Hyperscalers Raise 2026 AI Infrastructure Spending to $690 Billion

Serge Bulaev

Hyperscalers may spend up to $690 billion on AI infrastructure in 2026, which is about twice as much as in 2025. There appears to be a shortage of computers and chips as AI demand rises, so companies are raising prices and changing how they charge for access. Analysts suggest the advantage now lies in having and managing limited computing resources, not just building bigger AI models. Constraints like GPU supply, power, and cooling seem to make it hard to meet all demand, so companies may limit access or charge more for premium features. Enterprises might need to adjust their budgets and contracts to deal with rising and changing costs.

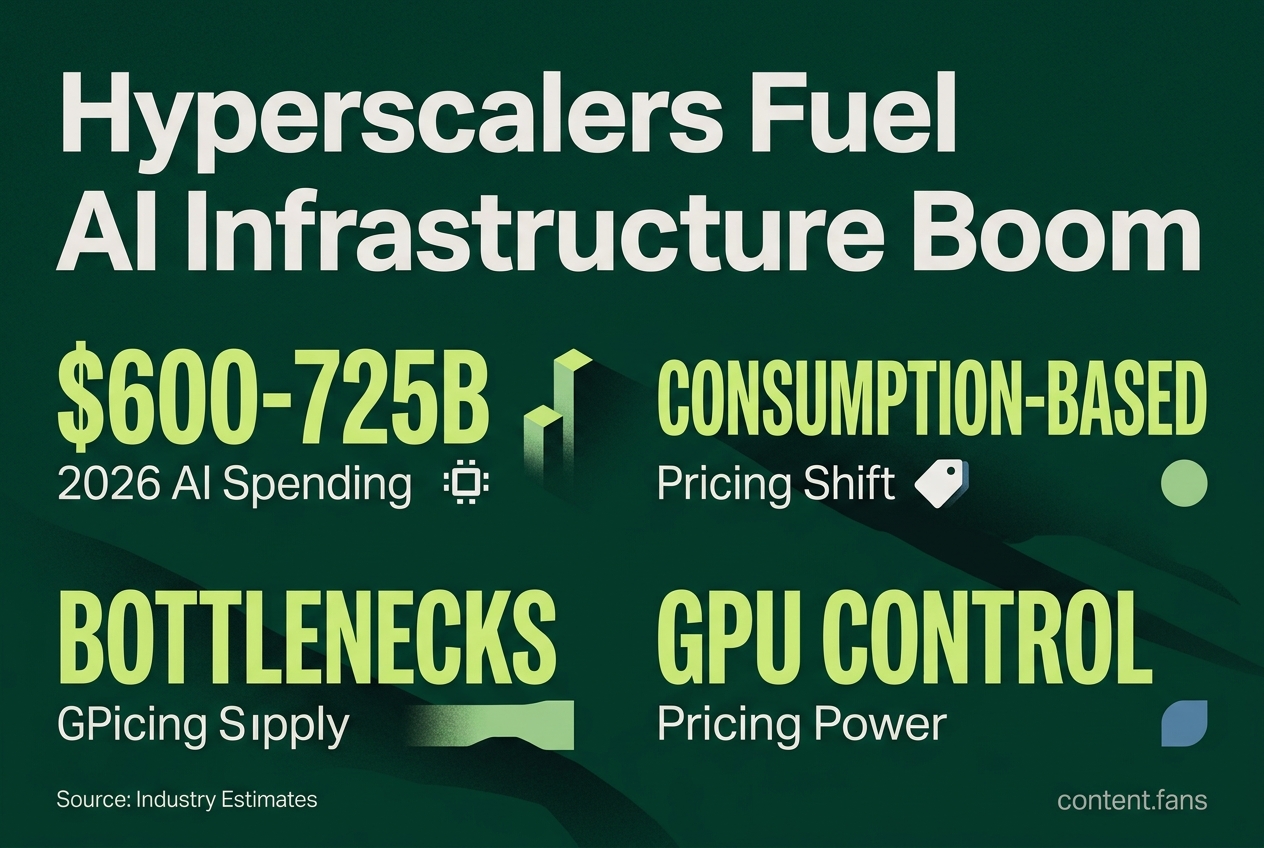

In a landmark move, hyperscalers are substantially increasing their 2026 AI infrastructure spending, with industry estimates suggesting investments in the range of $600-725 billion, signaling a strategic shift driven by rising compute scarcity and skyrocketing AI demand. This investment surge is reshaping pricing and infrastructure strategies as providers grapple with steepening demand curves from autonomous agents while facing persistent bottlenecks in GPU supply, power, and cooling. The competitive edge is no longer about building larger models, but about securing and monetizing limited compute resources.

Pricing drifts toward capacity awareness

Hyperscalers are projected to make substantial infrastructure investments in 2026, with industry estimates suggesting a significant increase over previous years. This capital is primarily directed at acquiring AI-specific hardware, including GPUs, and expanding data center capacity to meet the unprecedented demand for AI services and inference.

The era of flat-rate AI subscriptions is ending. As providers confront capacity limits, they are shifting to consumption-based models. A recent Albert Masoliver analysis notes that by spring 2026, major labs had already increased token prices, cut inclusive allowances, and throttled legacy plans, with inference costs rising "across the board."

Key changes in market pricing include:

- Increased per-token fees for frontier models, particularly for computationally intensive output tokens.

- Introduction of priority tiers allowing users to pay for premium access during peak utilization.

- Discontinuation of unlimited plans in favor of contracts that penalize heavy usage.

- Segmented access models reserving the fastest or most capable modes for premium contracts.

JPMorgan Asset Management confirms this trend, stating that pricing power is shifting to entities controlling scarce GPU supply. This forces enterprises to forecast total consumption costs instead of relying on simple headline rates.

Capital expenditure races ahead of supply

In response, hyperscalers have announced record capital expenditures. Industry reports project substantial combined capex from Amazon, Microsoft, Alphabet, Meta, and Oracle - representing a significant increase over their 2025 spending. A substantial portion of this is dedicated to AI infrastructure. According to various industry reports, individual commitments are staggering, with Amazon planning substantial investments and other major players significantly increasing their spending.

Industry estimates suggest major hyperscalers are planning substantial capex increases for 2026, with Amazon leading investments and other major players including Alphabet, Microsoft, and Meta planning significant outlays. These figures underscore how AI infrastructure has become a primary balance-sheet item, financed in part by substantial bond issuances.

Multi-layer bottlenecks complicate scale

Scaling AI capacity is complicated by bottlenecks beyond just chip supply. Inference is projected to consume a substantial portion of all AI compute this year, intensifying pressure on the entire stack. Critical constraints now include power grid access, data center cooling, HBM memory availability, and sold-out advanced semiconductor fabrication lines at manufacturers like TSMC. Experts from CNAS now consider chip production itself a primary binding constraint.

Strategic implications for buyers

For enterprise buyers, this new landscape demands a more sophisticated procurement strategy. Procurement teams now evaluate:

- Effective cost under real agent workloads, including retries and tool calls.

- Contractual rights to burst capacity during product launches or seasonal peaks.

- Trade-offs between frontier reasoning quality and cheaper commodity inference.

As analyst Masoliver argues, while metered billing aligns provider revenue with compute costs, it shifts budget volatility to the customer. To mitigate this risk, enterprises are increasingly seeking reserved capacity blocks or minimum commitment contracts. Meanwhile, large incumbents are locking in supply through multi-year GPU deals and direct investments in chip makers, leaving smaller players to navigate a volatile market where price and access are unpredictable.

How much are hyperscalers actually spending on AI infrastructure in 2026?

They are on track to invest substantial amounts in capital expenditures for the year, with industry estimates ranging from $600-690 billion in 2026 for the largest hyperscalers, up from estimates of around $380-465 billion in 2025. A significant portion of that total is estimated to be directed to AI infrastructure, with roughly $450 billion earmarked for AI-specific hardware and data centers. Amazon is estimated around $200 billion, while Alphabet and Meta are often projected above $100 billion, with Microsoft estimates varying across different sources.

Why is compute capacity suddenly treated as a strategic scarce resource?

Agentic workflows and frontier models now require significantly more inference per user session than traditional chat-style interactions. With inference consuming a substantial portion of all AI compute, the slightest supply shortfall becomes a market-moving choke point. Analysts at J.P. Morgan note that "compute is being locked in multi-year blocks", giving firms that control capacity immediate pricing and competitive leverage.

How is compute scarcity changing pricing for frontier AI services?

Providers are rapidly moving away from flat-rate plans. Expect the following shifts:

- Per-token pricing has become the default and rates for frontier output tokens have risen sharply.

- Priority tiers let customers pay extra for faster queues or reserved capacity.

- Unlimited plans are being phased out, replaced by usage-based contracts with steep overage fees.

Industry analysis indicates that traditional flat-rate arrangements are becoming increasingly unsustainable. The AI Pricing Shift to Consumption-Based Platforms

Which bottlenecks are limiting AI capacity besides raw compute?

Multiple layers of the stack are now constraints:

- Power and cooling - grid interconnection delays can halt deployment faster than chip shortages.

- Memory and networking - HBM supply and optical interconnect capacity are facing significant constraints according to industry reports.

- Semiconductor fabrication - TSMC's leading-edge nodes are at maximum allocation, creating downstream shortages for both GPUs and custom ASICs.

Industry reports indicate that AI chip production represents a significant constraint on the pace of AI compute buildout.

Who wins and who loses in the 2026 infrastructure sprint?

Winners: Large incumbents with balance-sheet strength (Amazon, Microsoft, Alphabet) and their key suppliers (Nvidia, AMD) that can secure multi-year capacity contracts and finance gigawatt-scale data centers.

At risk: Smaller AI start-ups, regional telcos and any service that still relies on overflow cloud credits or spot-GPU pricing. Without locked-in capacity, they face higher latency, hard limits on concurrent users, and pricing volatility whenever demand spikes.