New Report Details How Financial Regulators Audit AI Decisions

Serge Bulaev

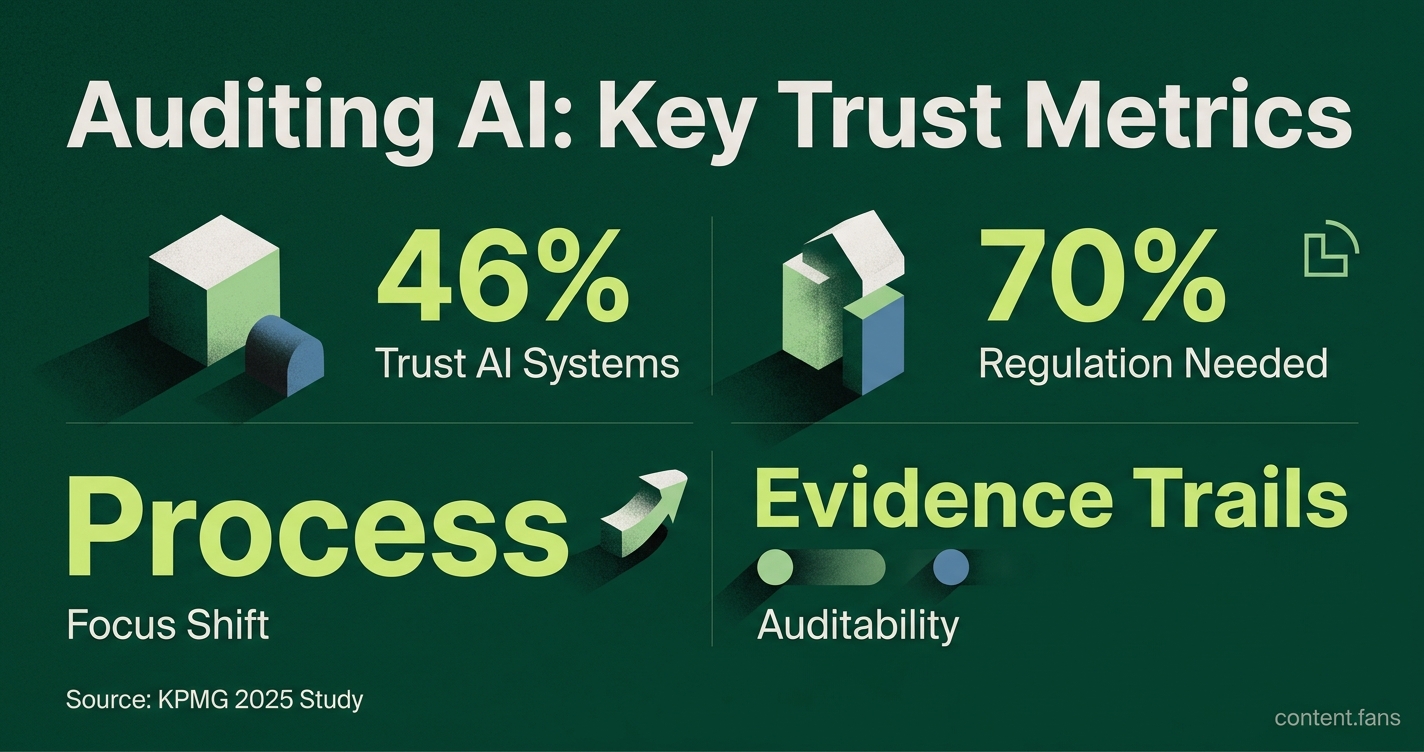

A new report suggests that public trust in AI remains low, with only about 46% of people willing to trust AI and 70% believing regulation is needed. Risk-based governance frameworks, like the NIST AI RMF and the EU AI Act, may help by requiring ongoing monitoring and human oversight for high-risk AI systems. Evidence shows that people want proof of how AI decisions are made, not just promises, so documentation and audit trails are becoming more important. In finance, regulators now focus on tracking data, decisions, and human approvals, which might become common in other high-risk areas. Experts suggest that organizations aligning with these practices and maintaining clear records may have an advantage as rules become stricter in 2026.

As financial regulators audit AI decisions with greater rigor, a public trust deficit persists. KPMG's 2025 global study says 46% are willing to trust AI systems and 70% believe regulation is needed. Consequently, adoption in high-stakes settings is stalling as institutions struggle to verify how AI systems arrive at their decisions. This report details how verifiability, governance frameworks, and new rules are converging to build that trust.

How Risk-Based Governance Addresses the AI Trust Deficit

A growing approach to AI regulation is risk-based tiering. Frameworks like the voluntary NIST AI RMF emphasize continuous monitoring over one-time certification. Simultaneously, the binding EU AI Act mandates strict conformity assessments, technical documentation, and human oversight for high-risk systems used in finance, employment, and law enforcement.

Financial regulators are shifting focus from outcomes to process. To audit AI decisions, they now require verifiable evidence trails that document data inputs, model versions, and human approvals. This process-centric supervision allows auditors to reconstruct incidents and confirm that internal controls operate as designed.

Trust Hinges on Evidence, Not Promises

Public concern centers on opaque AI processes rather than raw capability. The OECD cites weak guidance and legacy IT as key barriers to AI project success in government. As a result, a complete evidence trail - documenting data origin, model versioning, human oversight, and performance tests - is becoming a prerequisite for public trust and a social license to operate.

Finance Leads the Way in Verifiable AI

The financial sector provides a clear model for verifiable AI. Instead of merely judging outputs, supervisors now inspect the entire decision-making process. Industry reports suggest that emerging regulations require detailed logging. A compliant audit stack typically records:

- which data entered the model

- which model or prompt produced the decision

- who approved or overrode the action

- how the result performed over time

Regulators use these artifacts to reconstruct incidents, setting a precedent that may soon apply to other high-risk industries.

What Organizations Can Do to Prepare

To prepare, organizations should proactively align internal policies with frameworks like the NIST AI RMF and ISO 42001. Key steps include classifying AI applications by impact and enforcing human checkpoints for high-risk decisions. Industry observers suggest that institutions able to demonstrate continuous measurement, clear documentation, and transparent oversight will gain a significant adoption advantage as formal rules continue to develop.

How are regulators currently defining "auditability" for AI in finance?

Regulators now equate auditability with end-to-end evidence trails: every data point, model version, prompt, and human override that feeds into an AI decision must be retrievable and reproducible.

- Many financial institutions are being asked to disclose what data informed each AI lending decision and how performance was validated.

- FINRA recommends ongoing monitoring of prompts, responses, and outputs, storing logs for accountability, tracking model versions, and using validation plus human-in-the-loop review where appropriate for GenAI and agentic AI use cases.

- Regulatory frameworks are establishing control objectives that revolve around decision-path auditability, cross-system logging, and vendor transparency.

In short, you must be able to answer four questions at any moment: What happened? Why did it happen? Who approved it? Can we prove it later?

Which governance frameworks are regulators using to classify AI risk?

Risk-based governance is the norm. The dominant references are:

| Framework | Core approach | Why it matters for finance |

|---|---|---|

| NIST AI RMF 1.0 | Govern, Map, Measure, Manage four-function cycle | U.S. baseline; used by banks to run continuous risk assessment instead of one-time compliance gates |

| EU AI Act | Risk-tiered model (prohibited → high-risk → limited) | Lending, insurance, credit scoring are all high-risk; firms must show conformity assessments, human oversight, and public registration before deployment |

| ISO/IEC 42001 | AI management system standard | Operationalises governance; used by internal audit teams to prove repeatability to supervisors |

Together, these frameworks create a de-facto hierarchy: the higher the potential consumer impact, the stricter the evidence and oversight you must provide.

What concrete technical records do auditors request on-site?

Supervisors currently test system behaviour, not just high-level policy statements. Expect to present:

- Training-data provenance: dataset origin, licences, preprocessing steps

- Prompt-output logs: every user prompt, system message, and model response

- Model lineage: architecture, weights, tuning changes, approval history

- Decision-path trace: rule engines, thresholds, overrides, and human sign-offs

- Validation artefacts: bias tests, drift monitoring results, adverse-impact analyses

- Third-party artefacts: vendor contracts, audit rights, incident triggers

If any of these pieces are missing, regulators treat the model as non-auditable and may halt deployment.

How are regulators addressing trust deficits revealed by recent surveys?

Many global respondents in recent surveys express limited trust in AI. Regulators are responding with transparency mandates:

- Under the EU AI Act, specific transparency duties apply to certain AI-generated or manipulated content, with some obligations effective from 2 August 2025 and additional content-labeling obligations for image/audio/video generation becoming applicable on 2 August 2026.

- Various jurisdictions are considering requirements for developers to provide more information about training datasets to address the "black-box" problem.

- FINRA guidance insists on human-readable explanations before any adverse consumer action is taken.

These moves shift the burden of proof: firms must demonstrate safety and explainability, not just claim performance.

What practical steps should financial firms take to stay compliant?

Build an evidence trail that satisfies both U.S. and EU supervisory expectations today:

- Policy layer: adopt a written AI governance policy aligned to NIST AI RMF and ISO/IEC 42001.

- Risk tiering: classify every AI use-case as minimal, moderate, or high-risk; apply stronger controls for credit, fraud, and trading systems.

- Technical controls:

- Enable immutable logs for prompts, outputs, versions, and approvals

- Implement model registry with change tracking and rollback capacity

- Embed human checkpoints before any AI agent executes transactions - Third-party diligence: obtain audit rights and incident protocols from every AI vendor or foundation-model provider.

- Cross-border mapping: document which systems fall under EU AI Act, California laws, and upcoming U.S. federal guidance, then harmonise evidence collection.

Following this playbook now shortens onboarding time with partners and avoids last-minute remediation as regulations continue to evolve.