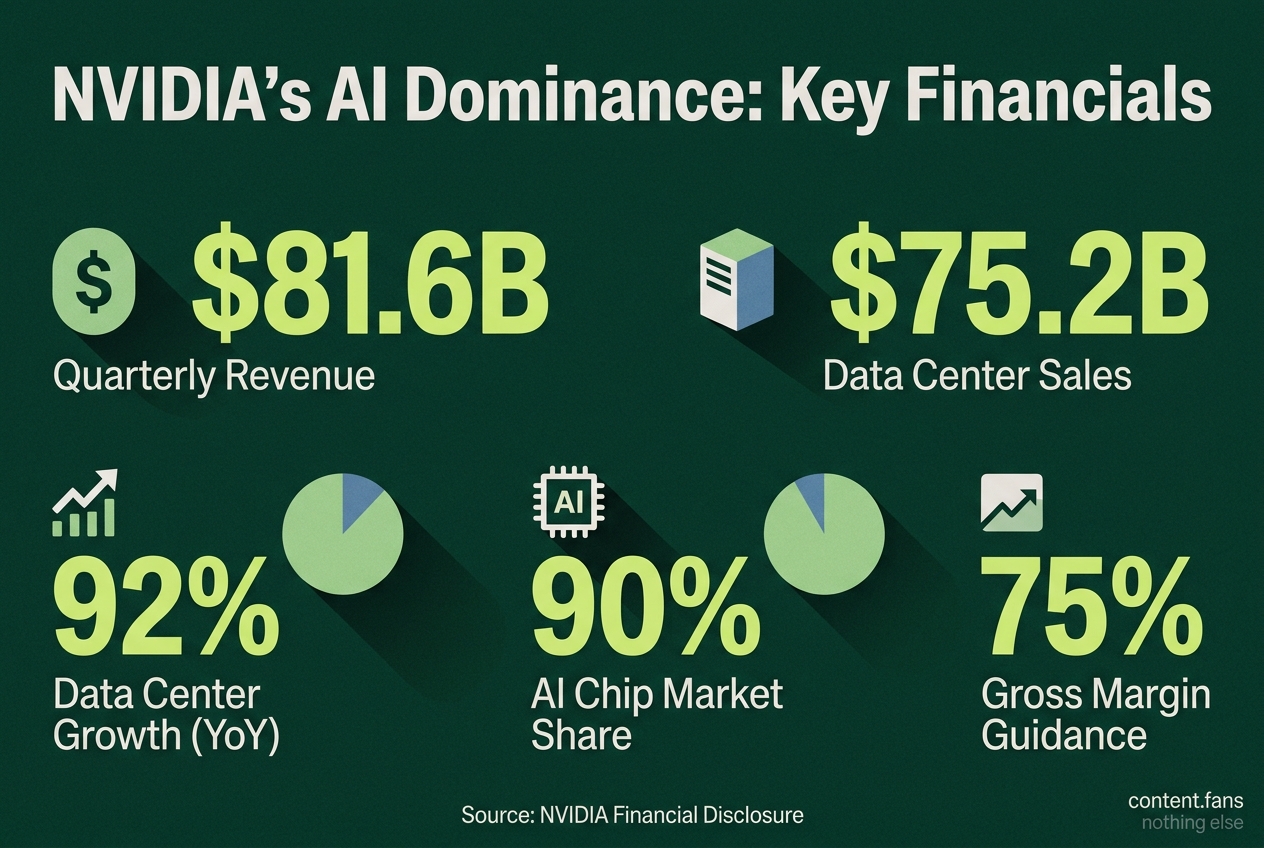

NVIDIA reported $81.6 billion in quarterly revenue, with $75.2 billion coming from its data center sales, which rose 92 percent from last year. The company's gross margin for the quarter was close to 75 percent, and its future guidance suggests revenue could reach $91 billion in an upcoming quarter. NVIDIA appears to hold about 90 percent of the AI chip market, though some sources project this might slowly drop to 87 percent by 2027. Factors like new competitors, changing regulations, and how buyers use AI may change NVIDIA's profits and market share in the future.

In its latest financial disclosure, NVIDIA reported $81.6B in quarterly revenue, with data center sales hitting $75.2B, extending a growth streak that is reshaping the AI infrastructure market. Data center revenue climbed 92 percent year-over-year, driven by accelerated demand from hyperscalers and enterprises for AI compute clusters.

The company's outlook signals continued momentum, with guidance for the upcoming quarter projecting revenues of approximately $78.0 billion (±2%) and gross margins holding near 75 percent, according to a Reuters report link. This strong forecast suggests analysts see persistent demand for NVIDIA's products, even as competition in the AI chip market intensifies.

Data center demand fuels record scale

NVIDIA's record revenue is primarily driven by its data center segment, which represents a significant portion of its total revenue for fiscal 2026. This surge reflects the immense, ongoing investment by cloud providers and large companies in building out the computational power required for AI.

For the full fiscal year 2026, NVIDIA's total revenue hit $215.9 billion, with data center products contributing $197.3 billion, according to the company's newsroom link. The sheer scale is notable, as the data center division's quarterly revenue represents substantial market presence. According to industry reports, NVIDIA maintains a dominant position in the AI accelerator market, though competitors are gaining traction.

Key FY2026 metrics:

- Total revenue: $215.9 billion

- Data center revenue: $197.3 billion (up substantially year over year)

- Sequential Q3-to-Q4 data center growth: significant increase

These figures underscore NVIDIA's strong pricing power in a market where demand continues to outstrip supply.

Competitive landscape and pricing power

NVIDIA's commanding position is widely recognized, with reports noting it "holds an astonishing 90 percent market share in AI chips" link. While competitors like AMD, Intel, and custom silicon from hyperscalers are gaining traction, NVIDIA maintains significant leverage. Its advantages in time-to-market, integrated networking, and the mature CUDA software ecosystem create a powerful lock-in effect. Though customers may seek to diversify suppliers for better prices, NVIDIA's performance leadership and robust development tools continue to justify its premium pricing.

Margin resilience at 75 percent guidance

Maintaining gross margins near the 75 percent guidance will depend on several key factors. Investors are closely watching the pace of hyperscaler capital expenditures, the performance gains of competing accelerators, and the balance between AI training and inference workloads. The interplay of these variables will determine if NVIDIA can sustain its current scale, ecosystem advantages, and pricing power.

Why market fragmentation matters

Geopolitical factors introduce further complexity and are leading to market fragmentation. Export controls on advanced GPUs, coupled with sovereign AI initiatives and data residency requirements, are influencing the location of training clusters and the deployment of inference capacity. As nations and regions prioritize domestic compute capabilities, the market could see a shift toward regional clouds and edge devices, potentially diversifying the accelerator landscape.

How did NVIDIA achieve $81.6 billion in quarterly revenue and what drove the $75.2 billion data-center surge?

The company posted $81.6 billion in quarterly revenue and $75.2 billion in data-center sales, a 92 % year-over-year jump. The outsized performance stems from continued mass deployment of AI training and inference clusters by hyperscalers, sovereign clouds and large enterprises. NVIDIA's single-quarter data-center revenue represents substantial market presence, illustrating both the scale of AI infrastructure demand and the company's dominant accelerator position.

What does the fiscal 2026 full-year picture look like and how much came from data-center?

For fiscal 2026, NVIDIA reported $215.9 billion in total revenue, with $197.3 billion coming from the data-center segment - a substantial increase versus the prior year. Put differently, the vast majority of revenue last year originated from data-center products and services, underlining how central AI compute has become to the company's financial engine.

How is the AI infrastructure market fragmenting and why does NVIDIA still dominate?

Markets are splitting along three axes:

- Workload - heavy training clusters vs latency-sensitive inference nodes

- Openness - proprietary CUDA stacks vs emerging open alternatives

- Geopolitics - export rules and sovereign-capacity initiatives

Despite this segmentation, NVIDIA maintains a dominant position in the AI accelerator market in 2026, according to industry reports. While analysts project market share may face growing competition as Google TPU, AMD MI and custom ASIC volumes rise, the CUDA software lock-in and full-platform sales model help preserve pricing power and customer stickiness.

Can NVIDIA maintain its ~75 % gross margin in FY2027 amid rising fabrication costs?

Guidance for the upcoming quarter points to gross margins near 75 %, essentially unchanged from the most recent quarter. Key supports include:

- Premium pricing on new Blackwell-generation systems constrained by limited supply

- Integrated hardware + networking + software bundles that raise blended ASPs

- Strong hyperscaler demand absorbing higher wafer and advanced-packaging costs

Management has explicitly excluded any China data-center revenue from the outlook, suggesting margin resilience is being delivered from other regions without price concessions.

What is the outlook for the next quarter and how is investor confidence measured?

Official guidance is set at $78.0 billion in revenue, plus or minus 2 %, representing strong growth expectations. Combined with the unchanged 75 % gross-margin target, the numbers signal management's confidence that tight supply of next-gen AI systems will outstrip any near-term competition or cost inflation. Investors watch the margin line as the primary barometer of pricing power; if margins stay at or near the top of the 75 % band, bullish sentiment is likely to persist.