Anthropic's revenue run rate reaches $30B, potentially topping OpenAI's $25B

Serge Bulaev

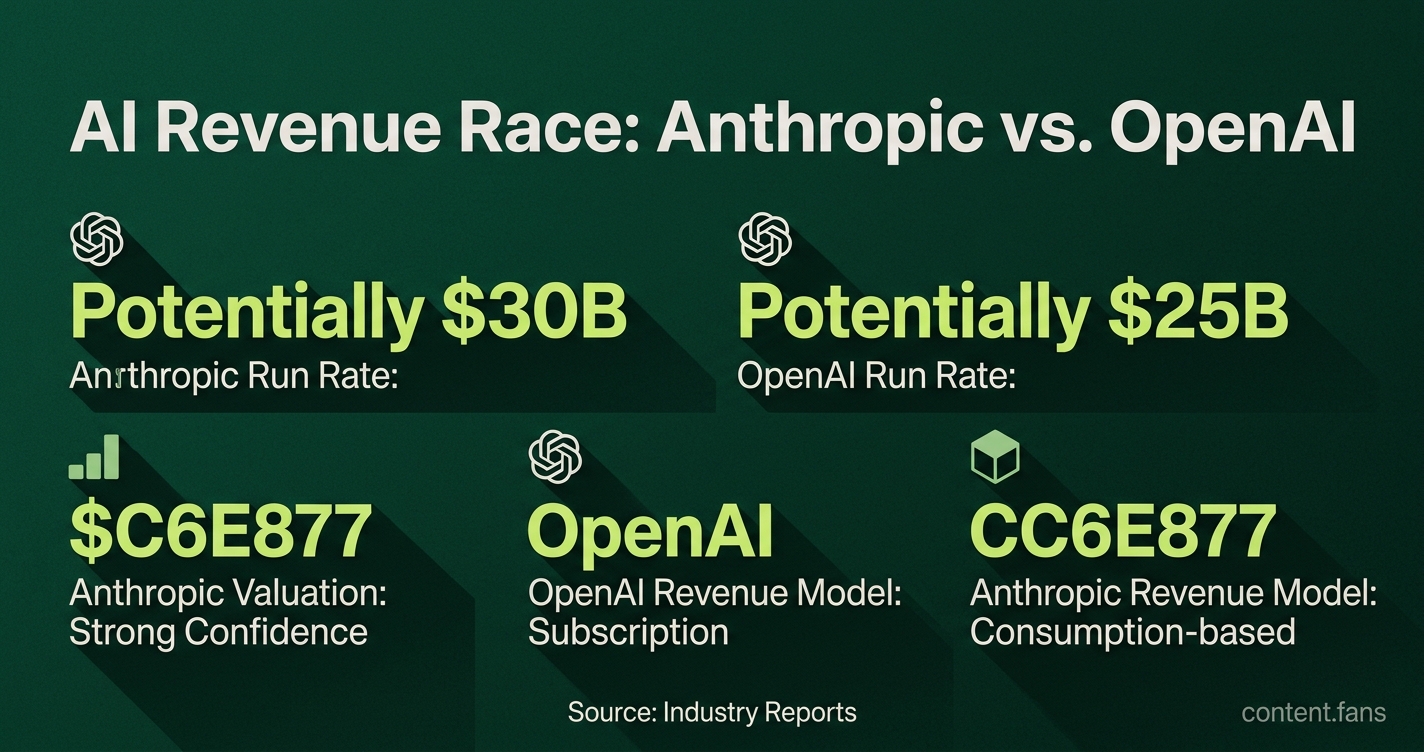

Recent reports suggest Anthropic's annual revenue run rate may have jumped to around $30 billion, possibly passing OpenAI's $25 billion run rate. Some sources indicate Anthropic might have closed the revenue gap with OpenAI, and there is strong market belief that Anthropic could have a higher valuation by the end of 2026. However, the way revenue is calculated for both companies can differ and may give a misleading picture of true financial health. Analysts say investors now care more about how much revenue companies keep and their profit margins, rather than just total sales. Both companies are spending a lot on infrastructure, and there is uncertainty about how they will be valued when they go public.

In a notable shift within the AI landscape, recent industry reports indicate Anthropic's revenue run rate has experienced dramatic growth, showing a significant increase from previous periods. This explosive growth potentially positions Anthropic as a stronger competitor to its chief rival, OpenAI, whose run rate remains substantial according to industry estimates. This new reality sets the stage for a landmark test of public market appetite for AI's hyper-growth, consumption-based business models ahead of anticipated IPOs.

Who Is Ahead on Revenue Momentum?

Recent reports suggest Anthropic's annualized revenue run rate may be gaining ground on OpenAI's position. This momentum shift is based on Anthropic's recent consumption metrics, though different calculation methods make a direct comparison complex. Market sentiment appears to favor Anthropic's growth trajectory.

Mid-2025 reporting showed Anthropic well below OpenAI on revenue/run-rate terms; any lead appears to be a 2026 development, not a mid-2025 one. According to Reuters, the company "may have closed the revenue gap on OpenAI" by annualizing its most recent 28-day consumption figures. Industry reports suggest Anthropic's run rate has shown significant growth, with some estimates indicating it may be approaching or matching OpenAI's position. This surge is reflected in market sentiment, with prediction markets indicating strong confidence that Anthropic will achieve a higher valuation than OpenAI by the end of 2026.

Private Valuations and the IPO Horizon

The race extends to private market valuations as both companies eye the public markets. Anthropic announced a substantial Series G funding round in February 2026 at a significant valuation. Reports later discussed possible future valuations far above that level, though no confirmed rounds at those higher valuations have been established. Meanwhile, OpenAI's last primary-market valuation was substantial according to industry reports. While IPO timelines are not yet fixed, industry analysts suggest both companies are considering public listings in the near future, with various target timeframes under discussion.

Why Accounting Differences Obscure the True Leader

Direct financial comparisons are complicated by differing accounting methodologies. Anthropic's use of a 28-day revenue multiplier, while indicative of momentum, is not a GAAP-compliant figure and is susceptible to temporary usage spikes from large clients. Key analytical distinctions include:

- Gross vs. Net Revenue: Some platforms report total customer spending as gross revenue, inflating the top line, while only retaining a small fraction.

- Revenue Models: OpenAI relies heavily on predictable subscription revenue from products like ChatGPT, whereas Anthropic's growth is driven by consumption-based API usage.

- Customer Concentration: Volatility in usage from a small number of large customers can create dramatic swings in annualized run-rate figures.

- Partner Agreements: Complex revenue-sharing and cloud-credit deals can significantly alter net revenue and profit margins once fully accounted for.

Reflecting this complexity, a consensus is forming among analysts that metrics like net revenue retention and gross margin are more reliable indicators of long-term value than headline revenue. Industry studies suggest that improvements in net revenue retention can significantly boost valuation multiples.

The High Stakes of Infrastructure Spending

Underpinning this growth is massive infrastructure investment. Both companies face enormous compute costs, with substantial public cloud and semiconductor commitments over multiple years. As analysts at Goldman Sachs highlight, the critical balance between upfront model training expenses and ongoing inference costs will be a key determinant of profitability and a crucial factor for public market investors to evaluate.

Market Sentiment and Pre-IPO Signals

Current investor enthusiasm appears focused more on the potential for margin improvement than on current profitability. This sentiment is visible in the secondary markets, where both companies' shares have seen various price movements relative to their primary valuations. However, these pre-IPO signals are preliminary. The ultimate test will come when S-1 filings force both companies to disclose audited financials, including customer concentration, revenue recognition policies, and true gross margins, setting the definitive narrative for the upcoming IPO season.