Dairy Processors Balance WPI Expansion With Nutrition Platforms

Serge Bulaev

Dairy processors are trying to grow their whey protein production while also building new nutrition platforms, as profits from whey are still good but customers want more complete nutrition products. High prices for whey protein may keep investment strong, but experts warn new factories could lower prices by 2027. There appears to be a move toward offering custom mixes and services, not just bulk protein, which might make earnings more stable. The article suggests that building small, skilled teams and focusing part of investment on these new capabilities may help manage risk. Success may depend on tracking both internal performance and market trends to see if this dual strategy is working.

Global dairy processors balance WPI expansion with nutrition platforms as they navigate a complex market. While attractive margins from whey proteins encourage building new capacity, customers increasingly demand comprehensive, turnkey nutrition solutions. This article reviews market signals, capex trends, and practical steps supporting a dual-track strategy.

Tight whey markets keep capex flowing

Processors face a strategic choice: invest in high-margin whey protein isolate (WPI) production to meet current demand, or build versatile nutrition platforms that offer long-term revenue stability. The risk is that new WPI capacity could depress future prices, making diversified, value-added services more attractive.

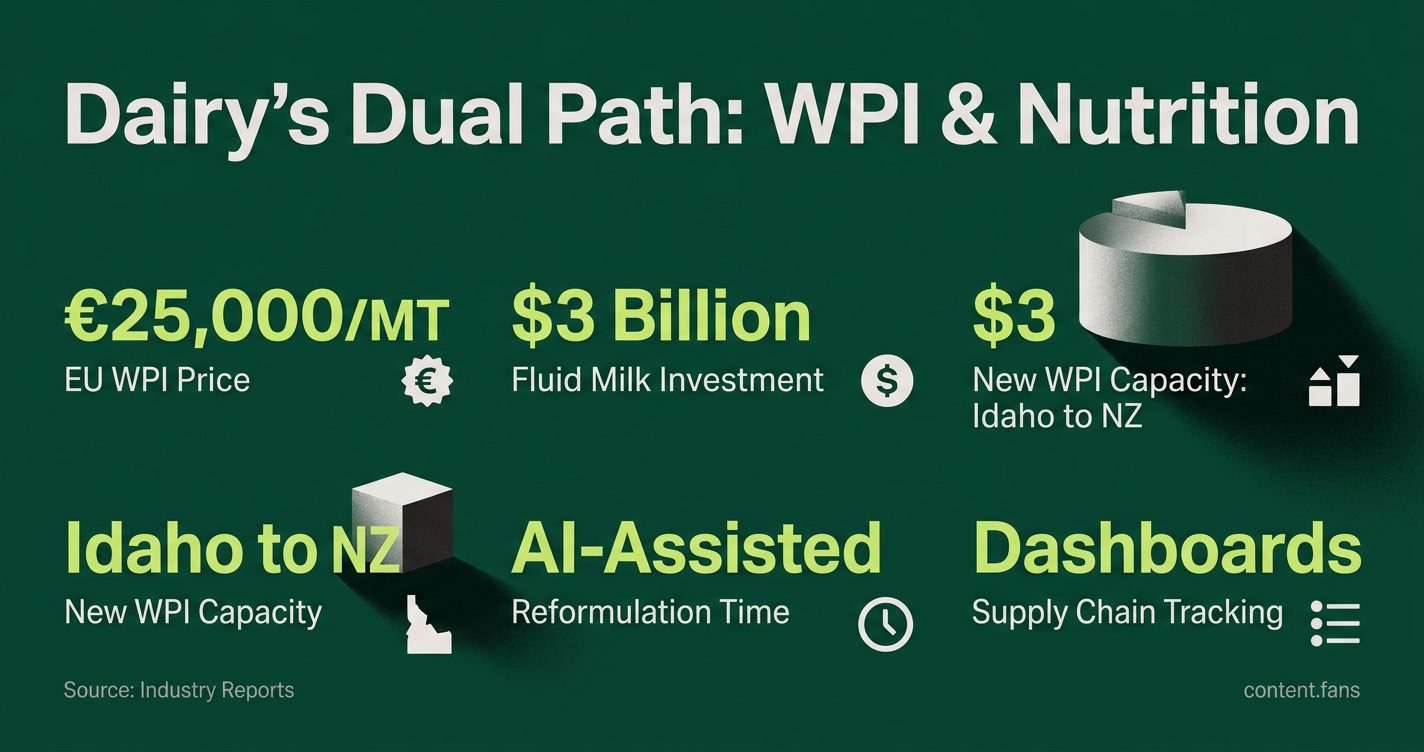

EU whey protein isolate prices are reportedly approaching €25,000 per metric ton, while U.S. spot values have shown significant increases according to industry reports. The same reports caution that demand destruction could emerge if prices climb further. Industry sources note that processors from Idaho to New Zealand are racing to add dryers and filtration lines to capture the current spread between raw whey and finished proteins.

These figures suggest that capacity expansion remains financially compelling. However, whey markets have cycled before, and industry analysts warn that new plants coming online may cap upside pricing.

Balancing capacity expansion for WPC/WPI with development of platform offerings

Rising demand for high-protein foods intersects with a broader shift toward functional formulations. Industry reports indicate that new dairy beverages are being tailored to support consumers using GLP-1 medications, often requiring custom nutrient premixes. Farm Credit East estimates roughly $3 billion has already been allocated to fluid milk plants that make ultra-filtered, high-protein drinks. This may indicate that processors who link stainless-steel investments with formulation services can diversify revenue before the next price trough.

What a platform investment looks like

Building a platform capability usually means adding small but skilled teams rather than huge assets. Premix rooms, pilot kitchens, and flavor labs can sit beside large dryers and fractionation towers. McKinsey research highlights AI-assisted sensory databases that cut reformulation time, while Folio3 describes supply-chain dashboards that track premix lots, expiry, and temperature. Both tools favor quick product turnarounds and tighter quality control.

• Premix blending lines: designed for short runs of vitamin, mineral, and flavor systems.

• Application labs: allow customers to prototype shakes, yogurts, or shots on site.

• Demand-linked MRP: forecasts micro-ingredient needs to avoid costly rush orders.

• Sensory analytics: pairs expert panels with data models to fine-tune flavor masking.

Risk management benefits

Committing every dollar to commodity protein assets ties earnings to a volatile spot market. Platform services can smooth cash flow because fees for formulation work, small-batch blends, or ready-to-drink co-manufacturing are less exposed to whey prices. Ever.Ag reports that WPC and WPI markets remain "extremely tight," yet the same document mentions buyer concerns about affordability, implying that differentiated products could command steadier margins if ingredient costs retreat.

Implementation checkpoints

- Allocate a fixed portion of capex to capability building rather than volume alone.

- Sequence hires so that R&D, pilot production, and commercial staff arrive before the first platform launch.

- Embed lot-level traceability and cold-chain monitoring for every premix shipment, as outlined by Folio3.

- Review regulatory and labeling impacts of masking agents early, reducing reformulation cycles.

Monitoring success

Coherent Market Insights values the dairy nutrition market at approximately USD 21.4 billion in 2026 and projects 8.1 percent CAGR through 2033. Management teams can track their share of that pool by combining internal KPIs - such as premix fill rate, new formula win rate, and average selling price per kilo - with external indicators like the spread between raw whey and finished WPI. When those metrics converge, the dual-track strategy may be delivering the intended hedge against commodity swings.

Why are dairy processors torn between expanding WPI capacity and building nutrition platforms?

Current WPC and WPI margins are exceptional. Industry reports show EU WPI prices approaching significant highs and U.S. WPI spot prices showing substantial increases. That upside tempts processors to pour capital into new fractionation plants. Yet the same market reports warn that relief from new capacity is likely gradual. By the time those plants ramp, price cycles could have reversed.

At the same time, industry research indicates the whey protein market is projected to show strong growth, with significant expansion expected through 2033. Capturing that growth increasingly hinges on nutrition platforms - premixes, functional beverages, and clinically positioned products - that diversify revenue beyond commodity swings. A dual-track strategy therefore balances short-term margin capture with long-term differentiation.

How large is the industry investment shift toward nutrition platforms and premix services?

Industry reports indicate the sector has channeled substantial investment into processing assets in recent years. Analysis highlights the nutrition focus:

- Significant investment in cheese plants - many adding high-protein formats

- Major investment in fluid milk plants targeting ultra-filtered, high-protein beverages and shakes

- Substantial investment in yogurt and cultured dairy for fortified and functional lines

Parallel market sizing shows the Dairy Nutrition Market showing strong growth, with significant expansion expected through 2033. These figures confirm that premix and platform investments are moving from pilot projects to balance-sheet priorities.

What operational hurdles emerge when dairy processors adopt flavor masking and premix logistics?

Flavor masking and premix handling are unfamiliar territory for many dairy suppliers. Key challenges identified by industry sources include:

- Cost inflation: A significant portion of U.S. processors rank cost management as a top priority

- Cold-chain fragility: premix vitamins, minerals, and micro-encapsulated flavors degrade if temperature or humidity drift outside specifications

- Lot-level traceability: every premix batch must be audit-ready to support clean-label or medical-nutrition claims, pushing compliance costs upward

Processors that overcome these hurdles rely on MRP-linked planning, dual-qualified suppliers, and IoT sensor networks to maintain low batch rejection rates.

Which demand drivers are accelerating the need for nutrition platforms in dairy?

Several growth vectors converge:

- Sports nutrition and functional beverages already outpace supply, keeping WPI structurally tight

- GLP-1 medication nutrition is adding incremental volume requirements; industry reports note this use-case "pulls additional volume into an already strained supply situation"

- Aging and active consumers seek high-protein, low-lactose formats, pushing demand for specialized premixes with added fiber, electrolytes, and micronutrients

Together these drivers explain why platform revenue is growing faster than commodity protein itself.

What practical actions should dairy processors take today to balance both tracks?

- Capital allocation split: earmark the majority of capex for proven WPC/WPI expansion while allocating a significant portion for pilot-scale nutrition platforms including application labs and premix suites

- Cross-functional squads: create tiger teams with R&D, supply-chain, and commercial members to move from concept to first retail SKU within reasonable timeframes

- Supplier collaboration: establish dual sourcing for high-impact masking ingredients and share rolling forecasts to cut lead-times

- Tech stack: deploy integrated dashboards that track premix lot expiry, sensory defects, and cost per gram of protein - error rates fall substantially once real-time data is available

- Regulation check-point: insert a compliance gate early in every NPD sprint to ensure label, allergen, and claim requirements are met before pilot runs

Following these steps lets processors harvest current WPI margins while building tomorrow's defensible nutrition franchises.