Engdahl's 2028 AI prediction: What it actually means for companies

Serge Bulaev

Overall, there may be more pressure on companies to invest in AI and adapt, or they could fall behind by 2028.

Industry AI predictions about corporate transformation have become a common executive talking point, but their true meaning is often lost. Various forecasts - including predictions about firms lacking AI-driven optimization facing challenges - stem from specific industrial frameworks, not widespread doomsday prophecies. Understanding these predictions' real basis is key to navigating the next few years.

Here, we examine what these frameworks actually cover, which sectors are most exposed, and how forces like regulation and capital will shape the timeline.

What the framework really covers

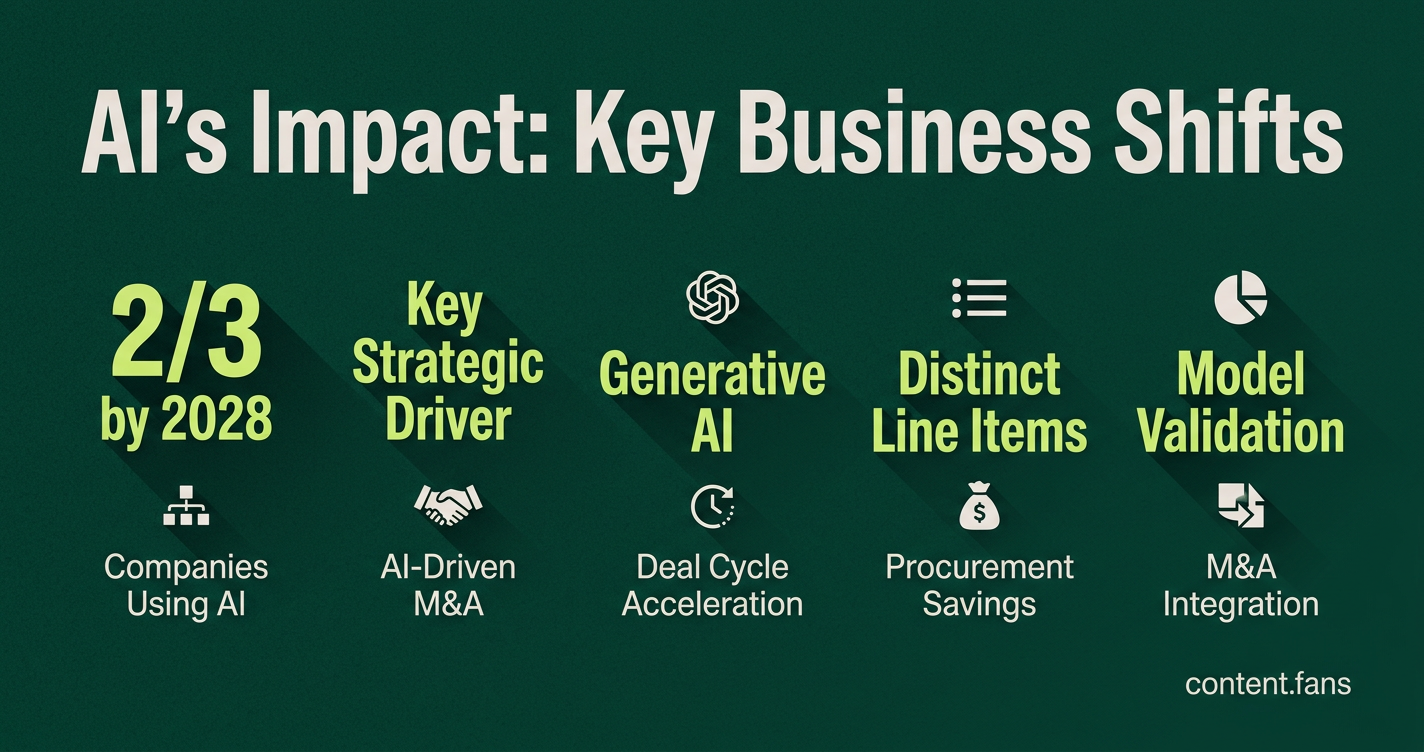

Recent AI predictions focus on specific transformations rather than mass corporate shutdowns. Analysis suggests that by 2028, two-thirds of companies will use AI to manage field service operations, representing a significant shift in how businesses operate rather than a universal corporate extinction event.

Industry analysis argues that industrial software is bifurcating into a deterministic control layer and a probabilistic AI layer. This places software near the user interface, like Manufacturing Execution Systems (MES) and field service tools, at higher risk of transformation. Lacking deep data moats, these systems can be rapidly replaced by agile, AI-native competitors.

The emphasis on continuous, compounding optimization explains why the 2028 timeframe resonates with industry observers. Small efficiency gains accumulate over hundreds of cycles, eventually forcing rivals to either rebuild their technology stack or adapt their market position. The shutdown narrative appears to be an extrapolation of competitive pressure rather than predicted mass closures.

Evidence from recent deal activity

Recent corporate finance data supports this thesis of AI-driven disruption. While PwC's 2026 outlook suggested massive AI infrastructure spending could slow M&A, AI has become a key strategic driver in a significant portion of major deals, according to industry reports. Furthermore, industry analysis suggests that generative AI tools are accelerating deal cycles and reducing costs in diligence and underwriting processes.

In capital-intensive, low-margin sectors like logistics, power, and heavy manufacturing, this acceleration creates a significant gap between AI-adopters and laggards. Research indicates substantial efficiency gains in analytical M&A tasks, suggesting that leadership teams who can fund and integrate AI are gaining a lasting structural advantage.

Board-level signals confirm this shift:

- Procurement savings from AI are being reported as distinct line items.

- M&A integration plans now feature dedicated checkpoints for "model validation".

- CFOs are flagging short-term capex increases for cloud infrastructure and AI model fine-tuning.

- SPACs increasingly list "agent compatibility" as a key criterion for acquisition targets.

Regulation and capital as counterweights

Regulatory headwinds could moderate the pace of change. The EU AI Act has key obligations taking effect on 2 August 2026, while Colorado's AI Act has a separate effective timeline. This fragmented landscape of rules for high-risk and frontier AI models introduces operational complexity that may slow the deployment of some customer-facing systems.

However, capital access provides a powerful counterforce. Well-funded incumbents can absorb compliance costs, turning regulatory burdens into a competitive moat. Smaller firms may need to delay AI adoption or rely on third-party solutions, confirming the thesis that businesses with weak moats face the greatest challenge.

Reading the next three years

While public data doesn't support a wave of imminent shutdowns, it clearly shows mounting pressure on companies. The combination of continuous AI-driven optimization, accelerated business workflows, and a complex regulatory environment creates a powerful dynamic. Industry observers suggest this combination will likely squeeze under-invested firms out of competitive markets, especially those unable to fund the necessary data governance, reskilling, and compliance efforts in time to keep pace.