Anthropic's 20x Revenue Multiple: What Justifies the Premium?

Serge Bulaev

Anthropic's high 20x revenue multiple may be justified because its revenue is growing very fast, with reports suggesting it jumped from $4.8 billion to $10.9 billion in one quarter. Analysts say this multiple is not unusual for top AI companies, though it is much higher than traditional software firms. However, there is uncertainty about whether Anthropic can keep strong profit margins, as some reports suggest profits may not be steady until 2028. Investors need to check details like how revenue is made, compute costs, and competition before accepting this high price. Small changes in growth or costs might greatly affect returns, showing the risks of paying such a premium.

Understanding Anthropic's 20x revenue multiple requires analyzing its hypergrowth trajectory, as fresh financial data provides the numerical basis for debate. Valuing hypergrowth AI firms like Anthropic begins with one question: what justifies paying such a premium?

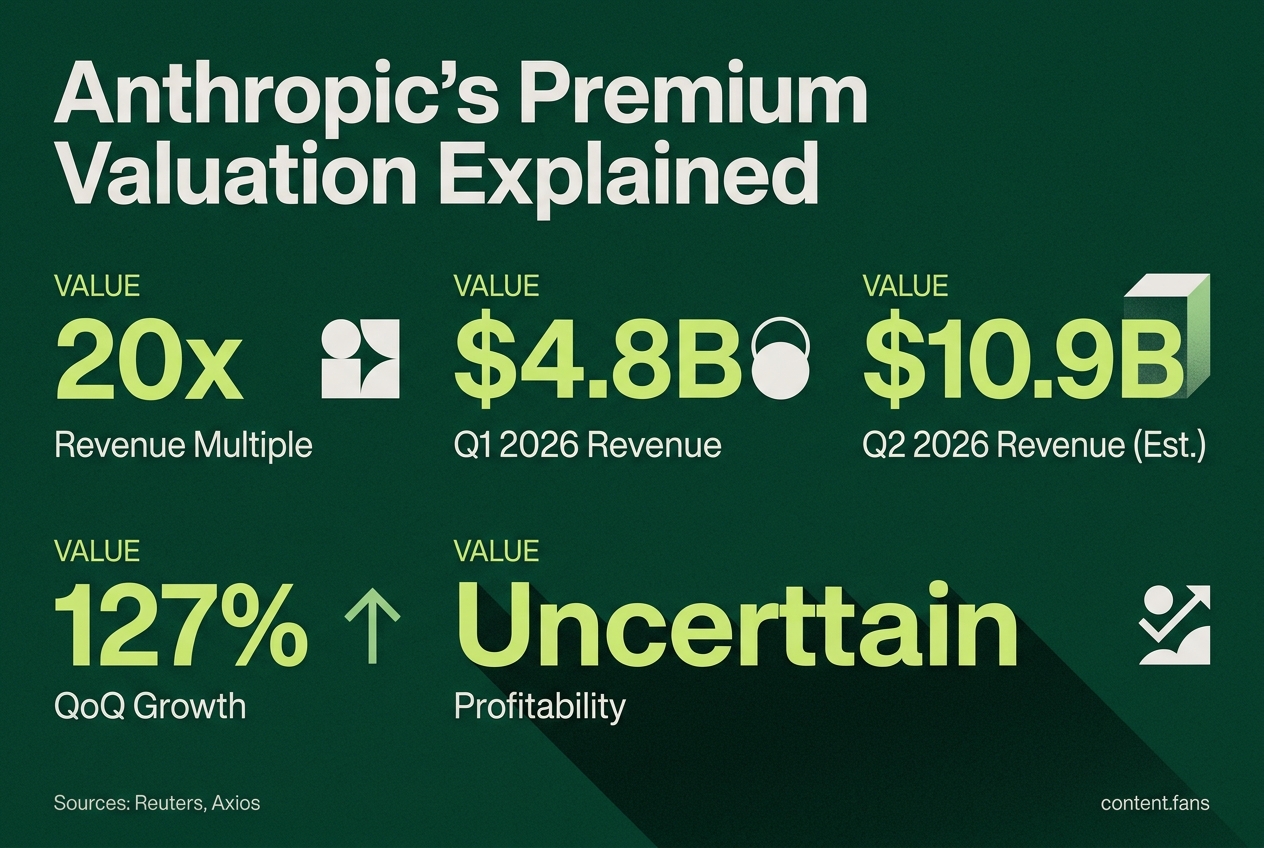

Recent reports indicate explosive growth: the company was reportedly around $4.8 billion in Q1 2026 and expected to reach about $10.9 billion in Q2 2026, which is roughly a 127% increase quarter over quarter (Reuters). Moreover, according to industry reports, its annualized revenue run rate has grown significantly over recent months (Axios).

Why a 20x Multiple May Be Within Range

The premium valuation is primarily justified by Anthropic's extreme revenue acceleration. When a company's revenue doubles quarterly, its forward-looking multiples compress rapidly, making a high entry valuation seem more reasonable. This growth rate places it squarely within the valuation band of other top-tier AI infrastructure companies.

Market data suggests this valuation is not an outlier for a leading AI firm. According to industry reports, AI startups often trade at significant multiples to revenue, with core infrastructure players commanding premium valuations. Industry data shows LLM vendors and broader AI infrastructure companies trading at substantial multiples, positioning Anthropic's multiple well above legacy SaaS firms but within the range of its direct competitors.

However, valuation is contingent on profitability. While Anthropic may report its first operating profit in the coming quarters according to industry reports, long-term margin stability is uncertain. Heavy compute costs could pressure margins, potentially affecting sustained profitability timing. Therefore, a 20x multiple bakes in an assumption of durable margin expansion, not just a single profitable quarter.

Key Due Diligence Areas for Investors

- Revenue Composition: Scrutinize the mix of recurring, usage-based revenue versus large, non-recurring deals.

- Compute Cost Trajectory: Model how price-per-token economics will shift as new, large-scale infrastructure contracts come online.

- Customer Concentration: Evaluate the renewal risk associated with a high concentration of revenue from a few key cloud partners.

- Competitive Landscape: Analyze Anthropic's positioning against OpenAI's extensive ecosystem and the increasing viability of lower-cost open-source models.

Scenario Framework for Valuation Sensitivity

| Variable | Bull case | Base case | Bear case |

|---|---|---|---|

| FY 2027 revenue growth | High growth | Moderate growth | Conservative growth |

| Gross margin trend | Significant expansion | Flat | Contraction |

| Implied EV/Rev at entry | 20x | 20x | 20x |

| Two-year forward EV/Rev exit | Lower multiple | Mid-range multiple | Higher multiple |

As the table illustrates, even modest changes in growth or margin assumptions can dramatically alter prospective returns from a 20x entry multiple. Stress-testing the valuation - for example, by reducing growth forecasts or increasing compute cost estimates - is critical, as it reveals how quickly exit multiples can fall below market medians. Ultimately, while hyper-acceleration justifies a premium valuation, it also leaves a very narrow margin for error.

How should investors interpret a 20x revenue multiple for a company growing substantially quarter-over-quarter?

According to industry reports, revenue valuations for AI companies sit within a significant range - not cheap, but hardly extreme for category leaders. What turns that headline multiple into a plausible entry point is the compounding speed: substantial sequential growth can dramatically compress forward-looking multiples, so the same share bought today costs significantly less on a forward run-rate revenue basis only quarters out. Investors who model continued growth at pace find effective exit multiples at levels that legacy-SaaS names accept for moderate organic growth. The trick is to watch the inflection: once growth moderates significantly, the same math pushes the multiple back up and the cushion disappears.

Which due-diligence lenses matter most when the headline number looks absurdly high?

- Revenue quality - split API/token income from seat licenses; API streams re-price regularly, so token-cost reductions can impact gross margin significantly.

- Customer concentration - if top accounts deliver a significant portion of ARR, model substantial churn in your bear case and see whether cash covers the compute bill.

- Compute economics - treat GPU leases as variable COGS. Reported operating profits could flip to losses if GPU pricing increases materially.

- Pricing power vs. open-source - run a sensitivity where open-source models capture meaningful share and force price cuts; check whether gross margin can stay healthy.

- Data moat half-life - estimate how fast model performance deltas decay; if edge shrinks significantly over time, maintenance R&D must rise substantially just to stay flat.

What does current profitability guidance signal about long-run margin durability?

Industry reports suggest Anthropic could post its first operating profit in upcoming quarters, yet also warn that full-year profitability remains uncertain because new compute commitments may pressure margins later on. Translation: fixed GPU racks are being spread over a growing revenue base, creating a short-term surplus, but any re-acceleration of capex - or a revenue miss - swings the pendulum back to red. Investors should therefore treat breakeven as a milestone, not a floor, and stress-test models with revenue shortfalls plus compute-cost spikes; under such scenarios, operating margins could turn significantly negative.

Where on the cap-table should analysts expect the biggest re-pricing risk?

Down-round protection sits with the last private investors. According to industry reports, Anthropic's recent growth trajectory implies rounds priced on substantial multiples; if growth moderates and multiples revert to lower levels, recent entry valuations could be significantly impacted. Public-comps baskets currently trade at meaningful multiples, so a future IPO exit could still be below the last private print if sentiment softens. Analysts should therefore flag ratchet and liquidation preference language; full-ratchet anti-dilution would transfer value from common holders to the latest round, magnifying downside for employees and early angels.

How do OpenAI and open-source models threaten Anthropic's pricing power?

- OpenAI bundles frontier models with a broad application ecosystem; if enterprises standardize on a single vendor stack, Anthropic risks being squeezed on distribution, not just model performance.

- Open-source models already hold a growing share of the LLM market and appeal where data sovereignty or cost sensitivity dominates; industry analysis notes that when proprietary vendors restrict access, open-source alternatives remain viable substitutes.

- Market data suggests Anthropic holds a significant enterprise share versus OpenAI, but that lead is not locked in - a substantial portion of head-to-head deals remain competitive, enough for a fast reversal if competitors narrow key gaps.

- The pricing floor is therefore set not by Anthropic's margin target but by the fully-loaded cost of an open-source deployment; any premium above that level must be justified by measurable accuracy, safety or latency advantages that customers will pay to keep.