Late-Stage Space, Infra Startups Raise $1.2B in Mega Deals

Serge Bulaev

Recent data suggests late-stage startups in space, observability, and infrastructure may be getting more funding, with three companies raising over $1.2 billion in one week. Most of this money appears to be going to firms with proven infrastructure or solid revenue. Reports suggest investors are focusing on companies with steady income and contracts, while risks remain if AI demand slows or there are delays in space hardware. Mega deals might be causing salaries to rise and smaller startups to get acquired, as more money clusters around big, established players.

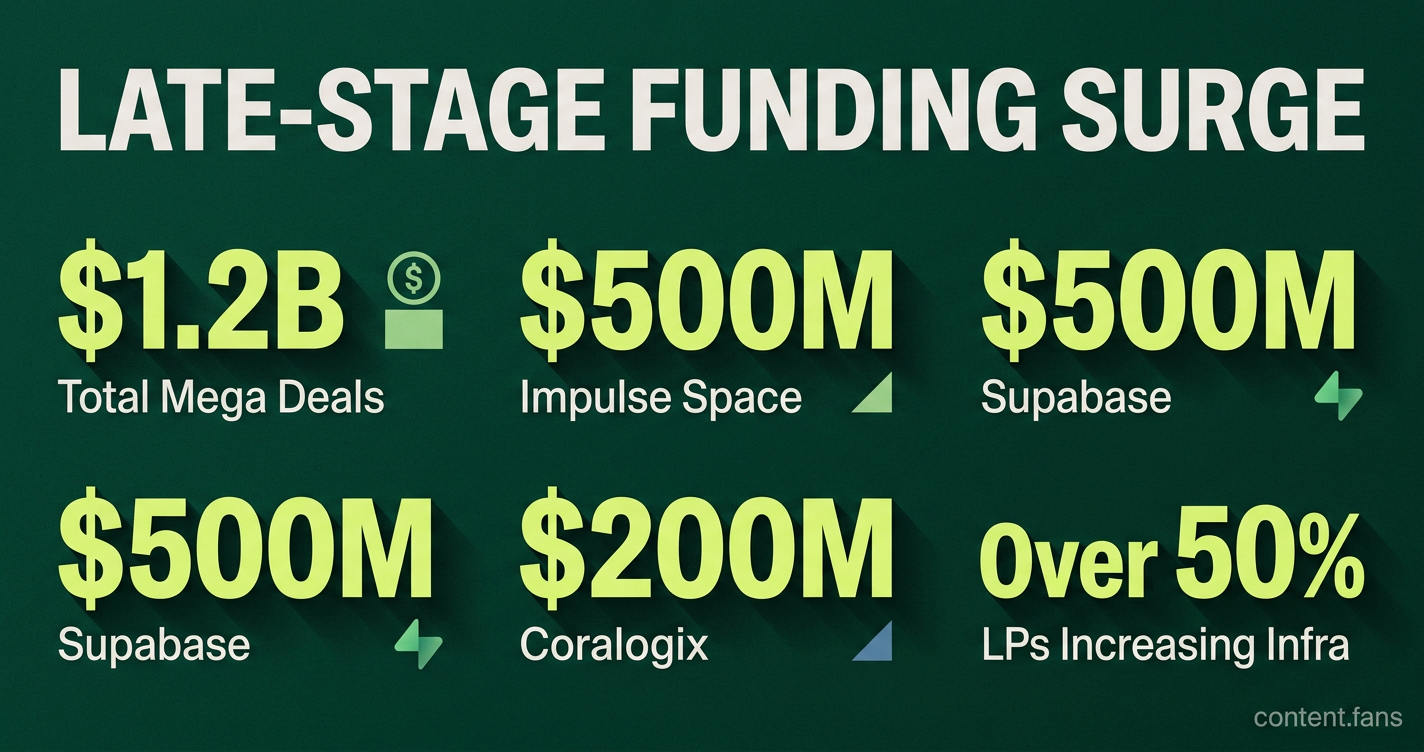

Venture capital is surging into late-stage space and infrastructure startups, with recent data showing three companies raising over $1.2 billion in a single week. This significant concentration of capital, highlighted by mega-deals for Impulse Space ($500M), Supabase ($500M), and Coralogix ($200M), signals a clear investor pivot toward businesses with proven infrastructure and strong revenue density.

Capital is clustering around scaled infrastructure

Investors are prioritizing companies that control essential infrastructure and demonstrate strong, predictable revenue. This shift favors established late-stage firms with significant enterprise or government contracts over more speculative, early-stage technology plays, as they represent a more secure investment in the current economic climate.

Analysis from a February 2026 FundUp.ai report confirms this trend, finding the market "heavy but polarized" where a few Series C+ deals capture the majority of funding. Investor focus has sharpened on metrics like ARR and contracted demand, favoring companies with clear expansion roadmaps and established enterprise or government clients.

The space sector is a key part of this infrastructure focus. Impulse Space's $500M round exemplifies a trend where investors reward operational reliability and contracted launch manifests - criteria similar to those for terrestrial cloud and data-center investments. This follows a quarter marked by strong interest in orbital security, satellite servicing, and defense-related robotics.

Why late-stage checks are getting larger

- Demand for Scarce Resources: The explosion of AI workloads is driving unprecedented demand for compute power and secure data transit. Companies controlling these critical inputs can command higher valuations and justify larger funding rounds.

- Search for Predictable Returns: In a volatile market, investors are shifting toward infrastructure assets for their predictable income streams. A McKinsey survey showed over half of LPs plan to increase infrastructure allocations, seeking the stability that these companies offer.

- An Uncertain IPO Market: The path to a public offering remains unpredictable. As a result, founders are securing large private funding rounds as a form of insurance, ensuring they have the capital to withstand market fluctuations and delay a public listing if necessary.

The scale of these mega-deals is so large that a single transaction can significantly skew quarterly funding data. For instance, Nebius's $4.34B convertible note represented nearly half of all tracked Q2 funding, per Fundz.net. This creates a distorted picture where headline totals appear robust while the median deal size remains stagnant.

Talent and M&A ripple effects

The influx of capital from mega-rounds provides companies with substantial cash reserves to fuel rapid team growth and strategic 'acquihires.' According to Crunchbase commentary, the focus in 2026 technology M&A has shifted to the value of talent and IP over traditional revenue metrics. With IPOs delayed, well-funded companies are opting to acquire niche capabilities instead of developing them in-house.

This trend creates significant ripple effects in the market:

- Rising Salaries: Competition for specialized talent intensifies, driving up salary bands for engineers with expertise in infrastructure, satellite technology, and AI operations.

- Accelerated Consolidation: Smaller startups with limited funding become prime acquisition targets, leading to faster consolidation within key sectors like observability, developer tools, and orbital logistics.

Near-term risk factors

- AI Demand Fluctuation: A potential cooling in the demand for AI infrastructure could lead to significant valuation compression for these highly-funded companies.

- Hardware and Regulatory Hurdles: The space sector remains vulnerable to supply-chain disruptions and regulatory delays, particularly for hardware dependent on government launch schedules.

- Complex Funding Structures: An over-reliance on structured financing or debt-like rounds could create future liquidity pressures and complicate subsequent funding or exit opportunities.

Despite these risks, investors continue to back businesses that demonstrate tangible progress. The ability to show contracted revenue, meet critical milestones, and maintain control over essential infrastructure remains the key to securing capital in this competitive landscape.

How much capital was raised this week, and which companies topped the list?

The digest tracked $1.2 billion across just three deals.

- Impulse Space closed a $500 million late-stage round, underscoring investor confidence in orbital logistics and last-mile delivery for satellites.

- Supabase, the open-source Firebase alternative, matched the $500 million figure as late-stage capital floods developer-data infrastructure.

- Coralogix secured $200 million, adding another data-heavy, revenue-rich observability platform to the quarter's record tally.

Why are late-stage investors suddenly favoring space and infra over pure software?

Current reporting shows a capital rotation toward scarce, revenue-heavy inputs rather than speculative growth.

Key filters now include annual recurring revenue, government or enterprise contracts, and measurable production capacity.

Space companies need orbital security credentials and demonstrated scale, while infra software must show recurring integration value.

The result is a more selective but larger-check environment where infrastructure controls the scarce layer and earns the premium.

What risks come with these mega-round concentrations?

- Winner-take-most pressure: only a handful of companies now carry outsized balance sheets, widening the gap between funded leaders and the rest.

- Valuation overhang: if public-market appetite softens, late-stage marks could face sharp re-pricing.

- IPO window fragility: with exits delayed, investors must rely on secondary liquidity or M&A; any delay multiplies carry risk for LPs.

How might these rounds reshape hiring and M&A activity?

- Talent as an acquisition asset: 2026 M&A data shows buyers paying more for engineers and proprietary IP than for pure revenue multiples.

- Acquihire momentum: well-funded players like Impulse and Supabase can buy teams outright rather than compete on salary alone.

- Consolidation wave: late-stage cash plus scarce talent is accelerating bundling plays in AI, security, and space segments.

Crunchbase predicts a 15 % uptick in tech M&A volume as startups facing down rounds opt for strategic sales instead.

Where can I track the next wave of mega-rounds?

- CBRE's Infrastructure Quarterly provides recurring snapshots of AI data-center and power deals.

- Qubit Capital's weekly funding roundups consistently surface the next Series C+ infrastructure and space names.