Enterprise AI spending shifts to infrastructure, hitting $2 trillion by 2026

Serge Bulaev

Enterprise AI spending may reach $2 trillion by 2026, with a shift in focus from AI models to infrastructure like hardware and governance. Reports suggest that most companies are investing more in platforms that connect and manage data, policies, and workflows across different systems. Many organizations feel less prepared in areas like infrastructure and talent, which may indicate a long-term need for tools that simplify complexity. Hybrid deployment appears to be growing quickly, and companies view shared infrastructure as a safer way to manage AI. Startups may stand out by offering integrated infrastructure solutions, while CIOs are focusing on solving integration challenges.

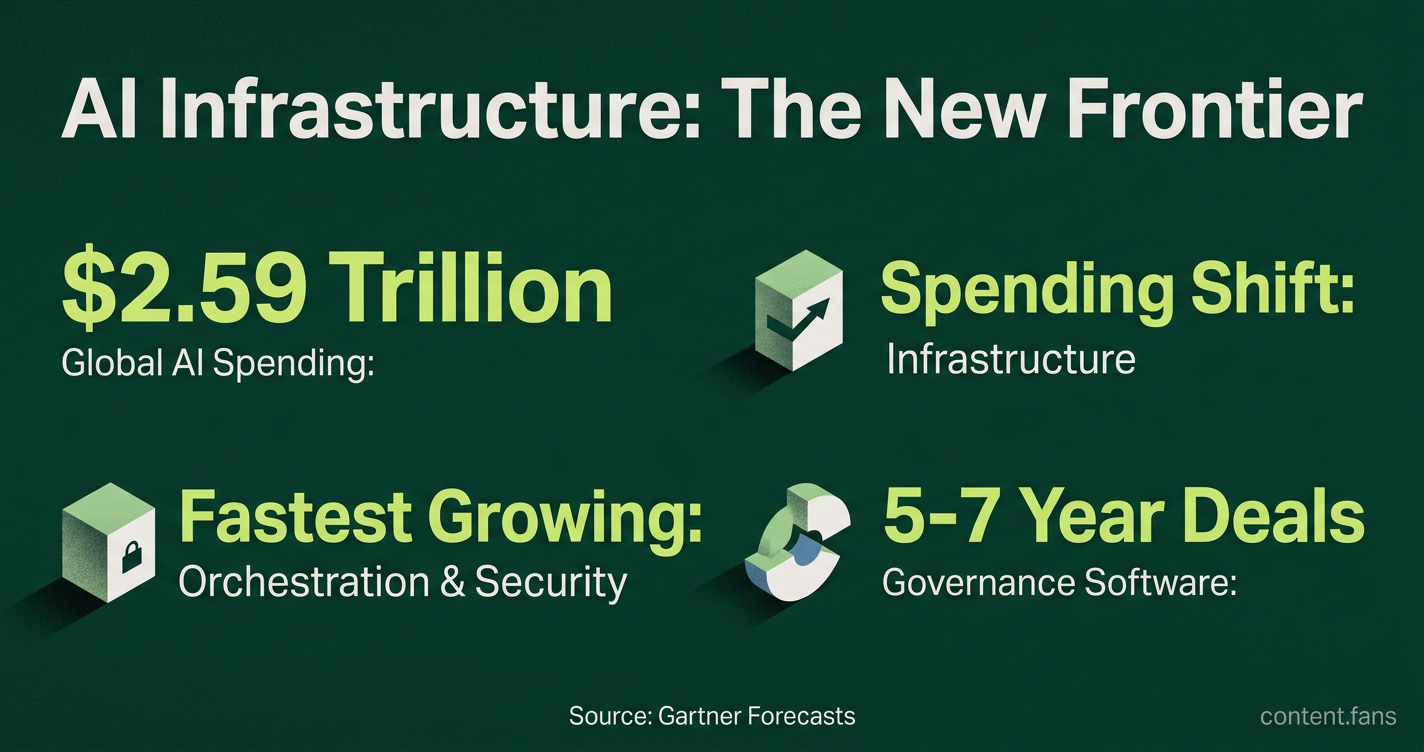

Gartner forecasts worldwide AI spending at approximately $2.59 trillion by 2026, yet most of the new money is not chasing flashier models. It is chasing the plumbing that lets models run at all: hybrid cloud fabrics, GPU clusters, orchestration layers, audit trails, and the connectors that glue everything to the order-entry screen your sales team already knows.

Wall Street is starting to price the platform above the parameters. Three converging forces explain why:

- Model capability is rising faster than model differentiation.

- Regulation is arriving region by region, forcing audit-ready pipelines.

- CIO budgets are shifting from "science experiments" to production SLAs.

Below is a concise FAQ that boards, investors, and product teams are already circulating.

Why is infrastructure, not the base model, becoming the bottleneck?

Enterprises are shifting focus from raw model performance to operational maturity. The true bottleneck has become the infrastructure needed to manage data, ensure governance, and scale AI workloads securely across complex hybrid cloud environments, which is essential for realizing value from AI investments at enterprise scale.

Hybrid cloud architectures changed the finish line. When GPU workloads, corporate data, and end-user SaaS all meet in the same 40 millisecond SLA window, the choke point becomes data gravity and governance, not raw FLOPS. Industry reports indicate that a significant portion of enterprises have yet to move past pilot clusters, with many organizations still working to address identity, lineage, and cost allocation challenges across on-prem, VPC, and edge footprints. Fixing those pipes is what unlocks the next 10× user scale.

Which sub-segments are pulling the biggest share of global AI spending?

Hardware still dominates dollar volume according to industry reports, with a substantial portion of new AI infrastructure investment going to accelerated compute, racks, and liquid-cooling modules. But the fastest-growing slice appears to be the orchestration and security layer, which industry analysts project will see significant growth through 2032. The spend mix matters: accelerators depreciate in three-year cycles; governance software locks in five-to-seven-year SaaS deals with built-in renewal paths.

What evaluation framework should executives use to avoid "vendor lock-in" vs "own the stack" debates?

Four practical filters surface quickly in recent CIO surveys:

- Portability: can the workload move between CSPs without rewriting policy-as-code artifacts?

- Observability: is inference telemetry joined to business KPIs in near real time?

- Compliance: does the platform embed region-specific retention, consent, and model-cards evidence?

- Pricing flexibility: does the contract separate compute, storage, and support so you can re-balance when GPU prices fluctuate?

Industry reports suggest that platforms addressing all four areas command premium valuations in private markets compared to those with gaps in their offerings.

How should startups position against incumbents that already own the data center door?

Differentiate on workflow depth, not model novelty. The most recent wave of Series A pitches winning term sheets embed connectors for the three systems of record CIOs care about - ERP, CRM, and ticket queues - and expose an SLA dashboard first, model card second. Investors reward this sequencing because once the governance layer is sticky, swapping a faster LLM in later is trivial.

What early warning metric on the earnings call best predicts who monetizes the shift?

Watch gross-margin contribution from noncompute services - i.e., professional services plus recurring platform seats. When that line outgrows bare-metal revenue for two consecutive quarters, the vendor is turning infrastructure into a durable software annuity, not a one-time hardware purchase. Market analysis suggests that firms crossing this threshold tend to command higher forward EV/EBITDA multiples than peers still selling racks on a cost-plus basis.

Industry projections indicate that AI infrastructure will support a substantial majority of global enterprise workloads by 2026, yet only the vendors that master connectors, audit trails, and hub-and-spoke governance will keep the wallet share when the next model inevitably arrives.