EU AI Act, Colorado Law Impact Financial Services Content by 2026

Serge Bulaev

New AI laws in the EU and Colorado may change how banks and insurers use and share AI content by 2026. These rules require companies to tell customers when AI is used, keep records, and check for bias. Many banks already use generative AI and plan to use it more, but they must follow new rules for fairness and privacy. Some experiments, like those at Ally Bank, suggest AI tools could help attract customers, but strict checks and approvals are needed. Firms are updating their workflows to meet these new requirements while trying to keep using AI tools safely.

The EU AI Act and Colorado's new AI law are creating significant impacts for financial services content, with major compliance deadlines approaching. As banks and insurers accelerate their use of AI, they face a new landscape of regulatory oversight focused on transparency, fairness, and documentation. This article outlines five key developments shaping how financial firms must adapt their client communication and content strategies.

Regulatory Pressure: Disclosures, Review, and Documentation

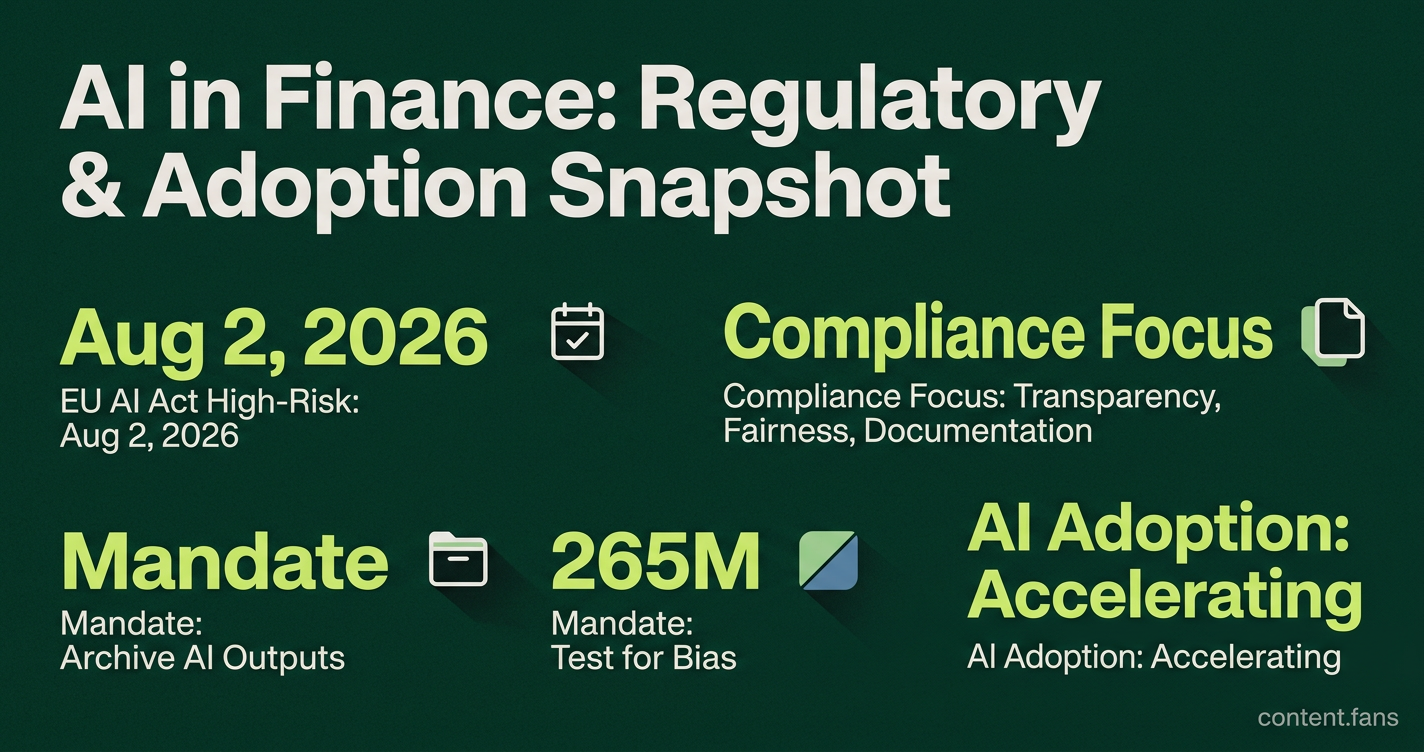

New laws mandate strict compliance for AI-generated content. The EU AI Act imposes high-risk obligations starting 2 August 2026. Colorado's AI law creates disclosure requirements for certain AI-driven decisions. With Utah's AI Policy Act also in effect, firms are now required to archive AI outputs, maintain model inventories, and ensure all AI-assisted content undergoes compliance review.

These laws mandate that financial firms disclose AI use in client communications, maintain detailed records of AI models and their outputs, and rigorously test for bias. Any AI-assisted content, from marketing emails to loan decisions, will require compliance review and a clear audit trail before publication.

Adoption Snapshot: Marketing and Internal Copilots

Despite new regulations, AI adoption is accelerating. Industry reports indicate a significant portion of financial firms already use generative AI, with many more planning to do so within the next few years. High-profile examples, like Morgan Stanley's GPT-4 chatbot and Wells Fargo's "Fargo" assistant, show a clear trend of moving AI tools from pilot programs to large-scale deployment for tasks like document summaries and customer service.

Marketing Experiments: Measurable but Supervised

Early marketing experiments show significant, measurable returns. Financial institutions are reporting improved performance using AI-generated content. However, compliance teams mandate that these AI outputs are treated as official firm communications, subject to fairness standards like UDAAP. This requires a strict process of pre-use approval, archiving, and bias screening for all AI-generated drafts.

2026 Deadlines Concentrate Planning Efforts

The upcoming deadlines are prompting many financial institutions to formalize their AI governance frameworks. The claim mixes several AI-law deadlines and obligations, but the specific table entries should be rechecked against original statutory sources before use.

In response, firms are actively updating their content approval workflows and integrating model-risk management tools into their marketing technology stacks.

Ethical Guardrails and Practical Checkpoints

Industry guidelines emphasize four core principles for AI use: fairness, transparency, privacy, and human accountability. To implement these, financial institutions are establishing practical checkpoints for all client-facing content:

- Disclosure: Adding mandatory AI-use statements to chat widgets and email footers.

- Review: Requiring pre-publication legal review for all AI-assisted marketing materials.

- Archiving: Saving all prompts and outputs to comply with record-retention policies.

- Testing: Conducting routine bias tests on models used for personalized offers.

- Documentation: Keeping detailed inventory logs for each model, its purpose, and data sources.

By embedding these governance steps into creative workflows, firms can continue to innovate with AI while ensuring robust compliance and risk management.

What changes in the coming years for banks and insurers using AI to talk to customers?

The laws create AI governance and disclosure obligations for certain high-risk uses, but the exact wording about all client communications requiring disclosure, fairness proof, and audit trails is overstated.

How will marketing teams have to treat AI copy that once went straight to "send"?

No more "post and forget".

- AI drafts need the same pre-use legal/compliance sign-off as human copy

- Archive prompts AND outputs - regulators want the full conversation

- Disclose when a bot writes or edits public material; certain jurisdictions demand consumer-facing notices for specific systems

Firms that skip the review step risk UDAAP (U.S.) or MiFID/PR (EU) breaches because an AI can quietly drop a key fee or eligibility clause.

Which everyday content pieces are caught first?

Utah requires disclosure upon request in consumer transactions and proactive disclosure for regulated occupations in high-risk AI interactions; Colorado requires pre-use notice and related transparency for consequential decisions; the EU AI Act has separate transparency obligations for certain AI interactions and AI-generated content.

What governance artefacts should be sitting on the shelf by the compliance deadlines?

- Model inventory - every customer-facing AI with version, data owner and risk tier

- Approval log - who reviewed, what changed, sign-off date

- Bias & fairness test results - documented metrics, re-test calendar

- Consumer notices - ready-to-publish blurbs, pop-ups, chat disclaimers

- Escalation path - human override and complaint procedure written into playbooks

Supervisors will ask to see these in upcoming audits.

Where are insurers and banks already seeing upside while they prepare?

- A significant portion of banking and insurance firms are actively using GenAI according to industry reports

- Financial institutions are reporting measurable improvements in customer engagement after implementing AI-optimized content, showing revenue upside is real

- Industry reports suggest many international banks already embed AI somewhere, giving a head-start on data pipelines that new governance rules can leverage

Firms that pair these gains with robust documentation turn compliance into a competitive moat rather than a last-minute patch.