PitchBook Unveils AIBQ Framework, Finds AI Valuation-Quality Paradox

Serge Bulaev

PitchBook has introduced the AIBQ framework so investors can better judge the long-term strength of AI companies, rather than just their short-term performance. The framework gives weighted scores on revenue quality, capital efficiency, computing independence, governance optionality, and competitive durability. Results suggest that some of the most expensive AI companies, like OpenAI, may have weaker business fundamentals, while others like Databricks appear to score higher on quality. This may show that investor excitement could be outpacing actual business strength in the AI sector. The AIBQ scorecard may help investors look beyond high valuations and focus on business quality and resilience.

PitchBook has launched the AI Business Quality (AIBQ) framework, a new standardized scorecard for investors to evaluate the long-term fundamentals of AI companies. This tool addresses a growing AI valuation-quality paradox, where market hype may be outpacing a company's actual business strength, giving capital allocators a unified language for assessing late-stage AI assets.

How Does the AIBQ Scorecard Work?

The AIBQ framework is a standardized scorecard designed to assess the long-term business strength of private AI companies, moving beyond short-term performance metrics. It provides investors with a unified method for evaluating assets by assigning a weighted score based on five key pillars of business quality and resilience.

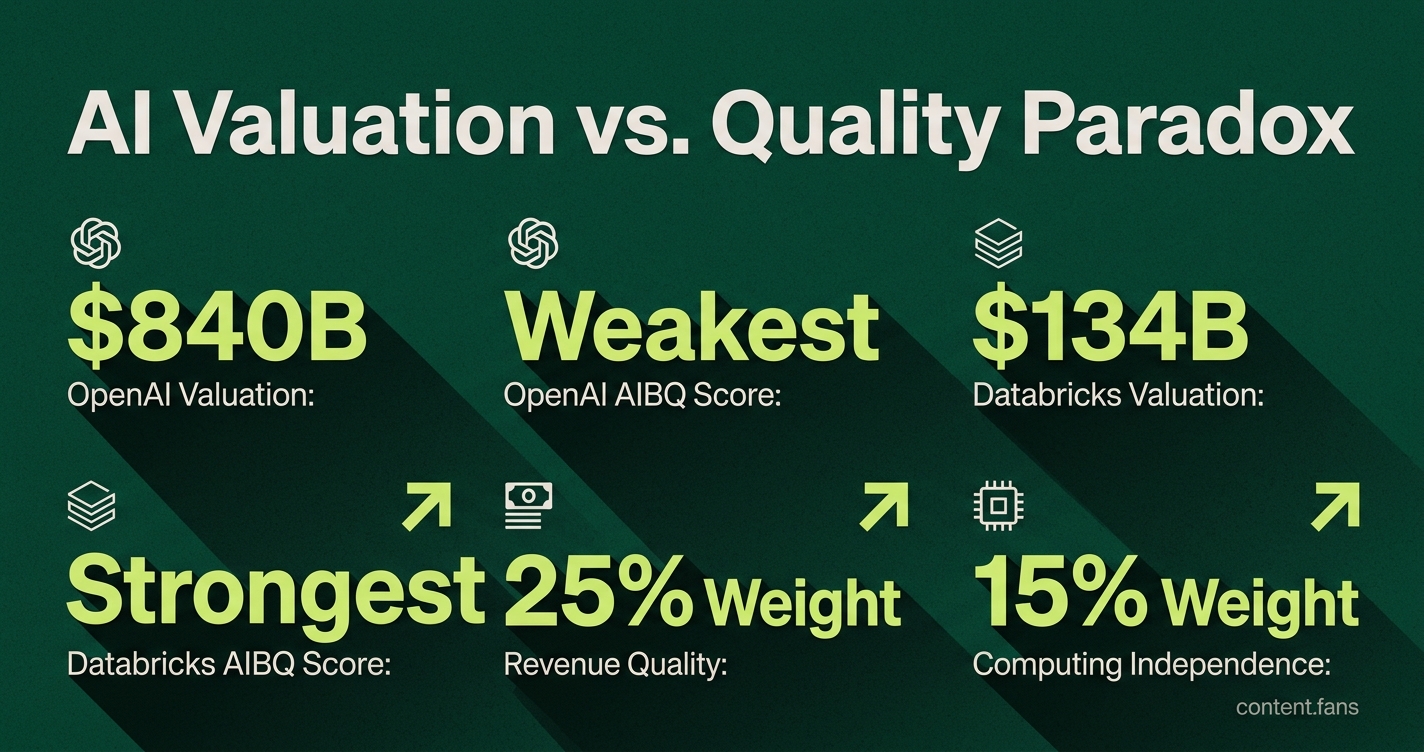

According to PitchBook's Business Wire release, the framework assigns scores across five core pillars. These include revenue quality (weighted at 25%), capital efficiency (20%), competitive durability (20%), governance optionality (20%), and computing independence (15%). Each pillar incorporates specific sub-metrics, like net revenue retention and control over GPU supply chains.

| Pillar | Reported weight |

|---|---|

| Revenue quality | 25% |

| Capital efficiency | 20% |

| Competitive durability | 20% |

| Governance optionality | 20% |

| Computing independence | 15% |

A Snapshot of the "Frontier Five"

Initial analysis using the AIBQ framework focused on the "Frontier Five," revealing key differences in their fundamental strengths:

- Databricks demonstrates the strongest capital efficiency among the group.

- OpenAI, despite having the highest estimated market valuation, shows the weakest composite AIBQ score.

- Anthropic and xAI are positioned in the middle range across most of the framework's pillars.

The AI Valuation-Quality Paradox Explained

The core finding from the AIBQ analysis is a significant "valuation-quality paradox." PitchBook analysts note that the most highly valued AI companies often exhibit the weakest underlying business fundamentals. For example, while OpenAI's estimated valuation reached $840 billion in early 2026, its AIBQ score trailed peers. In contrast, Databricks, valued at a lower $134 billion, achieved the top quality score.

This divergence suggests that investor enthusiasm and narrative-driven valuations have outpaced measurable business strength. As one PitchBook analysis noted, capital has flowed into frontier AI faster than the "analytical infrastructure" needed to properly assess it, resulting in pricing signals that may be misaligned with operational reality.

The Strategic Importance of Computing Independence

The AIBQ framework places specific emphasis on computing independence, a critical but often overlooked factor. Frontier AI labs are heavily reliant on third-party cloud providers and GPU suppliers, creating significant risk. This dependency can severely compress margins, especially as inference costs decline. By weighting this pillar, AIBQ shifts the focus from model performance benchmarks to long-term balance-sheet resilience.

AIBQ's Role in Late-Stage Venture Markets

The framework's launch is timely, given the context of the current venture market. According to a PitchBook Q1 2026 report, the median pre-money valuation for late-stage (Series D and beyond) AI companies has soared to $4.7 billion. This abundance of capital helps explain why narrative-driven valuations can persist even when fundamental quality scores are low.

For investors evaluating secondary market shares or anticipating future IPOs, the AIBQ framework offers a crucial due diligence tool. It encourages a shift in perspective, from chasing the highest valuation to scrutinizing the underlying health of the business, focusing on factors like recurring revenue, cost discipline, and governance structure.

What is the AIBQ framework and how does it work?

The AI Business Quality (AIBQ) framework is PitchBook's new scorecard that turns messy private-market data into a single 0-10 ranking.

It blends five weighted pillars:

- Revenue Quality (25%) - net retention, churn, enterprise mix

- Capital Efficiency (20%) - how much ARR each invested dollar produces

- Computing Independence (15%) - freedom from GPU or cloud lock-in

- Governance Optionality (20%) - room to maneuver through regulation

- Competitive Durability (20%) - moat depth versus commoditization

The first public run covered the "Frontier Five": Anthropic, Databricks, OpenAI, SSI and xAI.

What exactly is the "valuation-quality paradox"?

PitchBook finds a structural misalignment: the firms carrying the richest private valuations often post the lowest AIBQ scores.

In short, story is being rewarded faster than substance; investors are paying peak prices for businesses whose fundamentals - durable revenue, capital discipline, compute control - lag behind.

Which companies show the clearest paradox?

Early 2026 numbers place OpenAI at an $840 billion valuation but with the weakest AIBQ profile among the five.

Conversely, Databricks - valued at $134 billion - earns the highest AIBQ score (8.7/10), illustrating that a lower headline price can coincide with stronger long-term fundamentals.

Why does computing independence carry weight in 2025-26?

With GPU supply tight and cloud rebates shrinking, per-token margins hinge on who owns or reserves inference capacity.

AIBQ treats compute sovereignty as a leading indicator of whether a model maker can defend gross margin when API prices compress further.

How should investors use AIBQ right now?

- Benchmark new rounds - if a Series D quote implies >$50 B but the target's AIBQ sits below 6, demand visibility on revenue retention and compute contracts.

- Stack rank portfolios - re-weight holdings toward high-AIBQ names; they may weather down-cycles better even if headline upside feels smaller.

- Track momentum - re-run the five metrics quarterly; rapid improvement in capital efficiency or governance optionality can signal an inflection before the cap-table reprices.

Remember, AIBQ is a relative yardstick, not a crystal ball - yet in a market where median AI Series D+ pre-money touched $4.7 billion in Q1 2026, any tool that separates durable quality from hype is worth folding into diligence.