Intel Expands Foundry Roadmap as Companies Seek Backup Chipmakers

Serge Bulaev

Companies are looking for backup chipmakers like Intel because recent shortages and global tensions have shown that relying on one factory can be risky. Most advanced chip factories are in East Asia, and any problems there might cause big delays and losses for electronics makers. Government programs such as the U.S. CHIPS Act are making it easier and cheaper for companies to use more than one chip supplier. Intel is working on new chip technology and packaging, and some experts believe its U.S. factories may help shorten wait times for new designs. Many companies may use Intel as a backup supplier to make sure they have enough chips, even if it is not always the fastest or most advanced option.

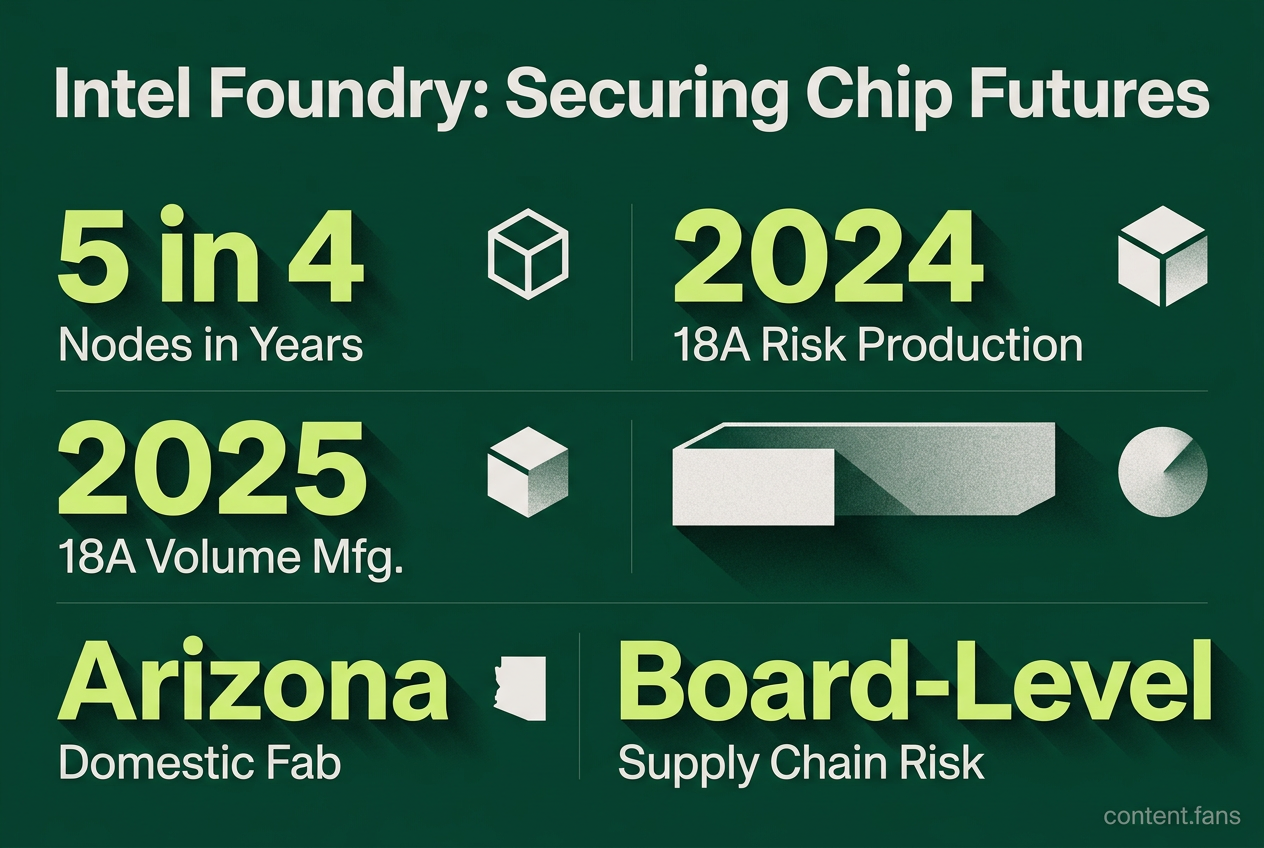

Recent semiconductor shortages and geopolitical tensions have elevated supply-chain risk analysis to a board-level imperative, prompting companies to seek backup chipmakers like Intel. Dependence on a single foundry has proven capable of stalling billion-dollar product lines. This analysis examines the core risks driving this diversification and how Intel's expanded foundry roadmap offers a strategic solution for business continuity.

Rising Demand and Geopolitical Exposure

The world's advanced logic production is heavily concentrated in East Asia, creating significant supply chain vulnerabilities. According to industry reports, there is a growing need for improved resilience and geographic diversification in semiconductor manufacturing. Experts warn that a disruption in the Taiwan Strait could eliminate a substantial portion of leading-edge capacity, impacting the server, networking, and automotive industries. Industry analyses suggest that such an interruption could cost global electronics firms billions in lost revenue.

Companies are diversifying their semiconductor manufacturing partners to mitigate significant financial and operational risks. Heavy reliance on single, geographically concentrated foundries has exposed them to disruptions from shortages and geopolitical instability. Using backup suppliers like Intel ensures production continuity, enhances negotiating leverage, and secures capacity buffers.

Government Incentives Accelerate Diversification

Government initiatives are a key catalyst for supply chain diversification. Landmark legislation like the U.S. CHIPS Act, along with similar programs in Europe and Japan, significantly reduces the capital expenditure for building domestic fabs. These incentives make second-source agreements more financially viable, transforming multi-sourcing from a premium strategy into a mainstream risk-management practice.

Intel's Foundry Roadmap and Systems-Foundry Model

Intel has aggressively re-entered the contract manufacturing market, detailing an ambitious Intel Foundry roadmap in February 2024 that maintains its "5 nodes in 4 years" objective. Key milestones on this path include:

- Intel 18A: Risk production in 2024, with volume manufacturing targeted for 2025.

- Intel 14A: Early customer engagement is underway, featuring a power delivery upgrade called PowerDirect.

- Advanced Packaging: A comprehensive menu including EMIB-T, Foveros-R, and FCBGA 2D+ is integrated into a single workflow.

Intel confirms that initial 18A test wafers are running at its Fab 52 in Arizona, providing a crucial domestic manufacturing option. Furthermore, Intel's "systems foundry" approach, which integrates wafer fabrication with advanced packaging and testing, is expected to shorten qualification cycles for complex, multi-chiplet designs.

Key Considerations for Evaluating Intel as a Backup Supplier

Until its 14A process matures, Intel's 18A node may lag competitors in transistor density but aims to deliver competitive power and performance via RibbonFET and backside power. Procurement teams must weigh this marginal performance gap against the critical benefit of supply availability during shortages.

Vendor risk assessments now prioritize geographic dispersion, financial stability, and policy alignment. Intel's U.S. manufacturing footprint, combined with strategic alliances, earns high marks on diversification metrics, though customers must perform due diligence on the readiness of each new process node.

A Strategic Playbook for Dual-Sourcing

To effectively secure supply chains, enterprises can adopt the following framework. This helps ensure business continuity without overcommitting to speculative technologies.

- Map component criticality against foundry concentration to spot single points of failure.

- Assign weighted risk scores that combine geopolitical exposure, node maturity, and financial health.

- Structure contracts with escape clauses tied to specific process-node milestones rather than dates.

- Align engineering roadmaps so substrates, packaging, and firmware tolerate cross-foundry variation.

By treating Intel as a qualified backup rather than a full replacement, buyers can balance near-term resilience with long-term performance goals.

What is driving Google, Nvidia and others to treat Intel as a potential backup chipmaker?

Capacity crunch, price leverage and geopolitical tension are the immediate triggers. Taiwan is still the dominant location for leading-edge semiconductor manufacturing, with sources citing about 68% of leading-edge capacity or over 90% of the most advanced chips, depending on the definition used, creating a single-point-of-failure scenario that procurement teams can no longer ignore. At the same time, post-shortage pricing power remains with the dominant foundry, so adding Intel gives buyers negotiating leverage and visible capacity buffers for future demand spikes.

How does Intel's roadmap compare with leading-edge alternatives?

Intel is moving from Intel 18A (risk production in 2024) to Intel 14A (early customer engagement now) and wraps both nodes into a systems-foundry package that includes 2.5D/3D advanced packaging, Foveros Direct bonding and EMIB interconnects. While 18A delivers RibbonFET + PowerVia - Intel's answer to TSMC's N3 family - the real differentiator is the domestic U.S. footprint: volume wafers start in Oregon and ramp in Arizona's Fab 52, giving customers a non-Asia leading-edge option for the first time in a decade.

What concrete procurement safeguards should be written into an Intel backup contract?

Treat the deal as a risk-scored service, not just capacity. Leading supply-chain teams are insisting on:

- Dual-sourcing clauses that reserve an agreed Intel wafer start volume without exclusivity, preserving fallback rights to other foundries

- Technology roadmap parity guarantees - contract language that Intel will maintain process parity (within one node) with its primary competitor for the life of the part

- Geographic resilience addendum - right to shift final assembly/test to Intel's U.S. or European ASAT lines if Asia logistics are disrupted

- Liability caps tied to geopolitical force majeure events, lowering exposure if export controls or sanctions intervene

How will multi-sourcing affect die cost and time-to-market?

Expect a cost uplift versus single-source pricing, but the hidden value is lead-time compression. By pre-qualifying Intel wafers in parallel with the primary source, companies have reduced risk mitigation inventory significantly, freeing working capital. Early adopters report faster product ramps when Intel's Arizona line is used for initial lots instead of air-freighting from Taiwan.

Which geopolitical triggers should procurement teams monitor?

Watch three risk vectors:

- Export-control escalations between the U.S. and China that could restrict EDA tools or EUV spare parts to any single foundry

- Taiwan Strait incident probability tracked by insurers - elevated risk readings typically trigger automatic dual-source activation clauses

- CHIPS Act disbursement schedules - Intel's capacity expansion subsidies are milestone-based; slipping timelines would delay Arizona ramp and push backup volumes back to Asia