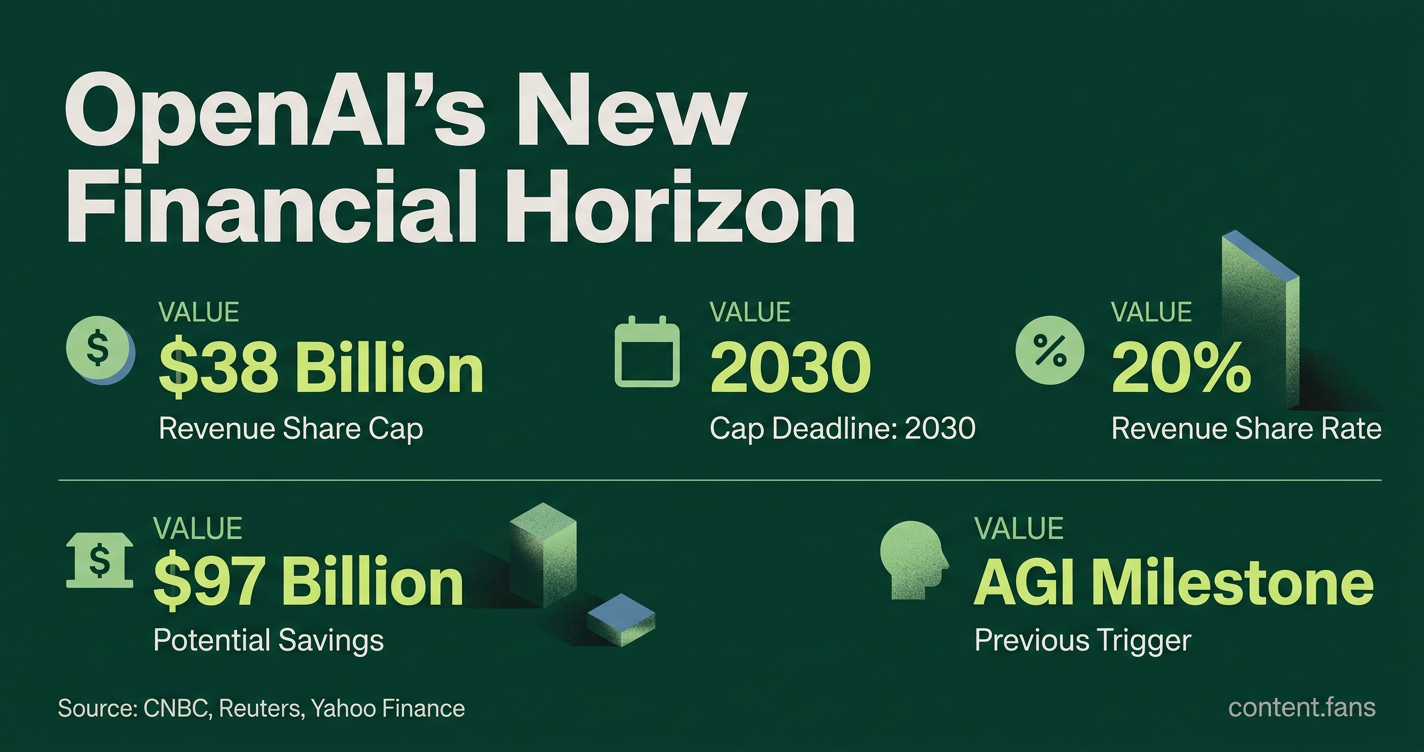

OpenAI caps Microsoft revenue share at $38 billion through 2030

Serge Bulaev

OpenAI and Microsoft have changed their partnership so that OpenAI will pay Microsoft no more than $38 billion in revenue sharing through 2030. OpenAI will continue to give Microsoft 20% of its revenue until this limit is reached. Some reports suggest that this may help OpenAI save money and make its finances clearer for investors. The new agreement also removes a rule that tied payments to a specific AI milestone, making payments based only on time. Details are based on press reports and the contract itself has not been made public, so some uncertainty remains.

In a strategic revision to their landmark partnership, OpenAI now caps its Microsoft revenue share at a cumulative $38 billion through 2030. This amendment places a definitive ceiling on payments to its largest investor, potentially saving OpenAI up to $97 billion, according to press reports. The new terms clarify OpenAI's long-term financial obligations, providing greater certainty for investors and signaling a potential shift in the economics of major AI platform alliances.

According to a CNBC report, the agreement maintains the existing 20% revenue-sharing rate until the $38 billion cap is reached. A separate Reuters analysis suggests this financial restructuring is designed to strengthen OpenAI's position ahead of a potential public offering by creating more predictable cash-flow models.

How the Cap Reshapes 2026-2030 Forecasts

The revised agreement caps OpenAI's cumulative revenue-sharing payments to Microsoft at $38 billion through 2030. The 20% revenue share rate remains until the ceiling is met. This change makes financial obligations time-based, removing previous AGI-related triggers and improving predictability for investors.

Key terms of the amended agreement include:

- Total Payout Cap: $38 billion cumulative through 2030.

- Revenue Share Rate: 20% of OpenAI revenue until the cap is reached.

- Agreement Term: Effective through the end of 2030.

This structure introduces a critical inflection point. While moderate growth may not trigger the cap, rapid revenue expansion would cause it to be met sooner. Once reached, Microsoft's share of revenue growth would cease, directly boosting OpenAI's gross margin. As noted by Reuters, this predictability strengthens OpenAI's financial narrative for investors analyzing free-cash-flow potential.

Furthermore, CNBC reports the removal of a clause linking payments to an artificial general intelligence (AGI) milestone. This transforms the obligation from a technology-contingent liability to a time-based expense, simplifying earnings models for analysts.

Signal to the Wider AI Startup Market

This deal directly addresses the growing investor scrutiny of "round-trip funding" - a practice where cloud providers invest in startups that then spend the capital on that same provider's services. As noted in Yahoo Finance commentary, investors have questioned the durability of such revenue streams. By capping one of the industry's most significant funding loops, the deal may alleviate these concerns while maintaining the core commercial relationship. Microsoft remains OpenAI's primary cloud provider with first-release rights on Azure.

For the broader market, this move carries two key implications. First, as Economic Times observers note, it aligns with Microsoft's strategy to diversify its AI partnerships beyond a single lab. Second, it demonstrates to other startups that achieving significant scale can provide the leverage needed to renegotiate contracts and pursue more flexible, multi-cloud strategies.

Precedents in Tech Deal Renegotiation

The OpenAI-Microsoft amendment aligns with a broader trend of high-value technology partnerships renegotiating economic terms. Legal analysts at Skadden draw a parallel to the European Commission's 2026 guidance on licensing negotiation groups for patent royalties, which also encourages collaborative reshaping of payment structures. Both instances highlight a growing willingness among major tech players and regulators to reconsider established financial splits in strategic alliances.

While the full contract remains private, the figures disclosed in press reports establish a new benchmark for AI partnerships dependent on heavy cloud computing investment. The $38 billion ceiling offers analysts a firm upper boundary for Microsoft's potential return and clarifies OpenAI's maximum financial exposure through 2030, setting a significant precedent for future deals across the AI industry.

What exactly is the new revenue-sharing cap between OpenAI and Microsoft?

OpenAI's revenue-share payments to Microsoft are now capped at a cumulative $38 billion through 2030. The existing 20% revenue-share rate applies until this cap is met. While Azure remains OpenAI's primary cloud provider, reports indicate OpenAI has more flexibility to use other clouds.

How much cash could OpenAI save under the cap?

Compared to an uncapped 20% payout, Reuters estimates the new ceiling could save OpenAI approximately $97 billion through 2030. The cap also makes the obligation a predictable expense by removing performance triggers tied to AGI milestones, which helps in forecasting gross margin and free cash flow.

Does the cap weaken Microsoft's strategic position?

No, Microsoft's strategic position remains strong. It retains first-call deployment rights, meaning new OpenAI products must launch on Azure unless Microsoft declines. While some exclusivity is reduced, reporting suggests the change is strictly financial, and OpenAI's operational dependence on Microsoft's computing infrastructure continues.

How might capped revenue sharing affect AI start-ups?

The cap helps legitimize the funding model by limiting concerns about "round-trip funding." According to Yahoo Finance, this may ease investor scrutiny. Startups with clear multi-cloud roadmaps may now be viewed more favorably, while those dependent on a single cloud partner could face tougher questions about customer-concentration risk.

Could other platform partnerships copy this model?

Possibly. The $38 billion ceiling serves as a powerful template for other platform partnerships. However, replicating it depends on specific contexts. While precedents like the EU's licensing-negotiation group guidance exist, legal experts at Skadden warn that regulatory acceptance, particularly from U.S. antitrust agencies, is not guaranteed and remains deal-specific.