Seed AI Valuations Surge 42% Amid Mega Private Rounds

Serge Bulaev

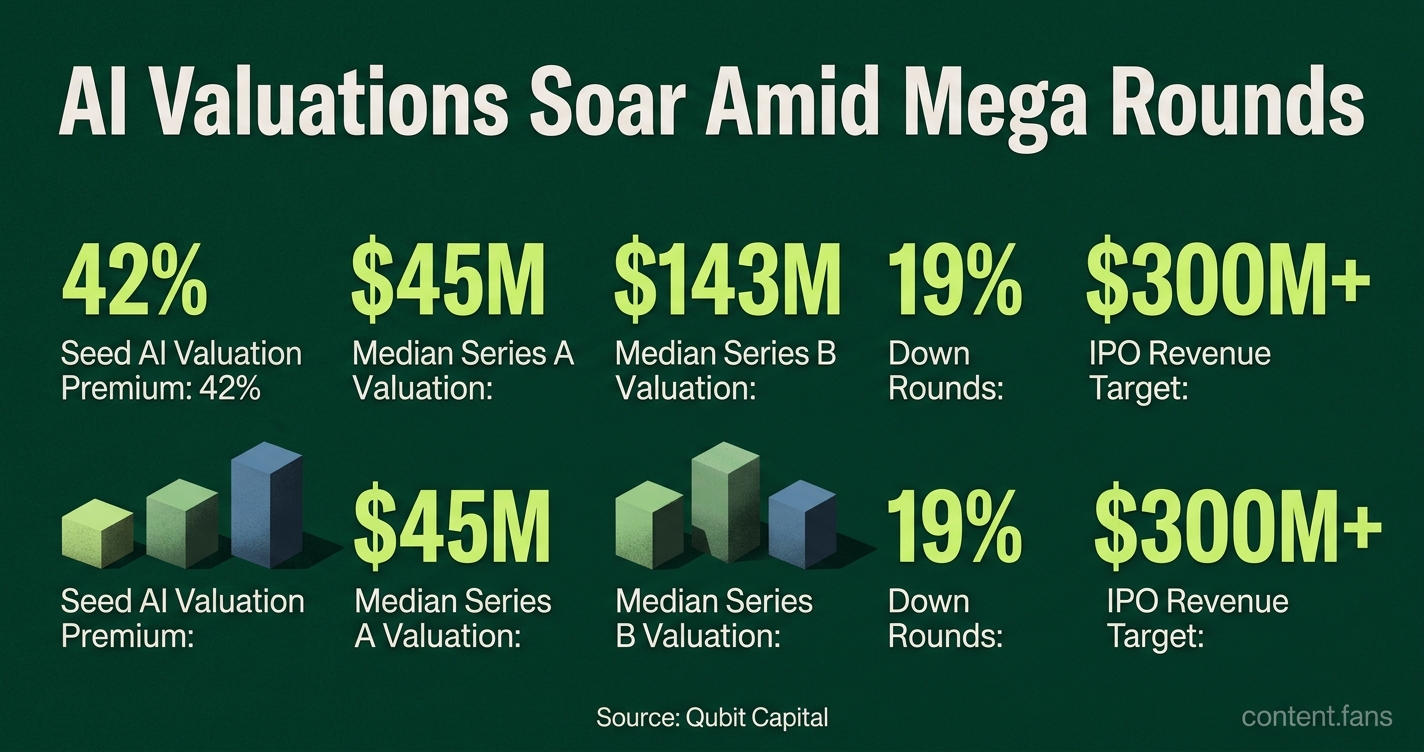

Seed-stage AI companies may have seen a 42 percent higher valuation compared to other startups, and mega private rounds appear to have become a key way for startups to raise money from 2024-2026. While valuations have gone up, nearly one in five deals were still down rounds, suggesting a split market. Well-funded startups seem able to hire faster and grow quickly, but this may put pressure on smaller companies and make it harder for them to compete. Founders might need to show strong growth to keep high valuations, and staying private longer could give more control but also brings added risks and expectations.

The surge in seed AI valuations is driven by mega private rounds, which became a core financing vehicle from 2024-2026 and fundamentally reshaped startup growth strategies. While data shows a median Series A valuation of $45 million, a split market persists with 19% of deals being down rounds. This divide is starker in AI, where seed-stage AI companies command a 42% valuation premium and Series B medians reach $143 million, according to Qubit Capital. Ultimately, these mega-rounds provide the capital for rapid scaling but also concentrate risk, pressuring founders to deliver on high valuations at an accelerated pace.

Mega private rounds and valuations

Mega-rounds have inflated headline valuations across most stages, though investors remain highly selective. Capital is increasingly "squeezed into fewer, much larger rounds," creating a winner-take-most environment, as noted in Qubit Capital's 2026 briefing. While category leaders see valuation growth, many other startups face resetting terms. This dynamic sets a higher growth bar for founders, where missing targets could lead to damaging down rounds.

The surge in AI startup valuations is fueled by intense investor competition for category-defining companies. Mega private rounds have become the primary mechanism to deploy large amounts of capital, enabling rapid scaling but also concentrating funding into a select group of perceived winners, leaving others to face tougher terms.

Competitive dynamics and the talent race

Access to massive capital allows well-funded companies to outpace rivals in hiring, sales expansion, and acquisitions. Qubit Capital highlights this creates an uneven playing field, giving early-stage competitors little room to maneuver. This capital concentration can also dampen innovation by reducing the number of funded experiments. Consequently, smaller startups struggle to attract talent and customers, who often prefer the perceived stability of mega-funded firms.

Founder incentives and later-stage capital markets

The influx of billions from crossover and sovereign funds allows companies to delay IPOs, often until they surpass the $300 million revenue mark favored by public markets, according to Forge Global. While structured secondary programs provide employee liquidity and aid retention, timing remains critical. As Reach Capital advises, founders should raise capital from a position of strength and momentum - not desperation - to secure favorable pricing and minimize dilution.

Recommendations for navigating a mega round

A focused, strategic playbook is essential for navigating a mega round. Key actions include:

- Curate a shortlist of 20-30 funds aligned with your sector and check size.

- Present new customer wins or product milestones during diligence to influence committees.

- Combine a generalist growth lead with a specialist co-investor to enhance credibility.

- Carefully structure secondary sales to reward early employees without deterring new investors.

- Model downside scenarios to understand potential valuation compression if growth targets are missed.

Trade-offs: private life vs public readiness

While staying private longer affords founders more control, accepting a billion-dollar valuation necessitates adopting public-market discipline sooner. The risk of future down rounds - as evidenced by Carta's data - is significant if growth falters. Founders must carefully weigh the advantages of accelerated market share against the heightened governance, reporting, and dilution pressures of mega-raises. For investors, the challenge is balancing the concentration risk against the potential for outsized returns from a category winner.

What is driving the 42% valuation premium for seed-stage AI companies?

Investor appetite is concentrated on AI-first teams that can show live traction.

According to Qubit Capital, median seed AI valuations have jumped 42% above non-AI startups in 2026, while Series A rounds routinely clear the $50 million mark and Series B medians sit at $143 million. The premium is not just hype - it reflects the $130 billion that flooded AI companies in the previous cycle and the $300 billion in planned AI cap-ex from megacaps that underwrites future demand.

How do mega private rounds change day-to-day competition for smaller startups?

Winners can out-spend rivals on talent, data and GPU access, raising the "proof" bar for everyone else.

Qubit Capital notes that once a company locks in a mega-round it can accelerate hiring, research and data acquisition at a pace early-stage competitors rarely match. The same report warns that new founders now need real traction before serious money shows up, because capital is being squeezed into fewer, much larger rounds.

What concrete challenges do under-funded startups face when hiring and selling?

- Talent: mega-funded players offer higher base salaries, signing bonuses and perceived stability; 90% startup failure stats make recruits risk-averse.

- Customers: buyers prefer well-capitalized vendors to avoid product-dead risk; Crunchbase data show five AI mega-rounds alone captured 20% of 2025 VC dollars, reinforcing the "safe-vendor" bias.

- Distribution: large firms out-spend on paid acquisition, conferences and channel deals, forcing smaller startups to prove capital efficiency and measurable outcomes before gaining share.

Should founders take the largest late-stage check available or stay lean and head toward IPO sooner?

Take the round only if the capital buys a defensible lead; otherwise the dilution and scrutiny may outweigh the benefit.

Forge Global reports that private liquidity (secondaries, tender offers) now lets teams stay private longer, while IPO thresholds have climbed to >$300 million revenue and >$2 billion public-market cap. Reach Capital adds: raise when momentum is strongest, not when cash is lowest, and run a time-bound, thesis-aligned process with 20-30 target funds rather than a broad spray.

How should investors underwrite a $1 billion+ Series H or similar mega deal?

- Check the burn-multiple against the stated 3-5 year product roadmap - mega rounds can hide unit-economic drift.

- Model exit liquidity: at IPO thresholds above $2 billion, only a handful of buyers can absorb the float; verify that revenue diversification and >20% YoY growth meet public-market gatekeeping.

- Stress-test cap-table governance - large crossover funds may demand structured liquidity or downside protection that skews incentives in a down-cycle.