JPMorgan raises $7B for OpenAI data center, financing AI infrastructure boom

Serge Bulaev

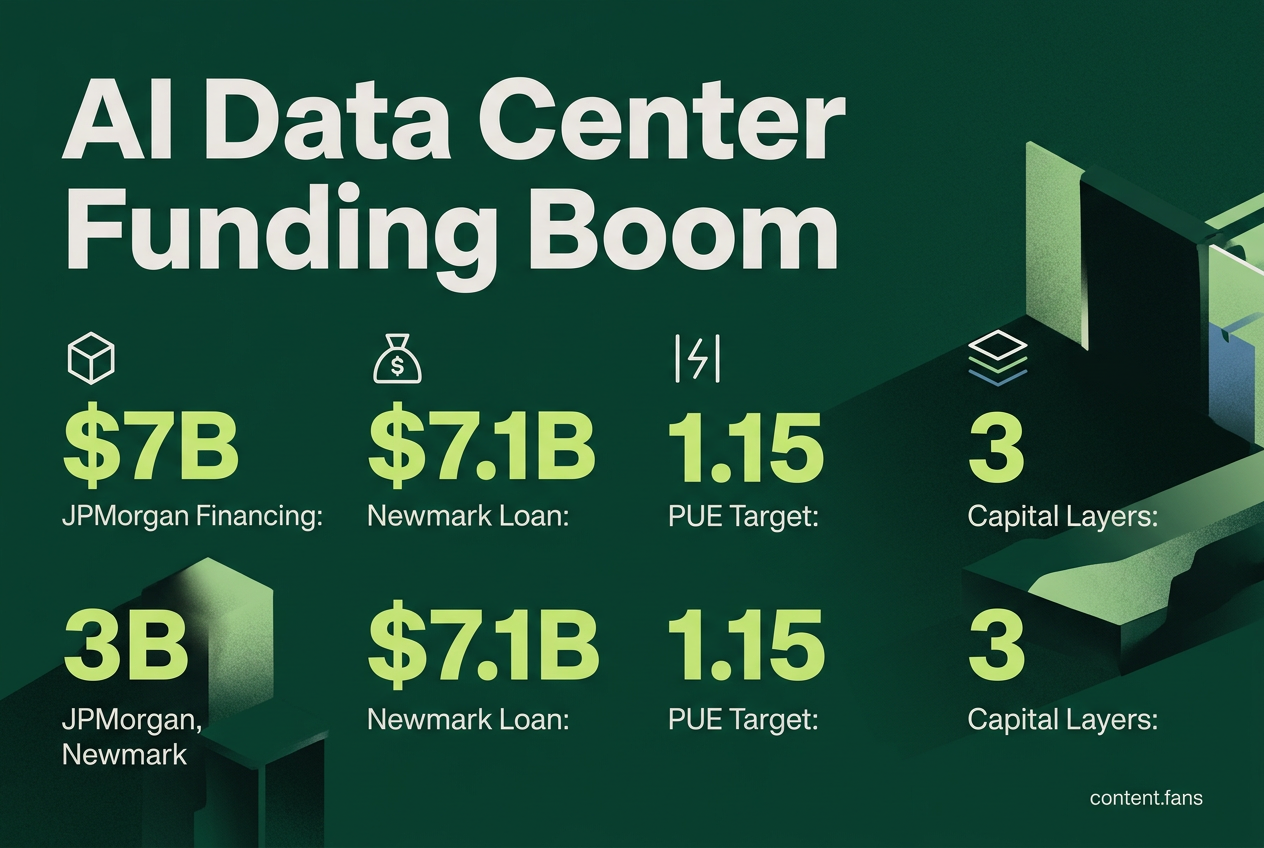

JPMorgan has raised over $7 billion to finance a new AI data center in Texas, connected to OpenAI's Stargate project. Another firm, Newmark, also arranged a $7.1 billion loan for a nearby large AI data center. These deals suggest banks are starting to view large AI data centers as important infrastructure. Lenders may require strict rules about cooling systems, power use, and equipment contracts. There might be challenges for lenders to sell some parts of these loans, showing the importance of strong agreements and careful planning.

JPMorgan's massive financing for an OpenAI data center in Texas signals a new era for the AI infrastructure boom. The deal, tied to OpenAI's Stargate program via an Oracle-leased campus, shows banks are now treating these large-scale facilities as essential infrastructure, not just enterprise IT, according to reports The Information. This follows a previous substantial construction loan, illustrating the enormous capital required to power the AI revolution.

This trend is further solidified by another landmark transaction: a major construction loan for a large-scale AI data center, also in Texas, arranged by Newmark's capital-markets team Newmark press release. The deal underscores the growing importance of specialized expertise, with Newmark having recruited top talent to secure such hyperscale projects PR Newswire.

These two financings provide a clear blueprint for structuring future AI-scale campus developments.

Building and Financing Data Centers for AI Workloads: Capital Stack

These multi-billion-dollar projects rely on a layered capital stack. A combination of senior construction debt from large banks, mezzanine loans from specialized funds, and significant equity from both sponsors and the hyperscale tenants themselves provides the necessary funding and distributes risk among the involved parties.

- Senior Construction Debt: Typically syndicated among major banks, covering a significant portion of the total cost.

- Mezzanine/Holdco Loans: Provided by infrastructure debt funds to fill a substantial gap in the capital stack.

- Sponsor and Tenant Equity: The remaining balance is covered by the developer's equity, often with co-investment from the hyperscale tenants.

In the JPMorgan deal, the single-tenant nature of the lease created syndication challenges, increasing perceived risk. To mitigate this, lenders required stringent covenants, including detailed power-purchase agreements (PPAs), step-in rights on GPU supply contracts, and limits on rack power density until advanced liquid-cooling systems are fully operational.

Tenant and Vendor Contracts

Long-term contracts are crucial for de-risking these investments. The Oracle lease, for instance, extends beyond the debt term, securing future cash flows and reducing refinancing risk. Similarly, projects are adopting "design-build-transfer" models where contractors must meet strict efficiency targets, like a 1.15 Power Usage Effectiveness (PUE), before handover. Both deals lock in multi-year supply agreements for critical equipment to prevent project delays.

Operations: Power, Cooling, Interconnect

Operationally, these AI data centers push the limits of power and cooling. Modern GPU racks consume significantly more power, dwarfing the capacity of older air-cooled facilities. Consequently, according to industry reports, projects are implementing direct-to-chip liquid cooling for high-density racks and planning for immersion cooling for future higher densities. The network architecture is similarly zoned, with high-performance fabrics for training clusters and separate networks for less intensive tasks.

Risk Management and Lender Checklist

Lenders are implementing a rigorous due diligence checklist to manage the unique risks of AI data centers:

- Power Agreements: Verifying long-term power-purchase contracts and access to dual-feed substations.

- Efficiency Testing: Stress-testing the facility's Power Usage Effectiveness (PUE) under various scenarios.

- Hardware Commitments: Confirming tenant obligations to purchase future GPU generations.

- Exit Strategy: Modeling exit capitalization rates with conservative assumptions, including significant vacancy scenarios after debt maturity.

- Operational Reporting: Requiring quarterly reports on critical metrics like water usage and coolant leak incidents.

Financial templates now include detailed technical covenants. Standard term sheets specify cure periods for cooling system failures and include "density step-down" clauses, which compel tenants to reduce computational load if temperatures exceed predefined safety thresholds.

Talent Flows and Market Signaling

The high-stakes nature of these deals is also reshaping the job market. The demand for bankers who grasp both complex financial covenants and the technical specifics of AI data center cooling is surging. The success of specialized teams, like Newmark's, in securing multiple multi-billion-dollar deals suggests that advisory expertise is shifting from traditional data-center REITs to diversified financial services firms.

With facilities targeting completion in the coming years, the market is watching closely. Despite the momentum, lenders face challenges syndicating such large, concentrated debt positions. This reinforces the critical importance of a diversified capital stack and strict operational covenants to successfully finance the next wave of AI infrastructure.

What exactly is the JPMorgan loan financing in the OpenAI data center?

The facility is an Oracle-leased campus in Texas that is part of the broader Stargate project. It is designed to house a substantial number of NVIDIA chips and target significant IT load capacity, making it one of the largest single-site AI training clusters ever financed. The loan is arranged on a project-finance basis, with debt secured by the long-term Oracle lease and the physical asset itself. JPMorgan previously supplied a substantial construction loan; the new financing completes the capital stack for the build-out expected to energize in the coming years.

How is risk distributed among lenders, tenants, and infrastructure partners?

Lenders are protected by a dual-cash-flow structure: the Oracle master lease provides primary repayment, while Crusoe, Blue Owl, and Primary Digital Infrastructure hold the developer equity and serve as the first-loss cushion. Concentration risk is mitigated through conservative loan-to-cost caps and step-down pricing grids if occupancy rates fall below target levels. Tenants (OpenAI via Oracle) enter a long-term triple-net lease with CPI-linked escalators and step-in rights for the bank in a default scenario - a structure that has become the template for most AI-scale sale-leaseback deals circulated in the market.

Which financing structures are emerging as the standard for AI data centers?

Because power-hungry GPU clusters can significantly increase the per-rack energy draw versus legacy servers, sponsors are favoring three structures:

- Project finance loans for green-field campuses with substantial power potential, using long-term hyperscaler leases as collateral.

- Corporate revolvers secured by a pledge of data-center assets, allowing developers to layer multiple smaller acquisitions.

- Private infrastructure funds (think DigitalBridge, Blackstone BIP) injecting equity in exchange for preferred yields backed by sale-leaseback agreements once the campus is energized.

According to industry reports, a growing portion of new AI data-center debt now follows one of these three templates.

What operational thresholds force the switch from air to liquid cooling?

Practical tipping points observed in live sites:

- Lower power densities - standard hot-aisle containment can still cope.

- Medium densities - hybrid arrangements (rear-door heat exchangers + liquid-assisted cold plates).

- Higher densities - direct-to-chip liquid cooling becomes mandatory; air is relegated to switchgear and storage arrays.

- Very high densities - two-phase immersion starts to pencil out once GPU generations exceed substantial wattage per card.

In data center builds, designers are increasingly scoping DLC loops sized for high power densities from day one, recognizing that future GPU generations are expected to require significantly more power.

Are talent moves signaling a broader market trend?

Industry talent shifts are part of a visible "infrastructure banker carousel". Data-center advisory revenues industry-wide have climbed substantially, and top rain-makers are being offered equity upside deals to change firms. Many teams that have arranged major loans have since seen senior directors move to infrastructure funds, underlining how human capital is becoming as scarce as suitable power sites. The takeaway for capital-seeking developers: lock in your banking syndicate early, because the next deal may not staff itself.