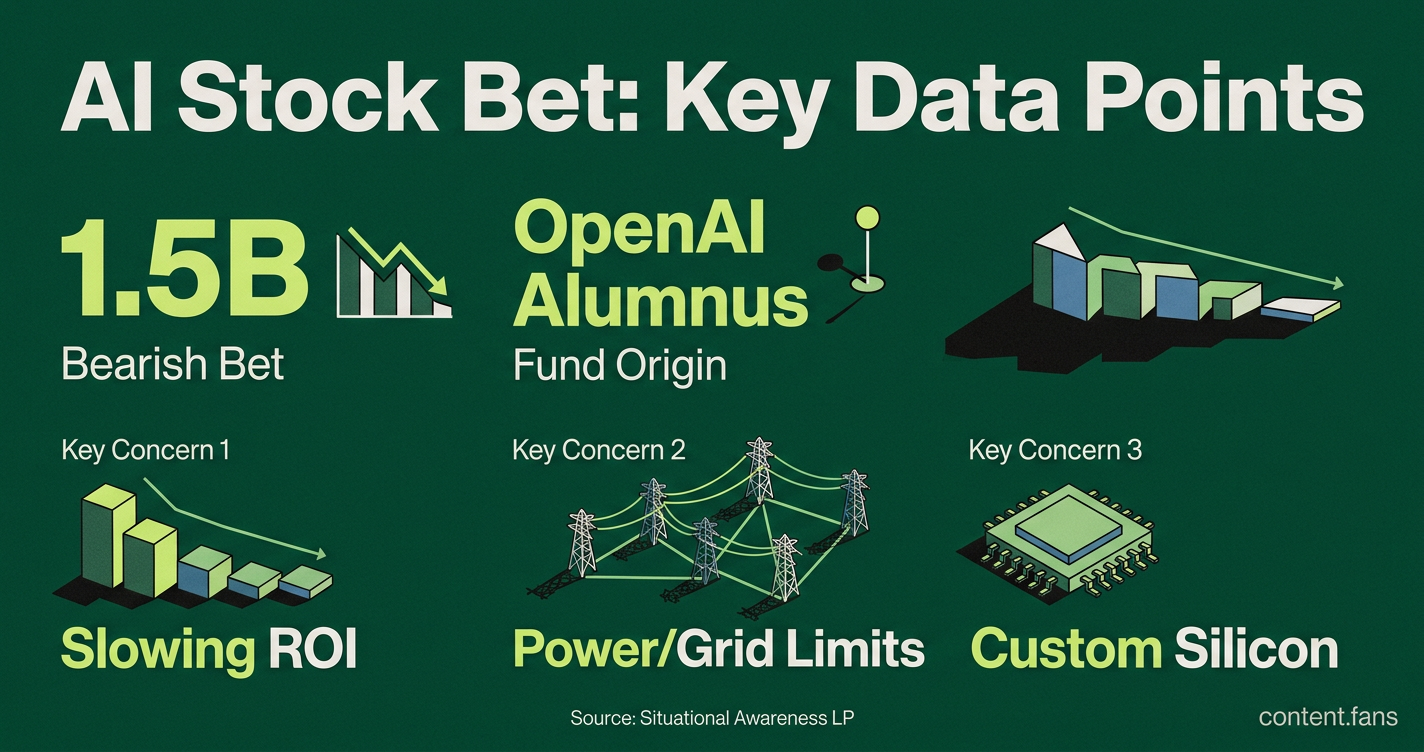

Hedge fund places $1.5B bearish bet against Nvidia, other AI stocks

Serge Bulaev

Situational Awareness, a hedge fund started by a former OpenAI researcher, has reportedly placed over $1.5 billion in bets against Nvidia and other AI-related companies. This move is unusual because most analysts still have a positive view on the future of AI infrastructure. The hedge fund's strategy may be based on concerns that more efficient AI models, slower returns on investment, and possible power or supply issues could hurt these companies. The fund's bets do not predict an end to AI growth but suggest there might be slower growth or setbacks that could affect stock prices. This approach appears to challenge the current strong optimism in the AI sector.

Situational Awareness, a hedge fund from former OpenAI researcher Leopold Aschenbrenner, has reportedly placed a significant bearish bet against Nvidia and other major AI stocks, including Oracle, AMD, and TSMC. This substantial wager stands out as a notable challenge to the market's largely constructive outlook on AI, a view recently detailed by the BlackRock Investment Institute.

As one of the larger institutional challenges to the consensus AI trade, the move warrants a closer look. This analysis examines the facts behind the bet, the founder's unique background, and the market crosscurrents informing the fund's contrarian position.

Why Hedge Fund 'Situational Awareness' Takes Large Bearish Bets Against AI Infrastructure

The fund, led by an OpenAI alumnus, is wagering against AI leaders like Nvidia due to concerns over slowing returns on investment. This bearish stance cites risks such as increasingly efficient AI models reducing compute demand and a widening gap between massive infrastructure spending and actual revenue generation.

Founder Leopold Aschenbrenner joined OpenAI's Superalignment team in 2023, co-authoring the paper "Weak to Strong Generalization" before departing in April 2024 to launch Situational Awareness LP. His research background provides a unique perspective on model efficiency trends that could curb future compute demand - a risk that analysts at CMC Markets believe could trigger a correction.

Further fueling this bearish thesis is a significant mismatch between spending and monetization. Industry reports highlight that hyperscalers have committed substantial capex investments, while enterprise AI has generated considerably less revenue. This gap suggests slower returns for chipmakers, setting the stage for potential investor disappointment.

Market enthusiasm meets rising headwinds

While many Wall Street forecasts project substantial AI infrastructure investment by 2030, emerging headwinds temper this enthusiasm. Fidelity notes that AI drives a significant portion of recent economic growth but also warns that "power is the feedstock for AI," pointing to rising costs and physical constraints. Key concerns include:

- Power and grid constraints that could delay data-center projects, reducing the near-term need for GPUs.

- The rise of custom silicon from cloud providers like Amazon and Alphabet threatens to erode Nvidia's pricing power.

- Debt-funded capex at some suppliers which may pressure earnings if interest rates remain elevated.

StoneX reports that soaring capital expenditures are already testing investor confidence despite solid earnings. Concurrently, Goldman Sachs warns that any slowdown in hyperscaler capex growth could trigger a rapid compression of valuations across the entire semiconductor supply chain.

How Aschenbrenner's thesis contrasts with consensus

While consensus outlooks from BlackRock and Fidelity still favor core suppliers like TSMC, and a Yahoo Finance roundup underscores Nvidia's market dominance, Situational Awareness is betting that this optimism overlooks several key downside catalysts:

- Rapid efficiency gains in AI models could reduce incremental compute demand faster than markets anticipate.

- Margins may shrink as competition from in-house chips from major cloud providers intensifies.

- Power shortages or regulatory hurdles could stretch deployment timelines and delay revenue.

- Valuations remain high relative to earnings estimates, leaving little room for error or disappointment.

The fund's strategy does not predict a collapse in AI investment but rather anticipates that even a modest deceleration in spending could trigger a sharp market correction. This targeted hedge is positioned for a scenario where high-flying AI stocks, having rallied far ahead of earnings, undergo a period of repricing as the infrastructure boom matures.

What exactly did Situational Awareness bet against?

According to industry reports, the fund purchased substantial put options against Nvidia and established bearish positions on Oracle, Broadcom, AMD, TSMC, and ASML. These trades are designed to profit if the share prices of these firms decline before the options expire.

Who runs Situational Awareness and why does their background matter?

The fund was founded by Leopold Aschenbrenner, a former researcher on OpenAI's Superalignment team. His background is notable as he co-authored the paper "Weak to Strong Generalization" and, according to his personal site, now focuses on AGI-related investments. That a former AI safety insider is betting against AI infrastructure has amplified the market's attention.

What are the main reasons behind the bearish view?

Current research points to several key catalysts:

- Revenue lag: Enterprise AI pilots convert to cash flow at low rates, while hyperscaler capex has reached substantial levels.

- Margin pressure: Custom chips from Google, Amazon and others threaten Nvidia's pricing power.

- Energy bottlenecks: Data-center electricity demand is forecast to grow significantly, risking project delays and higher operating costs.

- Valuation gap: Industry analysts note that infrastructure stocks have gained substantially while forward earnings estimates have risen more modestly.

- Debt load: Analysts expect significant new corporate bond issuance this year to fund data-center build-outs, raising refinancing risk.

- Concentration risk: A handful of hyperscalers drive the majority of orders; any pause could cascade through the supply chain.

- Efficiency gains: New, more efficient AI models could cut incremental compute demand.

- Capex cliff: Even a modest deceleration in hyperscaler spending could trigger multiple compression.

How does the broader market view AI infrastructure right now?

The prevailing market sentiment remains constructive but is growing more selective, according to recent analysis from BlackRock, Fidelity, and Morningstar. While long-term capex forecasts remain high, investors are increasingly focused on profitability and are beginning to rotate capital from chip designers toward sectors like energy, cooling, and other infrastructure enablers.

Could the bet backfire?

Absolutely. The bearish thesis depends on headwinds materializing. If enterprise adoption accelerates, power constraints are resolved, or demand continues to outstrip supply, the bet could fail. Nvidia still holds over 80% of the data-center accelerator market, and key suppliers like TSMC remain dominant.