AI Infrastructure Startups Raised $3.2B In January 2026 As VC Focus Shifts

Serge Bulaev

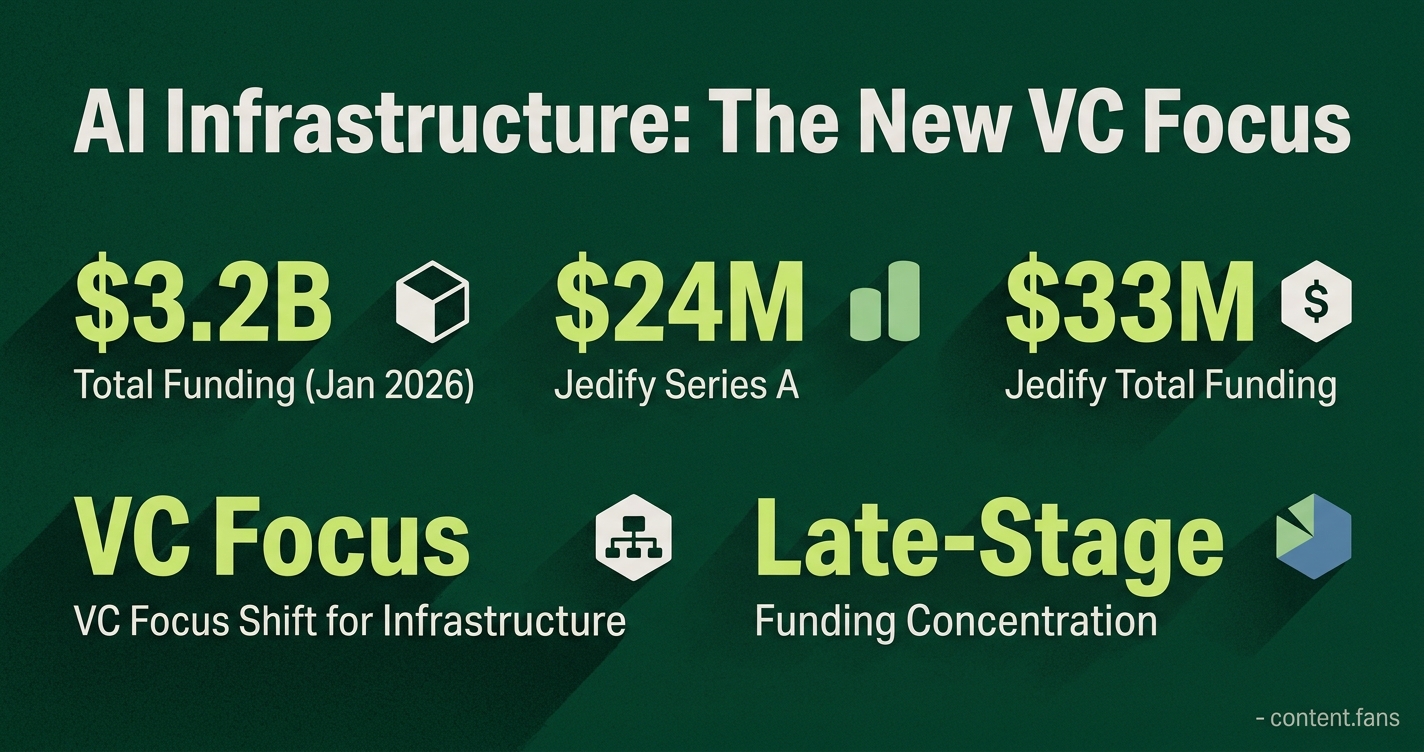

In January 2026, AI infrastructure startups raised about $3.2 billion across 32 deals, which appears to show a rebound in VC interest after a slowdown in late 2025. Most investment seems to be going to larger, later-stage companies, suggesting the market may be focusing on category leaders. Some areas, like failure detection and observability, get a lot of attention even if they receive less money overall. Analysts say the market may soon see more mergers or shutdowns, especially among vendors of observability tools, execution engines, and interoperability protocols. Experts believe the AI infrastructure field might end up with a few big winners and many smaller specialists by 2027.

Following a brief slowdown, venture capital focus is shifting decisively toward AI infrastructure startups, with industry reports indicating significant funding activity in early 2026. Investors are now prioritizing the essential "plumbing" - tools for failure detection, observability, and deployment monitoring - over speculative model development.

This strategic pivot reflects a market maturing from research to revenue. With AI capturing a significant portion of global venture capital according to industry reports, a growing share of that capital is now funding the production-grade systems required for real-world applications.

Early 2026 Funding Rebounds, Focuses on Market Leaders

AI infrastructure funding showed a significant rebound in early 2026, signaling renewed investor confidence. The capital is concentrating in late-stage rounds for category leaders, with a strong focus on tools for failure intelligence, context management, and observability for production-level AI systems.

Following a dip in late 2025, the new year saw a significant rebound according to industry tracking reports. This trend signals a "flight to quality," as industry reports suggest the value of late-stage deals grew substantially year-on-year while deal counts showed more modest growth. This market behavior indicates investors are consolidating bets on perceived category leaders rather than seeding a wide array of new ventures.

While representing a smaller portion of the total capital, startups in failure intelligence, context graphs, and observability are generating significant market buzz. Recent funding rounds highlight that early-stage capital remains available for companies addressing critical reliability gaps in enterprise AI. Meanwhile, Jedify was publicly reported on June 10, 2026 to have raised $24 million in a Series A round led by Norwest, bringing total funding to about $33 million.

The Emerging Ecosystem: Key Players and Platforms

Investment capital is currently clustering around three distinct groups of players:

- Cloud Incumbents: Giants like Microsoft, Google, and Amazon are integrating agentic frameworks directly into their existing cloud platforms.

- Horizontal Specialists: These startups focus on cross-platform layers for critical functions like durable execution, observability, and evaluation.

- Middleware and Standards: A third category includes efforts to establish protocol-level portability and interoperability between different AI systems.

Within this landscape, a battle is emerging for the definitive "operating layer" for LLM agents. Early data from trackers monitoring numerous agentic tools suggests developer adoption is already converging on a few key orchestration and memory frameworks. Similarly, the observability space is expected to consolidate, potentially mirroring the DevOps market where only a handful of dominant cross-vendor platforms achieved mass scale.

Consolidation Looms: Which AI Infrastructure Segments Will Merge First?

Industry analysts predict a wave of mergers and acquisitions, pointing to three segments facing immediate consolidation pressure:

- Observability Stacks: As enterprises scale customer-facing agents, the need for consistent performance and compliance metrics will drive them to standardize on a smaller number of vendors.

- Execution Engines: The high operational costs (particularly GPU resources) of durable agent runtimes may force standalone companies to seek acquisition by larger, better-capitalized players.

- Interoperability Protocols: With the ecosystem coalescing around a few dominant messaging standards, tools built on competing protocols risk becoming obsolete.

An active M&A environment is already evident, with numerous transactions in agentic AI reported in recent years. Industry experts suggest that the AI infrastructure market may stabilize in the coming years, potentially resembling the cloud monitoring sector with a few horizontal giants and a vibrant ecosystem of specialized vertical solutions.