Anthropic Seeks $30 Billion at $900 Billion Valuation

Serge Bulaev

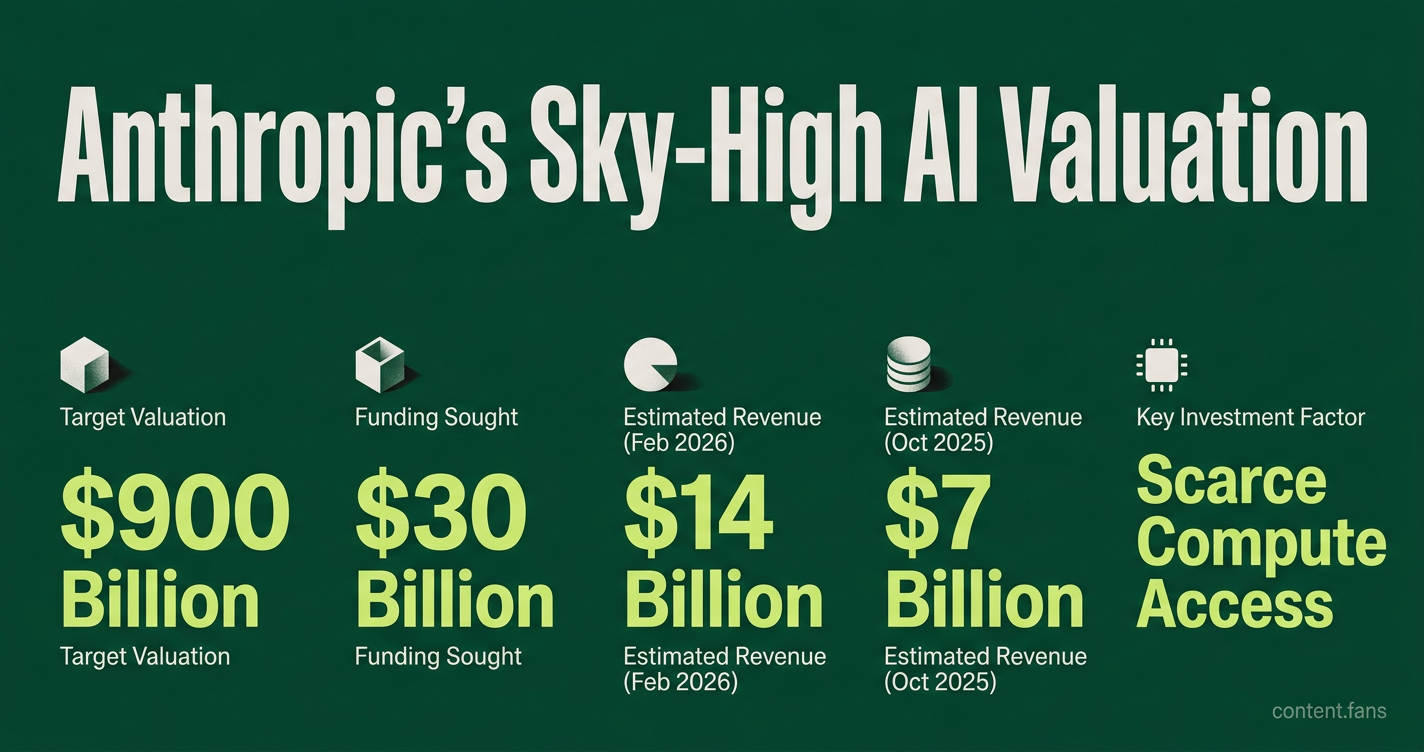

Anthropic is in talks to raise $30 billion at a valuation that may be above $900 billion, but no final deal has been signed yet. Reports suggest this would make it one of the largest startup fundraises ever, and could even reach $950 billion, though the figures are not confirmed. The company's true revenue is not clear, with some sources citing $14 billion in annual sales and others giving higher, unverified numbers. The funding round may include several major investors, and highlights how only a few big players are driving much of the AI industry's growth and risks. If the raise is completed, Anthropic might be able to compete more strongly for resources and talent, but there remains uncertainty about future values and market reactions.

Anthropic is in discussions to raise significant funding at a substantial valuation, according to recent reports that signal a new peak for AI investment. A May 12, 2026, Bloomberg report describes the talks but stresses that no deal is signed. Industry reports later suggested the valuation could reach even higher levels while clarifying the deal is unfinished.

If completed, the round would surpass OpenAI's last private valuation and become one of the largest single startup investments ever recorded. This monumental figure is prompting investors to re-evaluate how they benchmark revenue, capital needs, and competitive risks across the AI industry.

Reconciling Valuation with Revenue

The proposed substantial valuation for Anthropic sets a new benchmark for AI firms, reflecting a potential revenue multiple far exceeding public market averages. While the deal is not final, this figure highlights the intense investor competition and premium placed on leading AI research labs.

While public AI and robotics companies typically trade at significantly lower multiples according to industry reports, late-stage AI venture rounds command far higher multiples. Industry analysts report substantially higher multiples for top-tier companies. Anthropic has not publicly disclosed a formal revenue figure; Reuters reported it was nearing $7 billion in October 2025 and had exceeded $5 billion in August 2025, while later reports cited much higher estimates such as $14 billion in February 2026.

Capital Concentration and Industry Risk

Industry reports suggest the expected large raise may feature several co-leads investing substantial amounts each. This reflects a broader trend where a tight circle of capital providers shapes AI development, with overlapping investor rosters at Anthropic, OpenAI, and other top labs. This concentration is mirrored in infrastructure, where a few deep-pocketed firms drive demand, with industry estimates suggesting aggregate hyperscaler AI capex could reach substantial levels in 2026.

Key Frameworks for Evaluating AI Investments

Funds screening late-stage AI prospects are asking increasingly sophisticated questions to diligence these deals:

- Access to Scarce Compute: Does the company hold long-term, scalable contracts for GPUs and data center capacity to support user growth?

- Talent Defensibility: Are senior researchers locked in with multi-year incentives, or is their equity tied to short vesting schedules?

- Inference Unit Economics: What is the sustainable profit margin after accounting for soaring cloud costs and ongoing safety research?

- Regulatory Resilience: How might a mega-round attract new disclosure requirements or antitrust scrutiny in the US and Europe?

- Exit Optionality: Can an IPO be absorbed at this valuation, or is a strategic acquisition a more probable outcome?

Future Scenarios: Correction or Consolidation

Available source snippets show public SaaS multiples around 5.5x in Q4 2023 and about 3.3x in Q1 2026, suggesting two possible paths. A bullish case sees rapid revenue growth validating today's high private valuations. A bearish case involves slower enterprise adoption, pushing private values toward public benchmarks and accelerating acqui-hire activity. Either way, a multi-billion-dollar infusion would position Anthropic to compete aggressively for compute contracts and senior researchers if the round closes as reported.

What exactly is Anthropic proposing and is the deal final?

Anthropic is in early talks to raise substantial new funding at a significant pre-money valuation, according to industry reports from May 2026. No term sheet has been signed and the deal could still fall apart or change in size; industry reports cited varying ranges for both the funding amount and valuation levels. If it closes, it would be among the largest private tech financings on record and would push Anthropic past many previous valuation milestones.

Key aspects to watch:

- Substantial pre-money valuation floor

- Potentially higher upper bound

- Significant total raise amount

How does the revenue multiple stack up against the market?

With Anthropic's revenue figures varying across reports, the valuation implies a substantial revenue multiple, placing it in the premium tier now seen in late-stage AI companies.

| Segment | Characteristics | Notes |

|---|---|---|

| Public AI/Robotics | Lower multiples | Industry standard |

| Late-stage private AI | Significantly higher multiples | Premium tier |

| Top-decile AI leaders | Substantial premiums | Elite bracket |

The takeaway: AI leaders are valued at an order of magnitude above the broader tech cohort, and Anthropic sits in the upper tier of that elite bracket.

Why are investors willing to concentrate so much money in so few AI names?

Capital is clustering for three immediate reasons:

- Scarce compute: Hyperscalers are investing heavily in AI-related infrastructure - owning or partnering with a frontier lab is viewed as the only way to secure future capacity.

- Talent scarcity: A significant portion of venture funding now lands at AI startups, pushing median startup salaries and initial equity grants substantially higher.

- Follow-the-leader momentum: A small club of crossover funds already holds positions in multiple leading AI companies, creating a feedback loop where each new mega-round justifies the last.

The result is a two-tier market: AI or everything else.

How might regulators and competitors respond?

- Antitrust spotlight: Anthropic raised substantial funding in a Series G round at a high post-money valuation, though specific competition review risks vary by jurisdiction.

- Rival fundraising sprint: Expect OpenAI, xAI and Cohere to accelerate their own rounds to stay within striking distance.

- Talent bidding war: Compensation bands for senior researchers could reach substantial levels, pushing non-AI startups to either acqui-hire teams or exit entirely.

What frameworks should investors use to judge major AI rounds?

- Compute-adjusted burn: Estimate cost trajectory - does the new capital at least double effective compute per dollar spent?

- Revenue-to-inference ratio: Divide total revenue by monthly inference cost - low ratios are unsustainable at scale.

- Investor overlap delta: Track the percentage of new capital that also backs direct competitors - high overlap suggests strategic rather than purely financial money.

- Talent retention metric: Model equity refresh grants needed to keep top researchers for multiple years; excessive dilution breaks valuation math.

- Exit velocity scenario: Stress-test the cap table against valuation corrections; a healthy firm should still raise a flat or up-round under those conditions.

Use these filters before joining what might soon become an exclusive club with only a handful of members.