PitchBook: Agentic AI Shifts SaaS Valuations to Workflow Ownership

Serge Bulaev

PitchBook's report suggests that agentic AI is changing how investors value SaaS companies, with more focus on workflow ownership instead of just revenue. It appears that owning data and process control may be more important than adding new features. Some sources say that as AI agents get more integrated, pricing models might shift from seat-based to usage or outcome-based. However, the adoption of these agents seems slower in some areas, and there may still be security and reliability challenges. Overall, investors might look at how deeply platforms integrate and control workflows when deciding where to put their money.

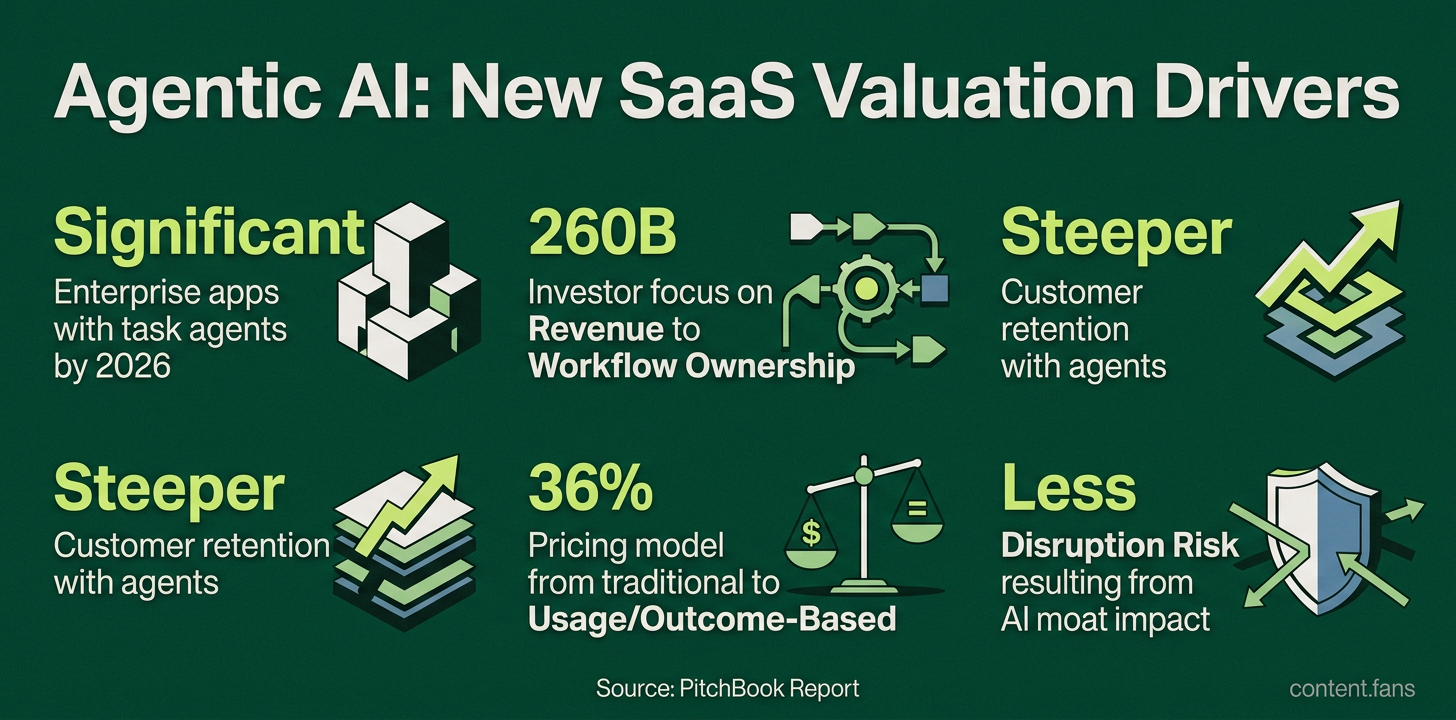

A new PitchBook report on agentic AI shifts SaaS valuations by emphasizing workflow ownership over surface-level revenue. The analysis suggests investors are re-evaluating software winners, favoring sticky, ERP-like systems over applications prone to churn. This pivot means that owning data, orchestration, and process control is becoming more critical for long-term value than feature velocity, causing a shift in how venture capital assesses moats.

Why ERP-style dynamics change the competitive map

Agentic AI is reshaping SaaS valuations by shifting investor focus from recurring revenue to workflow ownership. VCs now favor platforms that demonstrate deep system integration, control over proprietary data, and the ability to automate end-to-end processes, mirroring the sticky, long-term nature of enterprise resource planning (ERP) systems.

Like historical ERP implementations, emerging AI agents are defined by deep, slow integration that leads to long-term embeddedness. PitchBook argues that while pilots proliferate, production deployment depends on robust governance, data quality, and system connectivity. This view is echoed by industry reports, which forecast a move from seat-based pricing to usage or outcome-based models as agents automate core tasks. Oliver Wyman argues that software with strong AI-ready moats and defensible positioning is less exposed to AI disruption, while noting that AI can commoditize features and interface directly with software.

According to industry reports, a significant portion of enterprise apps will feature task agents by 2026, representing a dramatic increase from current levels. However, research shows a gap, with many companies still working to fully embed agents. This disparity highlights the ERP-like adoption cycle: broad experimentation followed by slower, more deliberate organizational integration.

Investor Scorecards: Swapping Revenue Multiples for Integration Depth

PitchBook cautions that traditional revenue multiples can misrepresent the value of private agentic AI companies. Instead, savvy investors are tracking capital concentration around platforms that own the entire workflow and its resulting data exhaust. The most valuable alternative metrics now include:

- Integration depth across core enterprise systems

- Rate of proprietary data accumulation

- Time required to move from proof-of-concept to production

- Net revenue retention linked directly to usage-based pricing

- Enterprise sales cycle velocity compared to similar ERP deals

Oliver Wyman notes that customer retention curves become steeper when agents execute tasks rather than merely assisting users. Industry analysts also identify hybrid pricing models as a key factor for stabilizing margins where autonomous agents, not people, drive platform activity.

Case Studies Underline Capital Concentration

PitchBook's dataset reveals a clear trend: venture capital is consolidating around companies that combine powerful orchestration engines with domain-specific data. Although the report's raw data is proprietary, its analysis points to a rising median Series B valuation for workflow-centric platforms compared to standalone copilots. This suggests investors are already awarding premiums to businesses whose unit economics are based on embedded control, not just user counts.

This capital flow is corroborated by industry consultants. Research frameworks present multiple potential SaaS futures, with many scenarios seeing agentic platforms consuming significant budget from surface-level applications. Early evidence already indicates significant pricing pressure on seat-based models as enterprises shift their spending toward outcome-based contracts.

Operational Hurdles Remain

Despite the opportunity, sources caution that production-grade agents still face significant security, compliance, and reliability challenges. Research shows that many pilot projects stall due to data silos or outdated APIs that prevent true end-to-end automation. Consequently, industry forecasts suggest a near-term reality where agents primarily handle support, retrieval, and recommendation tasks, leaving core financial and supply-chain systems untouched for now.

PitchBook concludes that its private-market data acts as a leading indicator for where workflow control is consolidating. By monitoring deal velocity and capital allocation in integration-heavy sectors, investors can identify which platforms are successfully transitioning from promising experiments to indispensable enterprise staples.