Anthropic, OpenAI account for 89% of top AI startup revenue

Serge Bulaev

Recent reports suggest that Anthropic and OpenAI together make up about 89% of the revenue among leading AI startups. Analysts believe this may show where money, talent, and power could gather in the AI industry. The share of revenue held by these two companies appears to be growing, possibly making it harder for smaller startups to compete. Some experts note that only a few companies are seeing big profits from AI so far, and many are still figuring out how to make money from it. It also appears that regulators and customers are watching closely to see how the balance of power might shift in the future.

A new report reveals Anthropic and OpenAI account for 89% of top AI startup revenue, indicating a powerful duopoly is forming. The two AI model providers dominate revenue generation in a field with dozens of competitors, signaling a major consolidation of capital, talent, and pricing power in the AI economy.

A Snapshot of AI Revenue Concentration

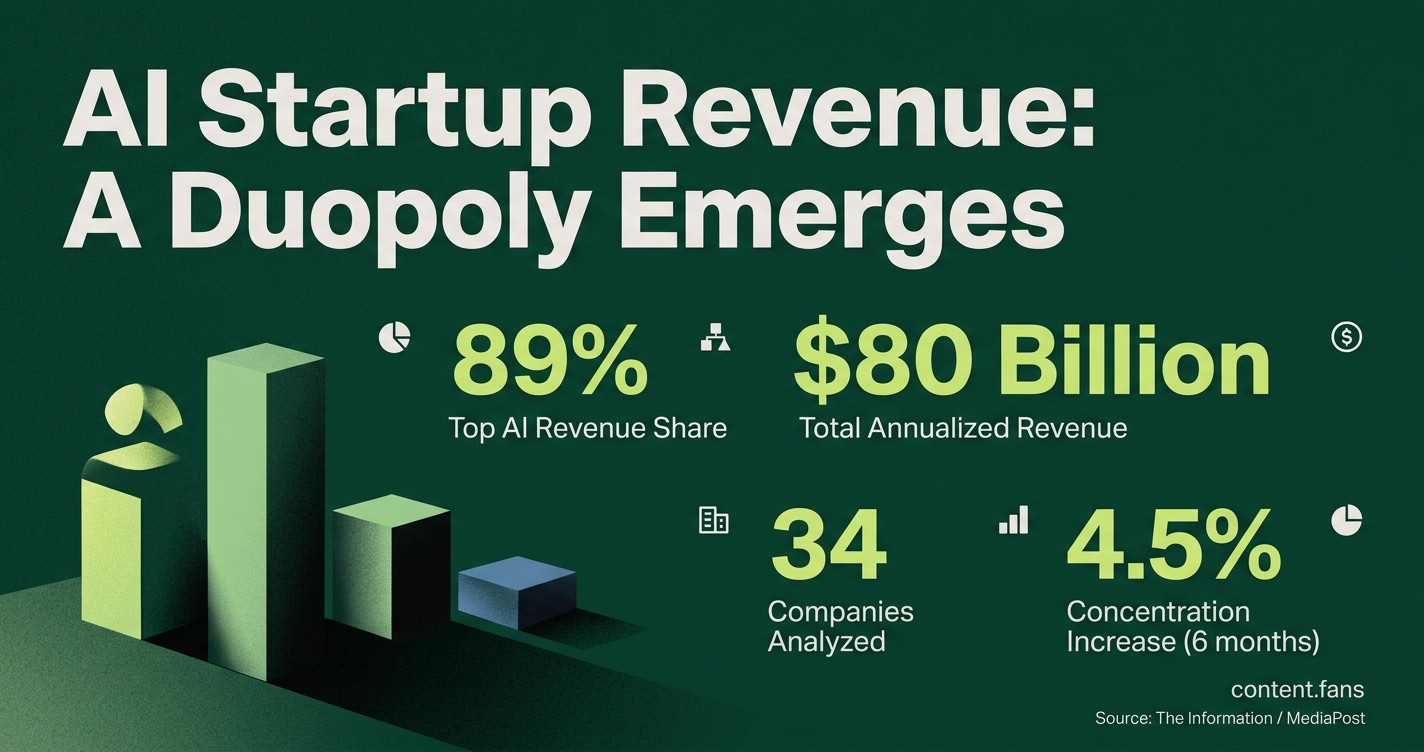

Recent analysis of 34 private AI companies shows a significant market concentration. Anthropic and OpenAI command a combined 89% of the group's total annualized revenue. This leaves the remaining companies to compete for the final 11%, highlighting a stark revenue gap between the leaders and the rest.

Data from The Information, also reported in MediaPost coverage from May 2026, analyzed 34 private AI firms. The cited report says the 34 leading AI startups are generating close to $80 billion in annualized revenue, with Anthropic and OpenAI together accounting for about 89% of that total. Anthropic accounts for nearly half of this figure, driven by high demand for its coding and workflow automation tools. It's noted that Anthropic's revenue may include partner-shared income from cloud providers like Amazon and Google, a common practice that can complicate direct comparisons. Despite this, the data shows concentration increased by 4.5 percentage points in just six months, indicating the market leaders are growing fastest.

How concentration shapes the emerging stack

This market concentration has several critical implications for the broader AI ecosystem:

- Fundraising Pressure: Venture capitalists are increasingly directing major investments toward established model developers. This concentrates capital, forcing application-focused startups to vie for a shrinking funding pool.

- Talent Migration: Top AI engineers and researchers are drawn to well-resourced industry leaders, creating a talent gap that smaller companies struggle to overcome.

- Pricing Power: Dominant firms can set API rates across the market, potentially squeezing the profit margins of application builders who rely on their models.

- Regulatory Scrutiny: Such high market concentration naturally attracts attention from regulators. Dominance can trigger antitrust investigations, a concern detailed in a recent OECD competition brief.

Competitive responses emerging in 2025

To survive, smaller AI companies are adopting several key strategies:

- Niche Specialization: Focusing on specific domains like legal research or radiology where proprietary data can deliver superior model performance.

- Deep Workflow Integration: Embedding their technology into essential enterprise systems to create high switching costs for customers.

- Strategic Cloud Partnerships: Partnering with major cloud providers to gain access to compute resources at preferential rates, trading lower margins for broader distribution.

However, the success of these strategies is not yet guaranteed. According to industry reports, only a significant portion of firms are capturing exceptional value from AI. Similarly, industry surveys suggest that while many businesses report innovation gains, a growing number have yet to see significant profit increases, suggesting the path to monetization remains unclear for many.

What industry watchers will monitor next

Looking ahead, several key factors will determine the future of competition in the AI market:

- Training Costs: The capital required for model training is a major barrier. Any breakthroughs that dramatically lower these costs could open the door for new competitors.

- Regulatory Action: Watchdogs are closely examining exclusive deals for compute power and data to ensure they don't unfairly block new companies from entering the market.

- Customer Behavior: Many businesses are exploring multi-model strategies to avoid vendor lock-in. If it becomes easier to switch between providers, the influence of any single dominant player could decrease.