EU Ends De Minimis Rule in 2026, Adds 3 EUR Duty to Low-Value Imports

Serge Bulaev

The EU is ending its de minimis rule in July 2026, so parcels worth up to 150 EUR will no longer be exempt from customs duty. Instead, a temporary 3 EUR duty per item category will be added, along with VAT, which may cause prices to rise by 12-30% for low-value goods. Retailers might change their shipping methods and pricing to handle these costs and avoid delays. This flat duty is expected to last until mid-2028, when new product-specific tariffs will start. Some goods covered by trade deals may still be exempt if VAT is reported through IOSS.

The EU ends its de minimis rule in 2028, a landmark customs reform eliminating the €150 duty-free threshold for all imports. This comprehensive guide details the new temporary customs duty, its effect on landed costs, and the essential strategic adjustments e-commerce retailers must prepare for.

What Actually Changes in 2028?

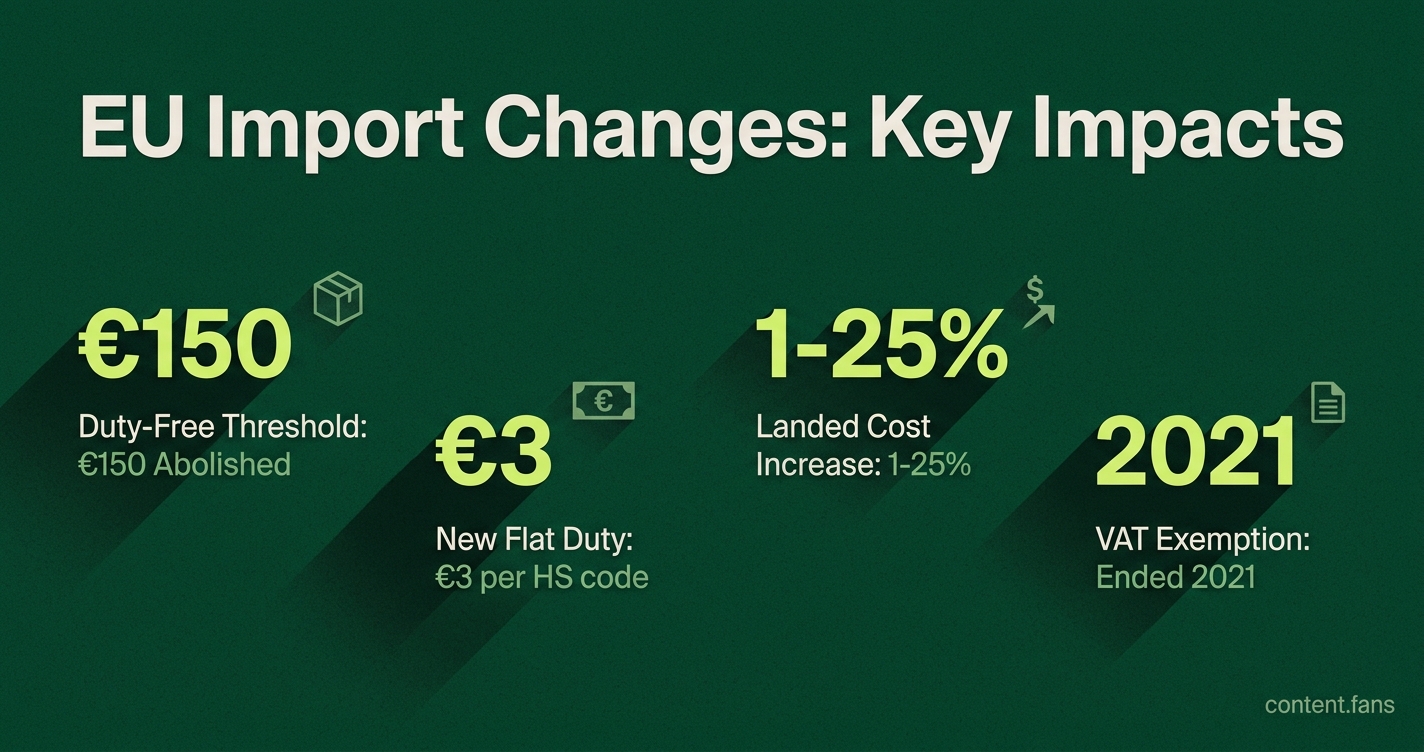

In 2028, the EU's €150 duty-free threshold for imports will be abolished. In its place, a temporary €3 flat-rate customs duty will apply to low-value consignments up to €150. This duty is charged per item category (HS code), not per individual parcel.

The long-standing duty exemption for low-value goods disappears, triggering a temporary €3 customs duty for each tariff heading in a consignment, according to the European Commission. This means a single shipment with multiple product types could incur several €3 charges. This flat-rate system is an interim measure scheduled to last until mid-2028, when it will be replaced by standard product-specific tariffs managed through the new EU Customs Data Hub.

How This Differs from the 2021 VAT Changes

The 2021 reform abolished the VAT exemption for low-value imports (previously €22), requiring VAT on all imports from the first euro. It did not primarily target customs duties. The 2026 reform targets customs duties (abolishing the €150 duty-free threshold).

| Change | Status | Impact |

|---|---|---|

| VAT de minimis | Ended in 2021 | VAT now applies from the first euro on all imports |

| Customs duty de minimis | Ends 2028 | The €150 duty-free threshold is abolished |

While separate, the two taxes interact. VAT is calculated on the total value of a shipment, which includes the product price, shipping costs, and now the new €3 duty. Sellers using the Import One-Stop Shop (IOSS) can collect VAT at checkout to prevent customers from facing unexpected fees and delays upon delivery.

The Economic Impact on Products and Consumers

Low-value items will be disproportionately affected. For low-value accessories, the €3 duty represents a significant price increase before VAT is even considered. This threatens the profitability of impulse buys and low-cost goods, with landed costs for apparel and fashion accessories expected to rise by 1-20% (with some forecasts up to 25%), driven by new tariffs for categories like:

- Fashion accessories

- Small electronics and homewares

- Product samples

This shift will likely alter consumer behavior. Industry analysis suggests that price-sensitive shoppers will consolidate orders, increasingly prefer EU-based sellers to avoid duties, and reduce impulse purchases of cheap, single-item imports.

How Retailers Should Adjust Logistics and Pricing

The end of de minimis requires a structural shift away from direct-to-consumer shipping for individual low-value parcels. Supply chain experts predict a market-wide pivot toward consolidated bulk freight and EU-based fulfillment centers. This strategy stages inventory locally, reducing per-item duty exposure and customs friction.

The Delivered Duty Unpaid (DDU) model, where the customer pays fees on delivery, is becoming unviable due to high rates of cart abandonment and rejected parcels. Retailers must transition to Delivered Duty Paid (DDP) models or localized inventory.

Key strategic decisions include:

- Absorbing duties to protect conversion rates at the cost of margins.

- Passing costs to customers, which risks losing sales, especially for sub-€30 items.

- Automating HS code validation to prevent clearance delays.

- Implementing dynamic checkout pricing that shows customers the full landed cost in real time.

Timeline and Data Requirements for Compliance

The €3 flat fee is temporary. Consignments with goods covered by a preferential trade agreement remain exempt from the fee if VAT is declared through IOSS. Retail compliance teams must track these regulatory milestones:

- 2025: De minimis exemption ended on Aug 29, 2025.

- 2028: EU Customs Data Hub development continues; product-specific duties expected to replace the flat fee.

As all shipments move into standard customs channels, accurate product classification, complete electronic data, and timely VAT reporting will become non-negotiable for avoiding costly holds and ensuring a smooth customer experience.